The Investment Thesis That No One Is Writing

Every analysis of Saudi Arabia's real estate market published over the past three years has told some version of the same story: Vision 2030 is transforming the Kingdom's built environment, mortgage penetration is deepening, the foreign ownership law is opening the market to international capital, and the residential pipeline is expanding to meet structural demographic demand. These are all legitimate and well-documented investment theses. None of them explains the specific surge in Riyadh's furnished residential unit demand in early 2025, or the acceleration of corporate leasing activity in the capital's Grade A office market at a pace that defied the usual seasonal patterns, or the pressure on serviced apartment occupancy that emerged in the Eastern Province as regional business networks shifted.

What explains those observations is something analytically distinct: a counter-cyclical, geopolitically driven flight of capital, people, and corporate functions into Saudi Arabia from markets experiencing instability or elevated risk perception elsewhere in the region. In April 2026, Asharq Al-Awsat reported the explicit version of this thesis directly: experts cited exceptional real estate growth of 20% to 30% driven by capital inflows from crisis-affected countries, a surge in occupancy across residential and hotel units as residents and investors sought stability, and an acceleration in corporate demand as companies reconsidered their regional headquarter locations. Saudi investor Mohammed Al-Murshid, a member of the Riyadh Chamber of Commerce, told the publication that the conflict was "not the main driver, but reinforced an existing trend" a careful and analytically important qualifier that investors must understand before building a position around the geopolitical narrative.

This article's purpose is to examine that narrative with institutional discipline. It maps the three-part argument Saudi Arabia as a geopolitical hedge, the specific sub-segments that absorb flight-to-stability demand most directly, and the structural limits of that demand for long-term investors with the rigor that a well-underwritten position requires. The opportunity is real. It is also bounded by fundamentals that a geopolitical narrative can temporarily amplify but cannot permanently replace.

The Historical Architecture of Safe Haven Real Estate

The concept of a real estate safe haven, a property market that attracts capital flight during periods of regional or global instability has a well-documented precedent in every geography where political stability and rule of law create a credible store of value relative to neighboring markets. London became the world's pre-eminent capital flight real estate destination during the 1970s and 1980s as political instability across Europe, the Middle East, and the former Soviet bloc drove HNWI capital into prime West End and Knightsbridge residential. Singapore absorbed capital from Indonesia during the 1998 Asian financial crisis and from Malaysia during multiple periods of political uncertainty, building a residential and commercial property market that consistently outperforms its ASEAN peers on institutional quality and price stability. Dubai's 2002 freehold law and its geographic positioning made it the GCC's dominant capital flight absorber for a generation, attracting Lebanese, Egyptian, Libyan, Syrian, and Iranian capital during successive periods of regional disruption.

Each of these safe haven transitions shares a common structural feature: the flight-to-stability demand is real and measurable in the short term, but it is only durable where the underlying market has independent structural demand drivers that can sustain occupancy, pricing, and yield once the geopolitical catalyst normalizes. London's real estate remained strong after the Berlin Wall fell because its financial sector, education system, and rule of law created independent demand for premium property at every price point. Singapore's market was sustained by its logistics hub status, its financial sector depth, and its legal infrastructure. Dubai's property market experienced significant cycles precisely because a portion of its capital flight demand was not anchored by independent commercial demand, leaving it exposed to reversal when regional conditions stabilized or when alternative options emerged.

Saudi Arabia's current geopolitical safe haven positioning is therefore most usefully analyzed against this framework: not as a simple binary capital is coming in, yields will rise but as a compound thesis in which flight-to-stability demand is stacked on top of pre-existing structural demand drivers, and where the durability of both layers must be assessed independently.

The Regional Context: When the GCC's Risk Map Shifts

The GCC has historically been understood by international investors as a bloc with broadly correlated political risk profiles, stable monarchies, oil-dependent but fiscally buffered sovereigns, and limited exposure to the type of government-change and rule-of-law risk that characterizes higher-volatility emerging markets. The regional risk map's reorientation over the past 18 months has disrupted that assumption in ways that are directly legible in real estate capital flows.

The UAE, specifically Dubai, has been the dominant regional safe haven destination for capital flight from the Levant, Iran, Pakistan, and sub-Saharan Africa for the past two decades. Its freehold zones, cosmopolitan infrastructure, neutral foreign policy positioning, and deep financial services sector created an absorptive capacity for displaced capital that no other GCC market could match. The Macro Real Estate analysis published in March 2026, updating its earlier GCC residential market overview, explicitly addressed what geopolitical intensification does to this architecture: it identified a scenario risk for Dubai in which "flight disruptions and partial airspace closures" begin to weaken the city's connectivity advantage, noting that "a broader conflict that disrupts travel, logistics or investor confidence could weaken demand more quickly than supply dynamics alone would suggest." The same analysis positioned Saudi Arabia as the "region's largest structural growth opportunity," noting that its residential market is projected to expand from USD 154.6 billion in 2025 to approximately USD 227 billion by 2031.

The critical implication is not that Dubai's safe haven status has collapsed, it has not, and the UAE's structural advantages remain formidable. It is that the margin between Saudi Arabia and the UAE as investment destinations has narrowed dramatically and, in several specific sub-markets and use categories, has reversed. Saudi Arabia is no longer primarily competing against Dubai for the second tier of GCC real estate capital it is competing for the first tier, and the January 2026 foreign ownership law, which formally opened the Kingdom to non-resident international property buyers across 170 designated geographic zones for the first time, has made that competition explicit and commercially actionable in ways it was not as recently as 2024.

The Saudi Market: Three Layers of Geopolitical Safe Haven Demand

Saudi Arabia's geopolitical safe haven dynamic operates through three distinct demand channels, each with a different duration profile, a different addressable sub-market, and a different risk framework for investors to underwrite.

The first channel is direct residential demand from displaced or relocating individuals, families and professionals from conflict-affected or high-risk-perception markets who are seeking stable, quality residential accommodation in Saudi Arabia on a temporary or medium-term basis. The Asharq Al-Awsat April 2026 reporting specifically identified this channel: Al-Murshid noted that "flight disruptions and partial airspace closures in the Gulf pushed travelers and residents toward Saudi Arabia as a relatively more stable hub," creating immediate demand for short-term rentals, furnished units, and hotels. This demand is real, it is measurable in occupancy data, and it is by definition shorter-duration than the structural residential demand driven by Vision 2030's economic programs. For investors in serviced apartments, short-term rental platforms, and hotel operators, this channel generates near-term revenue uplift that is not in underwriting models built on normal demand conditions.

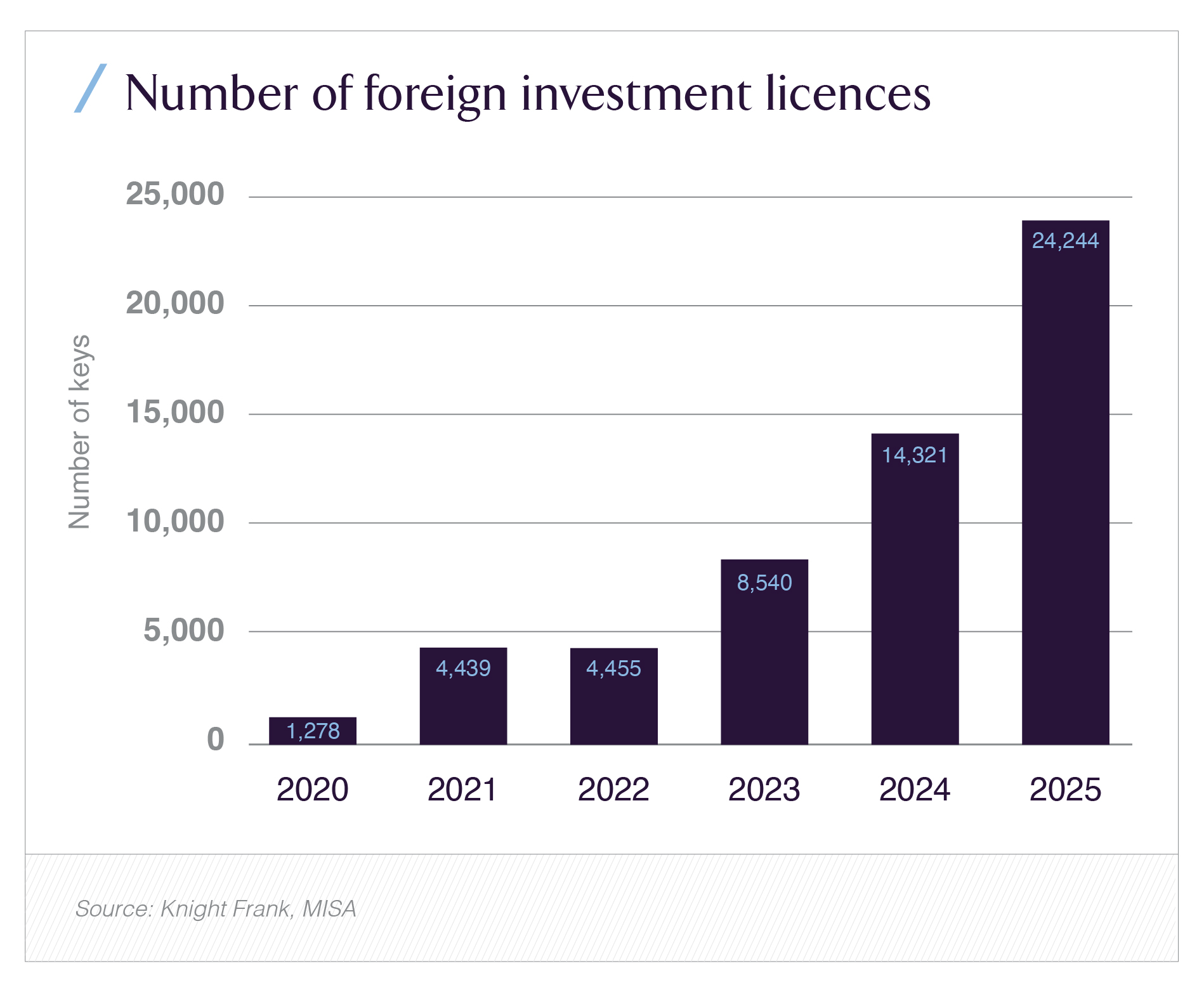

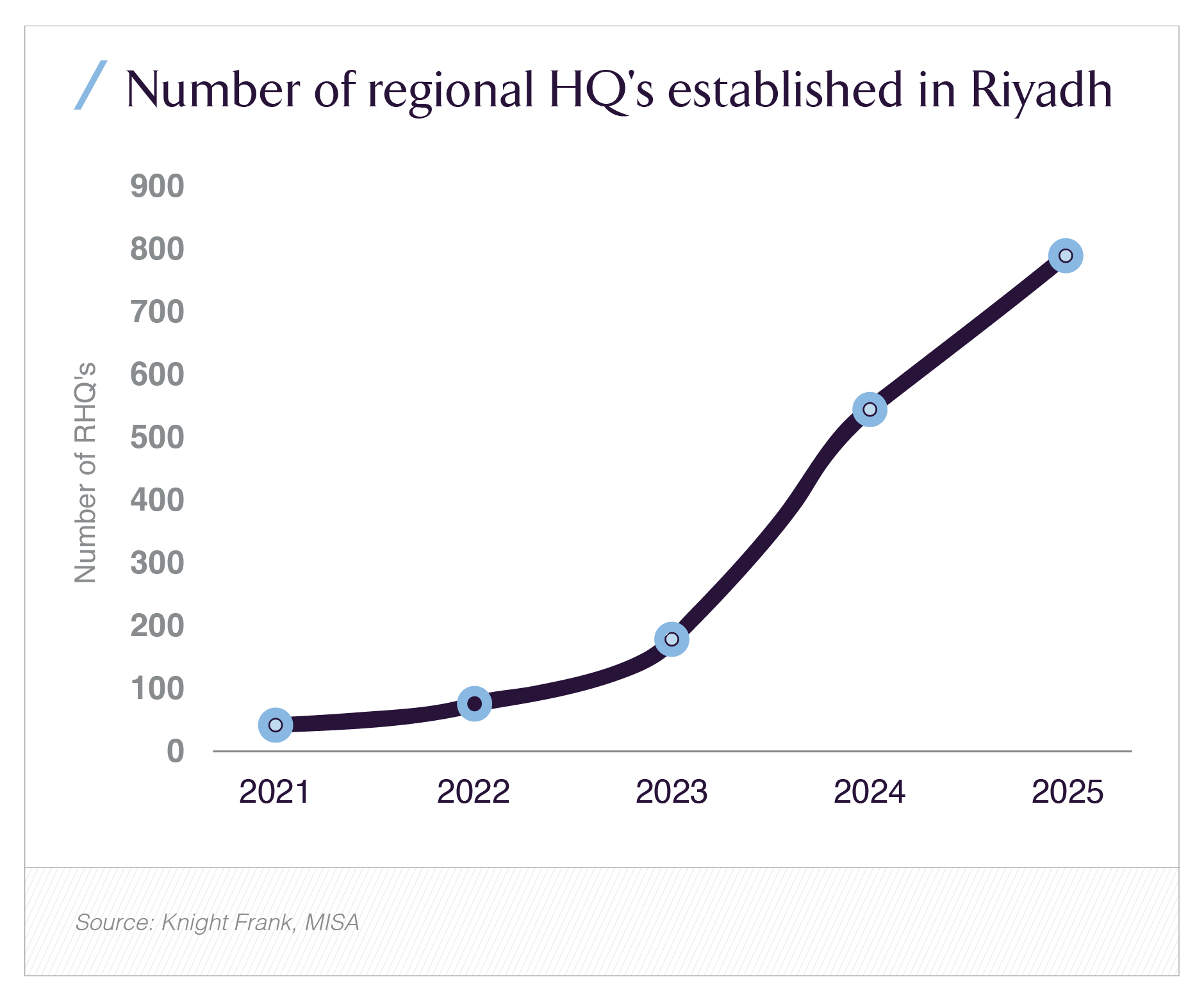

The second channel is corporate relocation, the movement of multinationals' regional headquarters, country management functions, and key personnel from higher-risk regional locations into Riyadh as the preferred Gulf business hub. This channel is both structurally underwritten and geopolitically accelerated, and it is the most important of the three for Grade A office and premium residential investors. The Regional Headquarters Program data in Knight Frank's Destination Saudi 2026 report is definitive: 44 RHQs in Riyadh in 2021, growing to 540 in 2024, and reaching approximately 780 by end of 2025. Foreign investment licences issued the lagging indicator of corporate presence rather than commitment rose from 8,540 in 2023 to 14,321 in 2024 and surged to 24,244 in 2025, a 70% year-on-year acceleration that is not explained by the linear underlying trend. The geopolitical context has compressed a corporate relocation timeline that would ordinarily span five to seven years into a two-to-three-year cycle.

The Grade A office market in Riyadh is the most direct financial beneficiary of this acceleration. Knight Frank confirms that Grade A office rents in Riyadh rose 34% in 2024, moderating to 2.8% growth in 2025 as some new supply was delivered but critically, occupancy remained at record levels. CBRE's Q1 2025 data documented Grade A occupancy at 99%, with rents up 21% year-on-year. This is not a market with pricing power left to capture in the spot rental market it is a market where forward-funded developments and pre-leased Grade A schemes represent the structural investment opportunity, because the demand pipeline significantly exceeds the supply pipeline even after accounting for the 4.2 million sqm of planned office stock that Knight Frank projects at 40–50% delivery probability.

The third channel is capital reallocation, the redirection of HNWI investment capital from regional markets perceived as elevated risk into Saudi real estate as a store of value. This channel is the most difficult to size and the most subject to reversal, but it is directly evidenced by Knight Frank's Destination Saudi 2026 survey: the report identified USD 6.3 billion in private global capital poised to enter the Kingdom's property market, with respondents from North Africa Egypt and Algeria among the most motivated groups for near-term purchase. The January 2026 foreign ownership law has created the legal infrastructure for this capital to execute, whereas before it could only circulate in informal structures or listed investment vehicles. The 170 designated zones now open to international buyers in Riyadh, Jeddah, Makkah, and Madinah represent, for the first time, a formal, legally protected, and auditable entry point for capital that previously had limited options in the Kingdom.

The Sub-Segments That Absorb Safe Haven Demand Most Directly

Understanding where flight-to-stability demand lands most efficiently in Saudi real estate requires mapping the specific product types and locations where displaced demand has lowest friction of absorption, highest available quality, most flexible tenure structures, and greatest alignment with the needs of a transient-but-premium user base.

Serviced apartments are the single most direct beneficiary of the first channel's transient residential demand, and the evidence is unambiguous. GASTAT's Q2 2025 tourism establishment data confirmed that Riyadh serviced apartment occupancy hit 57.7% meaningfully above the 52.1% recorded for hotels in the same city during the same period. The structural explanation is straightforward: displaced professionals, corporate relocatees, and families seeking medium-term stable accommodation in an unfamiliar city prefer a fully managed, all-inclusive residential format over a conventional unfurnished apartment that requires lease commitment, furniture procurement, and utility arrangement. The serviced apartment meets all of these requirements and allows the guest to transition to a longer lease structure once their situation stabilizes. For institutional investors, serviced apartments in Riyadh's northern premium sub-markets Al Olaya, Al Nakheel, and the King Abdullah Financial District area represent the cleanest expression of flight-to-stability demand, with occupancy data that persistently outperforms conventional residential rentals and pricing that has been structurally insulated from the five-year rent freeze (Riyadh's September 2025 residential rent freeze explicitly covers residential property the regulatory treatment of serviced apartments within that framework deserves careful legal review before investment commitment, as the definitional boundary between serviced hospitality and long-term residential determines whether rate escalation rights are preserved).

Grade-A furnished residential communities are the second most directly exposed sub-segment. Knight Frank's Destination Saudi 2026 survey found that 96% of all interviewees across Saudi-based expats, UAE-based expats, and international respondents expressed either strong or moderate interest in living within a master-planned residential community. Family-friendly environments, gated security, and healthcare facilities ranked as the top three sought-after community features, all of which resonate specifically with the priorities of families relocating from higher-risk environments. Riyadh boasts 180 villa compounds totaling 30,500 homes. Demand pressure on the best-located and best-managed of these compounds is already reflected in pricing: average apartment values in Riyadh increased 10.5% in 2025 to SAR 6,250 per square meter, according to Knight Frank, with prime northern district rents rising 50–60% over the preceding two years before the rent freeze was enacted.

Corporate leasing the direct office demand driven by RHQ establishment and corporate relocation is analytically the cleanest investment thesis because it is the most directly correlated to the structural policy programs that are geopolitically accelerated but not geopolitically dependent. The 780 RHQs committed or established by end of 2025 represent a legally obligated presence: companies with RHQ licences are required to maintain active operations in Riyadh, creating a contractual demand floor for Grade A office leasing that is not subject to the same reversal risk as discretionary individual residential migration. The 24,244 foreign investment licences issued in 2025 triple the 2023 figure are the upstream indicator of the corporate demand pipeline that will translate into additional RHQ establishments and office lease commitments over the 2026–2028 horizon.

The short-term and furnished rental market is the fourth sub-segment, and the one most directly responsive to episodic geopolitical events. Demand for Airbnb-style and furnished short-term units in Riyadh surged in early 2025, consistent with the Asharq Al-Awsat reporting on flight disruptions creating immediate displacement demand. For investors in purpose-built short-term rental assets or in residential real estate with flexible tenure capabilities, this channel generates near-term income uplift that conservative underwriting models should treat as non-recurring income above the normalized baseline rather than as a durable yield premium.

The Structural Limits: What Geopolitical Safe Haven Demand Cannot Do

The discipline of this investment thesis requires as much attention to its limits as to its opportunities. Three structural constraints define the ceiling on geopolitically driven real estate appreciation in the Saudi market, and any institutional position built on this narrative must account for all three explicitly.

The first constraint is the rent freeze. Riyadh's September 2025 Rental Provisions Act froze all residential and commercial rents at their then-current gross rental values for five years, with escalation clauses prohibited. For existing investors in Saudi residential assets, this creates a five-year income floor that is simultaneously a ceiling. Flight-to-stability demand that would ordinarily manifest as rental rate uplift the clearest financial expression of a geopolitical supply-demand imbalance has been administratively capped. The Kingdom's Riyadh market is therefore offering geopolitical capital flows a store of value and a capital appreciation play rather than a near-term income enhancement story. This is not necessarily a negative outcome for all investor profiles; patient equity capital seeking capital value appreciation over a five-to-ten-year horizon can still be appropriately served but it materially changes the underwriting logic relative to a market where rent escalation is structurally available.

The second constraint is supply. The Kingdom's residential pipeline approximately 6.7 million total residential units projected across major cities by 2028, up from 6.1 million today, is not the pipeline of a chronically undersupplied market. It is the pipeline of a market in active and government-supported expansion. Knight Frank estimates Riyadh alone will require over 305,000 additional homes by 2034, a demand forecast that is structural and credible; but it notes that transaction volumes declined 55% in 2025 and values fell 48%, attributing this primarily to affordability constraints at peak pricing levels. Geopolitical safe haven demand adds a demand tailwind to this environment, but it does not eliminate the price discovery process that was already underway before the regional risk event.

The third constraint is duration uncertainty. The expert consensus captured in both the Asharq Al-Awsat reporting and Knight Frank's analysis is consistent: geopolitical demand is real but finite in duration. As Faisal Durrani of Knight Frank noted in the March 2026 Destination Saudi 2026 press release, "the key downside risk lies in a prolonged escalation that disrupts travel flows, capital mobility, or business relocation decisions." A normalization of regional conditions would not erase the structural demand drivers of the RHQ program, the demographic growth, the urban expansion but it would reduce the premium that episodic displacement demand has added to near-term occupancy rates and leasing velocity. Any investment model that prices in geopolitical uplift as a permanent component of its base case is making an assumption that the market data does not support.

The Investment Architecture: How to Position for Safe Haven Dynamics Without Overexposure

The institutional framework for capturing geopolitical safe haven upside in Saudi real estate while managing the structural risks requires a clear hierarchy of investment preferences calibrated to duration, sub-market, and product type.

At the first tier, Grade A commercial office assets in Riyadh's primary business districts pre-leased to RHQ-committed multinationals on five-to-ten-year corporate leases represent the cleanest risk-adjusted expression of the corporate relocation thesis. The RHQ program's legal architecture creates durable demand that is geopolitically accelerated but structurally anchored. Lease terms are long, tenant profiles are investment grade, and the supply delivery discount (Knight Frank's estimate of 40–50% materialisation on announced stock) provides ongoing pricing support. This is an income-generating, inflation-protected commercial real estate play that benefits from geopolitical acceleration without being dependent on it.

At the second tier, professionally managed serviced apartment portfolios in Riyadh's northern sub-markets and the King Abdullah Financial District corridor serve both the corporate relocation channel and the short-term displacement demand simultaneously. Their occupancy premium over conventional residential is documented, their flexible tenure structures are directly aligned with the needs of transient-to-permanent demand migration, and their insulation from the rent freeze to the extent that their regulatory classification as hospitality rather than residential holds preserves income growth optionality that conventional residential assets do not have.

At the third tier, premium residential community investments master-planned, gated, amenity-rich serve the longer-duration element of the safe haven demand: families and professionals seeking permanent or semi-permanent relocation to Riyadh from regional markets who need the residential product that currently has the deepest demand and the thinnest institutional supply. The rent freeze constrains income growth but capital value appreciation in Riyadh's northern districts has consistently outpaced income returns over the last decade, and Knight Frank's survey data showing 63% of its 1,550 interviewees expressing interest in purchasing Saudi property with 85% of Saudi-based expats planning eventual ownership provides the structural demand confidence that long-duration capital requires.

Conclusion: Reading the Geopolitical Layer Without Mistaking It for the Foundation

Saudi Arabia's status as a geopolitical safe haven in the current regional environment is a real, measurable, and institutionally legible phenomenon. The Asharq Al-Awsat reporting, the Knight Frank capital flow data, the RHQ acceleration, the foreign investment licence surge, and the Grade A office market tightening all point to the same underlying dynamic: capital, companies, and people are moving toward Saudi Arabia from markets with elevated risk profiles, and Saudi real estate is absorbing that movement in observable, quantifiable ways.

The investor error to avoid is confusing the geopolitical layer with the structural foundation. Saudi Arabia is not a compelling real estate investment opportunity because of geopolitical flight dynamics. It is a compelling real estate investment opportunity because of demographic growth, Vision 2030 infrastructure investment, regulatory liberalization, and urban expansion at a scale that has no precedent in the Kingdom's history. The geopolitical dynamic has compressed timelines, elevated near-term occupancy metrics, and accelerated the corporate leasing cycle but the foundation was already there before the regional risk event, and it will remain after regional conditions normalize.

The investors who will generate the best risk-adjusted returns from Saudi real estate over the next decade are those who position in assets anchored to the structural demand drivers RHQ-committed corporate tenants, professionally managed serviced residential, and premium community developments in Riyadh's northern growth corridors and who treat geopolitical uplift as a timing accelerator that improves short-term income metrics and acquisition velocity rather than as a permanent component of terminal value underwriting. Saudi Arabia's property market has earned its safe haven reputation through structural reform and sovereign commitment. The geopolitical moment has simply made the rest of the world notice.