Saudi Arabia’s tourism build out is entering a new phase. After several years of headline grabbing ultra luxury openings on the Red Sea and in giga projects, officials spent November 2025 sending a different message: the next leg of growth has to be about mid and upper mid market capacity, especially for religious and mass market leisure travel.

At the UN Tourism General Assembly in Riyadh, Minister of Tourism Ahmed Al Khateeb was unusually explicit: Saudi “started with luxury destinations,” but is now building destinations for the middle and upper middle class and expanding more affordable hotel options for religious pilgrims. At the same time, the state is still on course for some of the world’s most expensive luxury resorts Miraval Red Sea, Shebara, and others but with ten “cost effective” resorts now planned on Shebara Island specifically to balance USD 2,000 per night rate points.

This pivot lands on top of a tourism base that already looks like a mid sized G20 economy:

- 115.9 million tourists in 2024, domestic + inbound, up 6% year on year.

- Around 30 million international visitors, including 18.5 million pilgrims (Umrah and Hajj).

- Travel & tourism on track to contribute >10% of Saudi GDP in 2025, with sector employment around 2.7 million jobs.

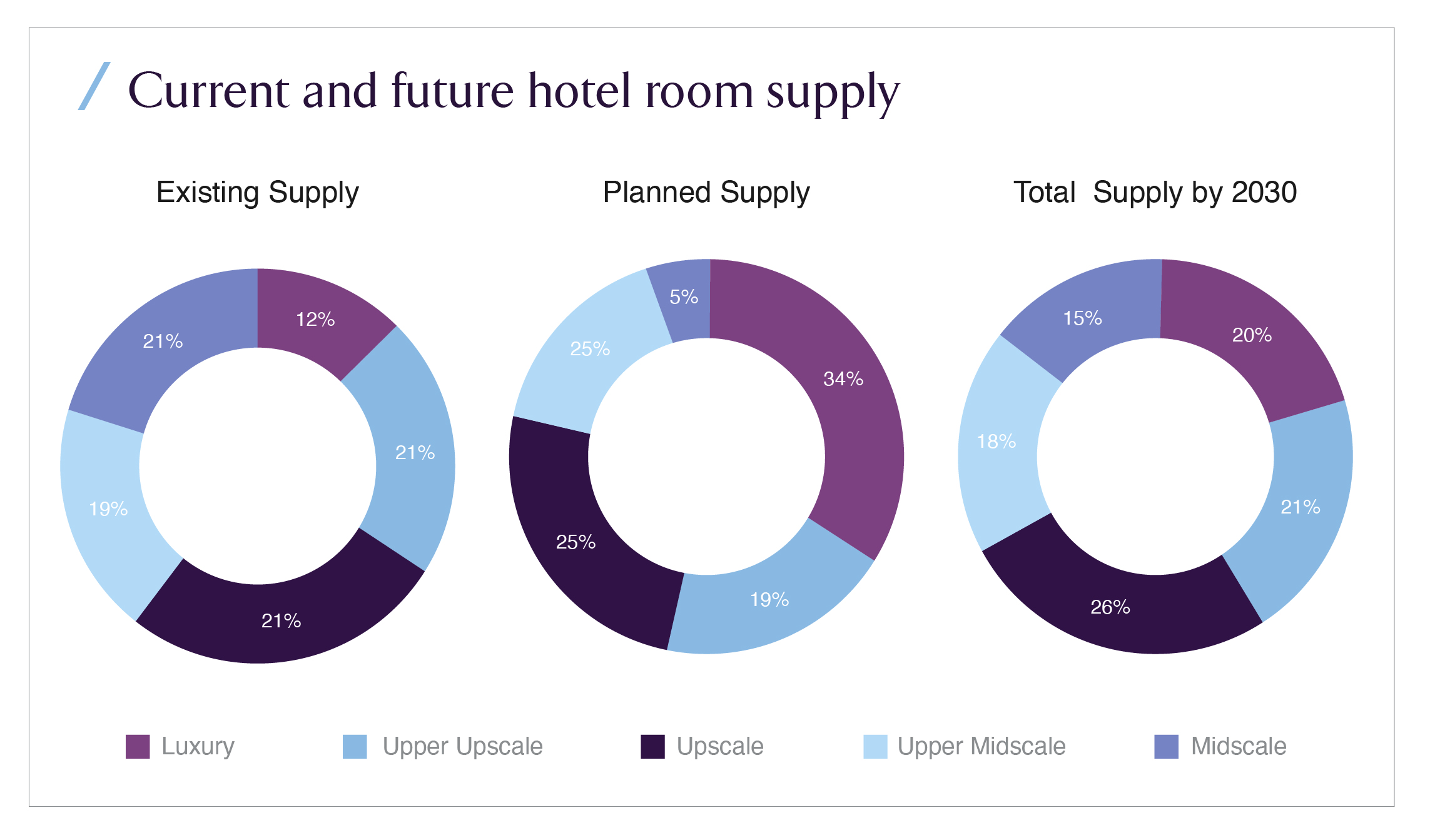

At the asset level, however, the hotel stock is still distinctly top heavy. As of Q1 2025, 61% of the 167,500 existing hotel keys are in luxury, upper upscale, or upscale categories and 78% of the 99,500 pipeline keys due by 2030 are also in these high end brackets.

The 2026 mid market push is therefore not a marginal diversification. It is an attempt to close a structural mismatch: a demand base that is majority domestic and religious, and a supply pipeline that, until now, was skewed toward ultra luxury.

Global Context: Tourism Has Recovered, But the Spend Mix Is Changing

Globally, the timing of Saudi’s pivot is not accidental.

International tourism has essentially fully recovered: UN Tourism estimates around 1.4 billion international tourist arrivals in 2024, roughly 99% of pre pandemic levels and 11% higher than 2023. Travel & tourism’s contribution to global GDP reached USD 10.9 trillion, around 10% of the world economy.

But within those aggregates, behaviour is shifting:

- Travellers are trading some ultra luxury nights for longer stays at more affordable properties.

- Demand is skewing toward religious, cultural, and experiential travel, not just beach or shopping.

- Inflation and higher for longer interest rates are squeezing middle income travellers, making price points and total trip cost much more binding.

For destinations, that means the growth edge is not only at the very top of the market. Countries that can combine credible premium offerings with deep mid market capacity 3 and 4 star hotels, branded residences, serviced apartments, and efficient limited service formats will capture larger volume and more diversified spend.

The Middle East is already the fastest growing tourism region globally, with 2024 international arrivals around 32% above 2019 levels. Saudi Arabia’s choice to rebalance its supply mix is happening while global capital is still actively hunting for scalable, policy backed tourism plays in this region.

Regional Landscape: GCC Hospitality Still Skewed to the Top End

Across the GCC, the first wave of Vision style tourism builds has been dominated by flagship luxury: over-water villas, branded residences, and 5 star city hotels. Saudi Arabia is no exception.

The Knight Frank “Saudi Arabia Hospitality Market Review – 2025” summarises the structure clearly:

- 167,500 existing keys,

- 99,500 keys under construction or in late planning,

- and roughly 362,000 keys in total expected by 2030 when giga projects are included.

Crucially, 61% of existing supply and 78% of upcoming supply sit in the luxury / upper upscale / upscale bands, with midscale and upper midscale still under represented relative to mass market demand.

At the wider Middle East level, pipeline data tell the same story. Saudi leads the regional construction pipeline with 349 hotel projects, while luxury and upscale chains account for 55% of all projects across the Middle East.

That luxury bias has been rational up to now: early phases of Vision 2030 and giga projects needed iconic assets to change brand perception and prove that the Kingdom can deliver global standard hospitality at scale. Investors, in turn, have been comfortable underwriting high ADR, high capex assets backed by PIF or other state linked sponsors.

The policy signal in late 2025 is essentially that the “iconic phase” is not over, but it is no longer sufficient.

Saudi Tourism Today: Demand Is Already Mass Market

Look past the high end resorts and the demand picture is fundamentally mass market and domestic:

- 115.9 million tourists in 2024, of which 86.2 million were domestic and 29.7 million international.

- Total spending of around SAR 284 billion (USD ~75.7 billion), with inbound spending up strongly year on year.

- A travel surplus (balance of payments) rising to almost SAR 50 billion in 2024.

On the religious side, Saudi is already operating at scale:

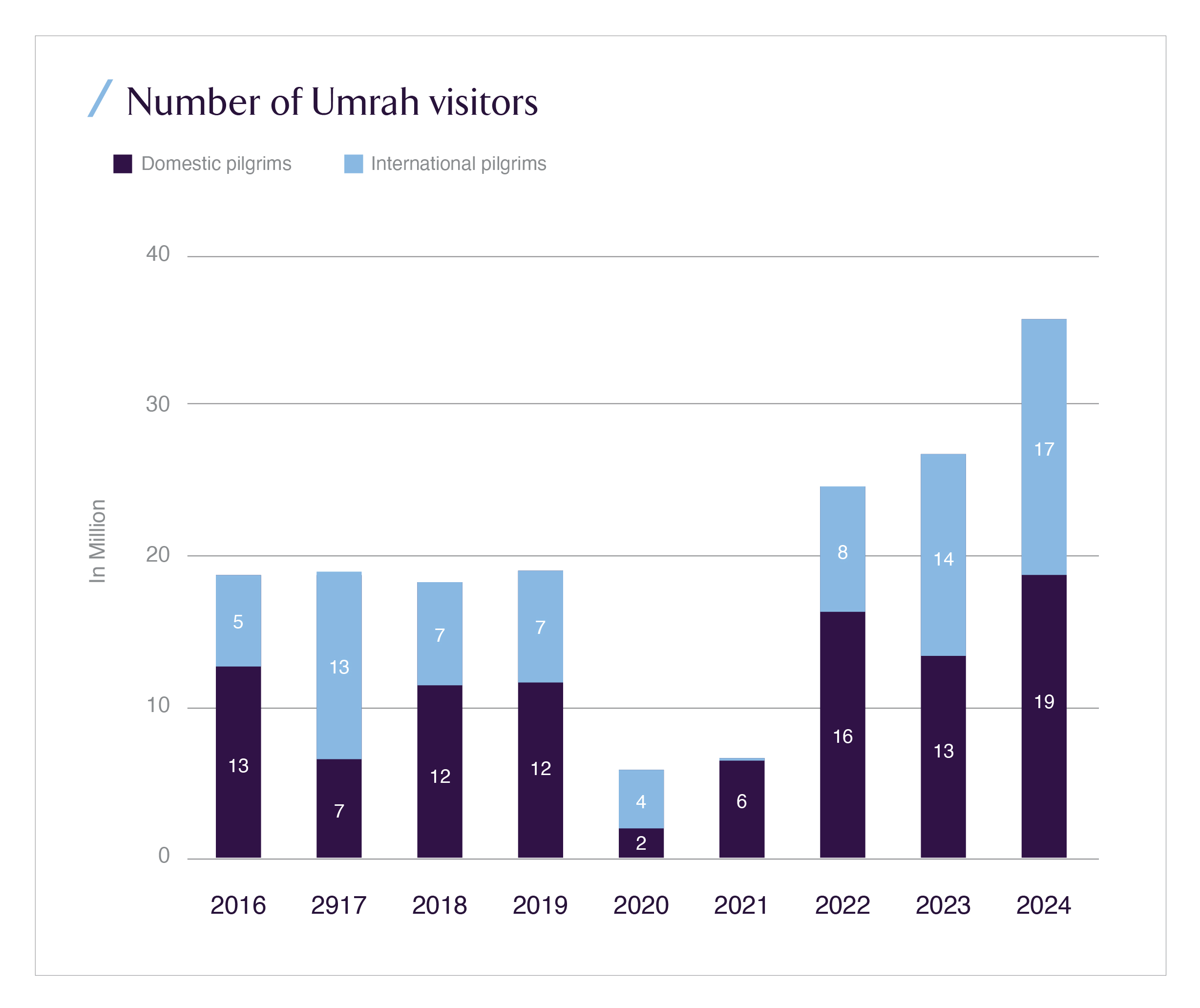

- 35.8 million Umrah pilgrims in 2024, domestic + foreign, the highest ever recorded, with 18.5 million from abroad.

- Around 2 million Hajj pilgrims in 2024; 2025 quotas have been raised again, implying further growth.

- An official target of 30 million Umrah pilgrims annually by 2030, and 150 million total annual visits.

If you strip out the handful of USD 2,000 per night rooms on remote islands, the average Saudi trip is not ultra luxury. It is:

- a family from Jeddah driving to Taif for a weekend;

- an Umrah pilgrim from Indonesia or Pakistan combining a few nights in Makkah and Madinah with short domestic excursions;

- regional visitors from GCC countries staying in 3 or 4 star branded hotels near business districts or malls.

WTTC now describes Saudi as one of the fastest growing tourism economies in the world, with the sector expected to inject SAR 447.2 billion into GDP in 2025 and support 2.7 million jobs. At the same time, Renub and other market researchers expect the Saudi hotel market to grow from USD 15.4 billion in 2024 to roughly USD 27.3 billion by 2033, a 6.5% CAGR.

The demand engine is therefore broad based, recurring and price sensitive. The supply engine, until now, has been narrow, premium, and capex heavy.

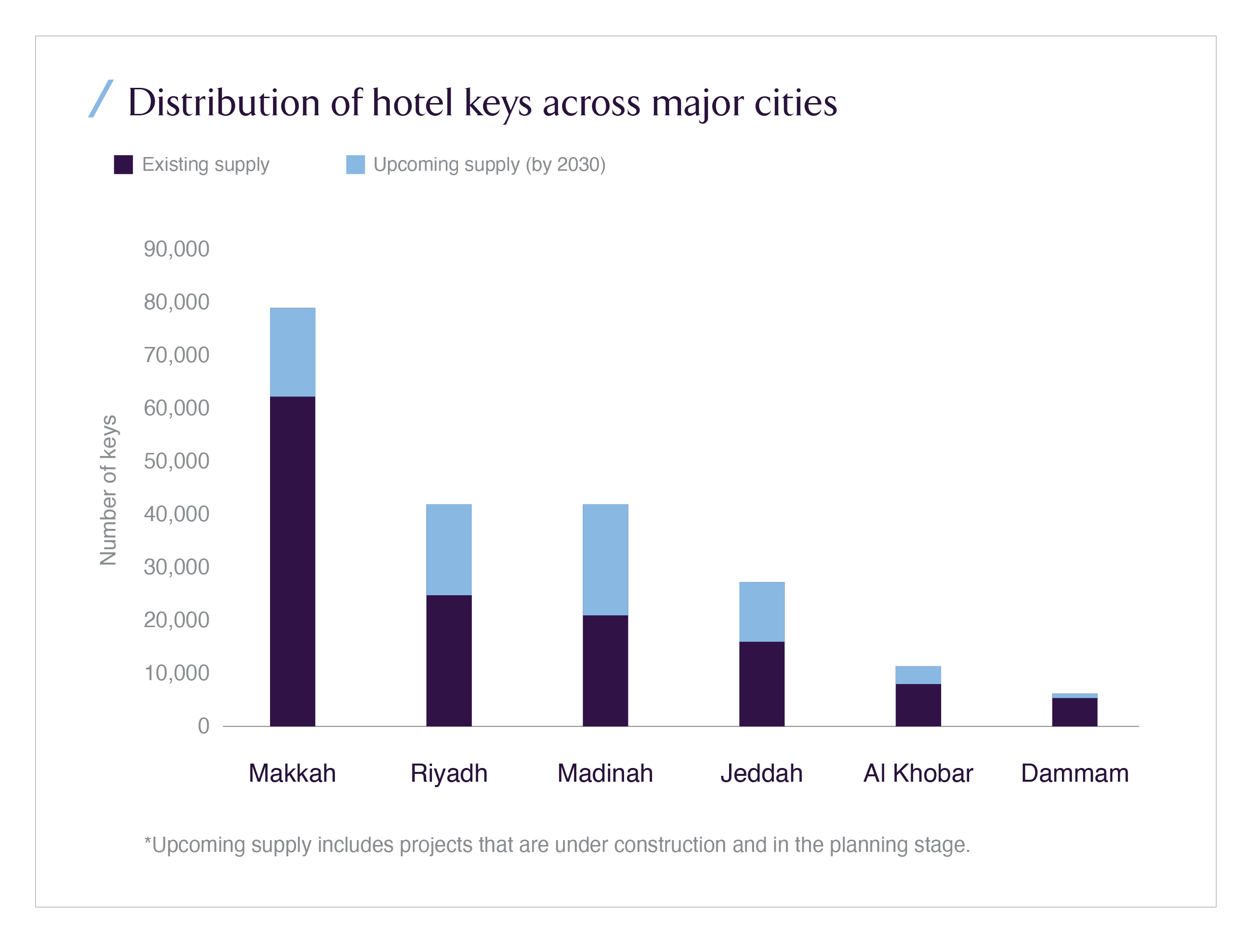

Where the Keys Are Today: Geographic and Segment Imbalance

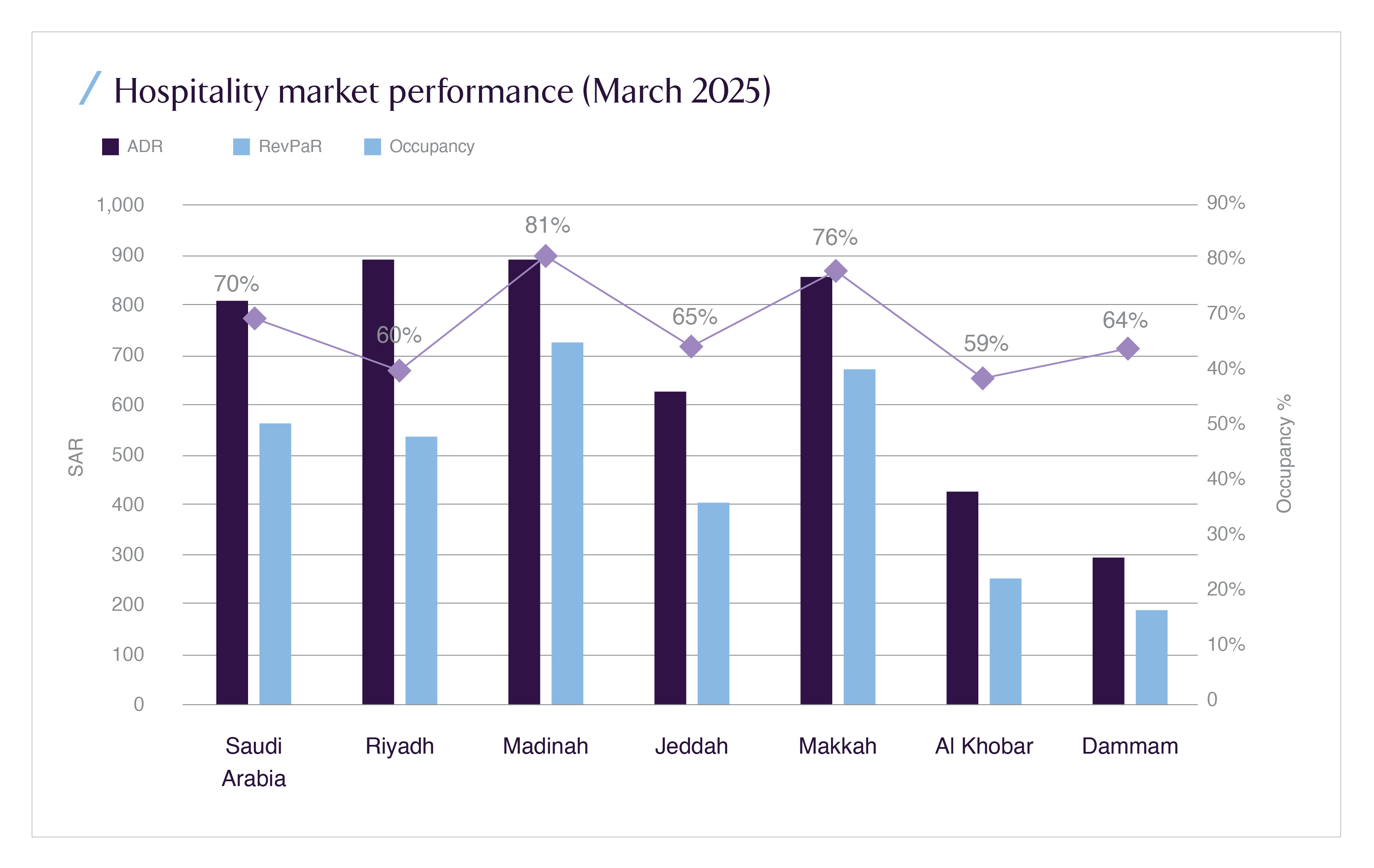

Within the current hotel stock, geography matters as much as segment. Knight Frank’s 2025 infographic shows both an occupancy step up in religious cities and a key concentration in Makkah and Riyadh:

- National average occupancy around 70% in 2024.

- Madinah at roughly 81% occupancy, Makkah 78%, versus ~60–65% in Riyadh and Jeddah and sub 60% in Al Khobar.

- Key counts heavily concentrated in Makkah and Riyadh, followed by Madinah and Jeddah, with Eastern Province cities still relatively under supplied.

Overlay that with segment data (luxury vs upper mid vs mid), and a clear picture emerges:

- Religious cities already run at very high occupancy on peak dates and relatively tight occupancy off peak.

- The giga project pipeline in Makkah and Madinah alone exceeds 252,000 keys by 2030, with 64% of under construction / planned keys in the Holy Cities in 4 and 5 star categories.

- New PIF backed projects such as the Al Balad Development Company’s USD 3.6 billion hospitality portfolio in historic Jeddah will add 3,300 units spanning mid scale to luxury, but again with a heavy emphasis on prime, heritage linked locations.

In short: the metros and holy cities are attracting huge volumes of visitors, but the physical product is still disproportionately four and five stars. If Saudi Arabia wants to welcome 150m+ visitors by 2030 without pricing out the middle of the global and domestic market, the supply mix has to change.

The 2026 Pivot: From Signal to Operating Mandate

The November 2025 Reuters interview with Minister Al Khateeb effectively formalised what many in the market had anticipated:

- Saudi will build more mid and upper mid range tourism options, not just ultra luxury.

- Part of that push is explicitly aimed at expanding affordable hotel access for religious pilgrims.

- Ten “cost effective” resorts are planned for Shebara Island to sit alongside ultra luxury properties, with a broader ambition to attract 150 million visitors annually by 2030, one third from abroad.

For 2026, that becomes an operating mandate for investors and developers:

- Red Sea and NEOM assets can no longer be modelled purely as luxury only enclaves; they need rate ladders that capture affluent but not ultra rich segments.

- Religious tourism platforms in Makkah, Madinah, and Jeddah have to expand room counts in 3 and 4 star formats that can price nights in the SAR 300–600 range, not only SAR 1,200+.

- Secondary cities and transit hubs Al Ahsa, Taif, Abha, Qassim must build enough mid market capacity to spread demand beyond the holy city and Riyadh/Jeddah axes.

This pivot also dovetails with policy levers already in motion:

- A proposed Schengen style GCC visa for 2026–27, which could make Saudi part of multi-country itineraries and increase the importance of mid-market city stays.

- Ongoing investments in low cost carriers and airport expansion, which naturally bring in more price sensitive travellers.

For capital, the question shifts from “where is the next trophy resort?” to “where can mid market product produce resilient ADR × occupancy at scale?”

Challenges: Getting Mid Market Right Is Not Trivial

The pivot is strategically sound, but the execution risk is real. Three constraints stand out.

1. Brand Architecture and Positioning

Many of the international operators leading the pipeline Marriott, Hilton, Accor, IHG, Radisson already have midscale and select service brands in their global portfolios. The challenge is to position those brands in Saudi so they feel aspirational for domestic middle class households and acceptable for international pilgrims, without cannibalising higher end flags in the same city.

2. Development Economics Under Higher Rates

Mid market does not mean low capex in Saudi. Land in Makkah, Madinah and central Riyadh is expensive; construction costs are elevated; and lenders are still adjusting to global rate cycles. Developers need products that can deliver attractive yields at more modest ADRs, which implies tight control over build cost, operating efficiencies, and financing structures.

3. Demand Segmentation and Seasonality

Religious tourism is inherently spiky, peaking around Ramadan, Hajj, school holidays and long weekends. The mid market segment must be able to handle sharp swings in occupancy and average length of stay without destabilising P&Ls. That requires more sophisticated revenue management, targeted regional marketing in off peak windows, and potentially mixed use structures (e.g., combining hotel and branded residence inventory).

Solution Pathways: How Capital and Policy Can Align

From an investor and policymaker perspective, the 2026 shift opens several concrete solution spaces.

1. Rebalancing the Pipeline at the Margin

The Knight Frank data show that existing and planned supply is still dominated by high end categories. Rebalancing does not require cancelling luxury product; it requires tilting incremental approvals and incentives toward mid market:

- Tourism Development Fund (TDF) and PIF vehicles can offer better terms for upper midscale and midscale projects in undersupplied corridors and religious tourism catchments.

- Mega project masterplans can create quota-like targets for mid market keys relative to luxury keys, especially in nodes near transport hubs, staff accommodation and service corridors.

Because the base pipeline is so large, even a 10–15 percentage point shift in the mix of new approvals can materially increase the number of mid market keys by 2030.

2. New Asset Typologies

Mid market in Saudi does not need to copy European 3 star norms. There is room for hybrid formats tuned to local demand:

- Compact, efficient hotel rooms co-located with large prayer facilities, shared kitchens and family lounges for pilgrims.

- Serviced apartment style mid market properties in secondary cities, aimed at domestic families and long stay regional visitors.

- Dual brand hotels stacking an upscale and an upper midscale product vertically on the same site, sharing back of house to improve margins while segmenting rates and guests.

Such typologies can be more land and capex efficient than fully standalone properties, yet still deliver differentiated price points.

3. Capital Structures for Volume Segments

On the capital side, structures that work for trophy resorts may be sub optimal for mid market portfolios. More suitable playbooks include:

- Income focused REITs or private funds aggregating mid market properties in religious and secondary cities, targeting stable cash yields rather than pure capital gains.

- PPP models where land is contributed by public entities (municipalities, royal commissions, Awqaf institutions) and private investors fund construction and operation in return for long term leases.

- Shariah compliant Sukuk and project finance structures that spread risk over clusters of properties rather than single assets, lowering unit financing costs.

These structures align more naturally with the economics of SAR 300–600 ADR products and high occupancy, rather than relying on ultra premium nightly rates.

Investor Benefits: Why “Beyond Luxury” Improves the Risk–Return Profile

For Saudi and international investors, the move into mid market is not philanthropy; it enhances portfolio characteristics.

1. More Resilient Cash Flows

Luxury segments are high margin but cyclical. Mid market and religious tourism products are volume businesses: they hold up better in downturns, as travellers trade down rather than cancel. For a country that wants travel & tourism to be >10% of GDP, having a diversified hospitality base is a macro stability play.

2. Deeper Domestic Participation

Mid market assets, especially smaller hotels and serviced apartments are more accessible tickets for local and regional investors than multi billion riyal mega resorts. This supports domestic capital market deepening, SME participation, and broader wealth effects.

3. Stronger Alignment with Religious Tourism Strategy

Most pilgrims are not luxury travellers; they are cost conscious households from across the Muslim world. An asset base that matches their budget range and visit patterns will better support the target of 30 million Umrah pilgrims and larger Hajj quotas, while preserving affordability and social licence.

4. Enhanced International Perception

For many visitors, the first Saudi hotel they experience will not be a USD 2,000 per night island villa; it will be a room near a mosque, a city centre mall, or an airport. A robust, well managed mid market segment therefore becomes a soft power instrument: it shapes the lived experience of millions of visitors per year, not just the top percentile.

Recap: Mid Market as the Load Bearing Layer of Vision 2030 Tourism

By January 2026, Saudi tourism will still have some of the most ambitious luxury projects on the planet. But if officials follow through on the signals they sent in November, the load bearing layer of the Kingdom’s tourism strategy will increasingly be mid and upper mid market supply.

The data already show why this is necessary:

- Global tourism is back at or above pre pandemic levels, but the growth edge is in value conscious segments.

- Saudi’s own demand is overwhelmingly domestic and religious, with tens of millions of pilgrims and family travellers each year.

- The hotel pipeline, by contrast, remains skewed to high end categories, especially in giga projects and holy city developments.

The 2026 pivot “beyond luxury” is therefore both a risk management move of concentrating exposure away from a narrow luxury band and a growth strategy that ensures the Kingdom’s targets of 150 million visitors and 30 million Umrah pilgrims have a realistic physical foundation.

For investors, the opportunity is to design vehicles, partnerships, and product typologies that:

- lean into mid market and upper mid segments in high demand corridors;

- use smarter capital structures and PPP models to make the economics work at lower ADRs;

- and treat Saudi tourism not as a string of trophy assets, but as a diversified, policy backed, volume business with global scale demand.

That is the essence of the shift now underway and why mid market, not just luxury, will determine whether Saudi tourism becomes a durable, investment grade pillar of the national portfolio.