Overview: From “Find Me Space” to “Reserve It Before It Exists”

At the top end of Saudi Arabia’s office market, the numbers are blunt. By Q3 2025, Riyadh’s Grade A headline rents had climbed to around SAR 2,750 per square metre per year, up more than 15% year on year, with occupancy at roughly 98%. Grade B followed closely, with mid 90s occupancy and strong rental growth of its own.

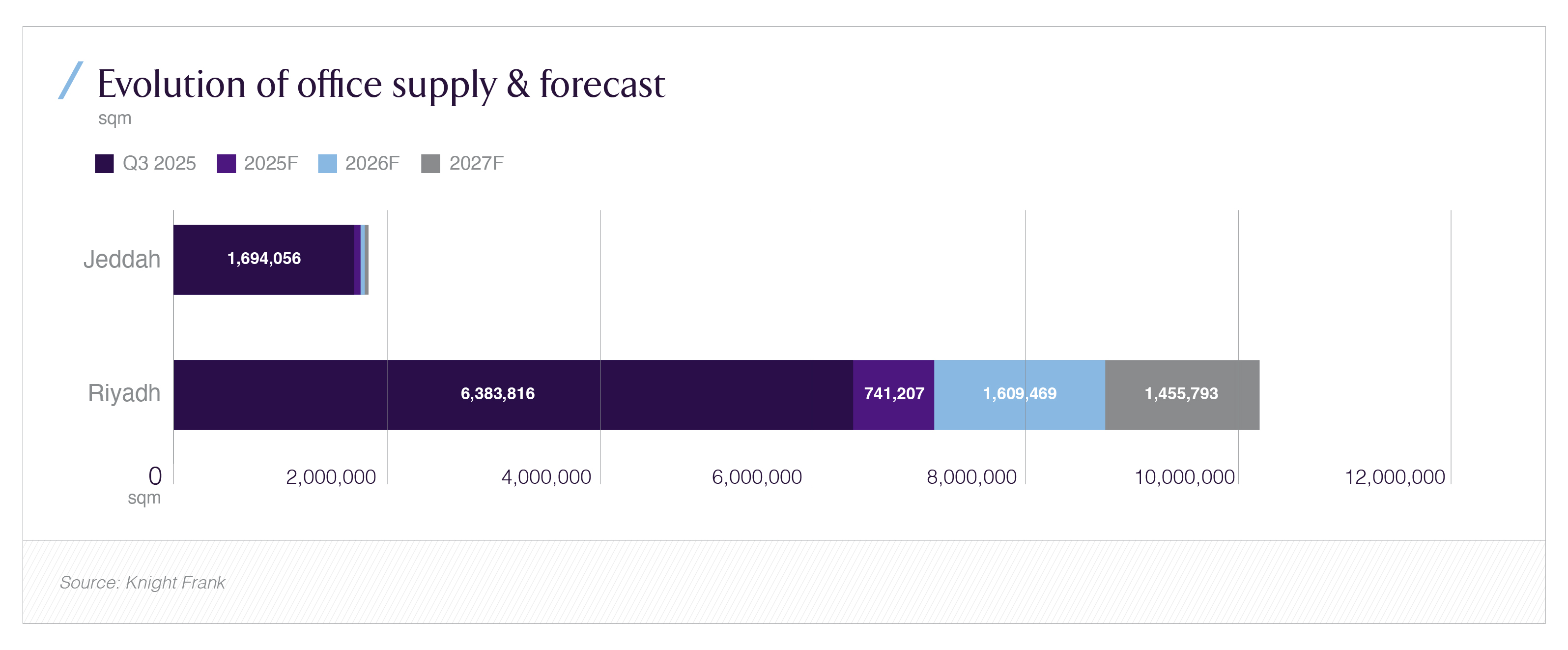

At the same time, Knight Frank estimates that total office stock across Riyadh, Jeddah, and the Dammam Metropolitan Area will rise from roughly 9.7 million sqm in 2025 to about 15 million sqm by 2028, with Riyadh accounting for nearly half of that pipeline. In other words, the capital city is simultaneously almost full and about to absorb one of the region’s largest waves of new office supply.

That cocktail near zero vacancy, double digit rent growth, and an accelerating development pipeline is exactly what shifts leasing behaviour. Occupiers increasingly commit to space before it is built. Developers rely on forward commitments to de risk projects and secure finance. And investors no longer evaluate Grade A offices purely on “today’s rent” and “today’s yield,” but on pre lease depth, tenant mix, and the quality of the forward pipeline.

Riyadh’s Grade A office story has therefore become a story about pre leasing and pricing power: who can lock in the next generation of tenants, at what rents, on what terms, and how long that advantage lasts before new supply resets the balance.

Global Backdrop: Prime Offices Under Pressure, but Flight to Quality Survives

Globally, office markets are still digesting hybrid working, higher interest rates, and a large stock of older, non ESG compliant buildings. Colliers’ EMEA prime office rent index continued to rise in Q2 2025, but at a slower pace, up 5.8% year on year with an aggregate vacancy rate of about 9.1%, above the long term average.

Within that aggregate, the pattern is uneven. Many markets are tenant favourable, with landlords offering rent free periods and fit out incentives. But in a small group of cities, Paris CBD, Dubai, Abu Dhabi, Riyadh, Cairo, prime CBD rents have been growing much faster than the regional average, underpinned by limited supply of truly best in class buildings and strong corporate demand.

For institutional allocators, the implication is simple: office risk is no longer a single asset class bet. It is a split market: structurally challenged secondary stock in some Western cities versus tight, growth driven Grade A clusters in a narrow set of global hubs. Riyadh sits clearly in the latter camp for now.

Regional GCC Context: Tight Prime Space, Competitive Pipelines

Across the GCC, prime and Grade A office markets have been supported by diversification programmes and regional headquarters mandates. In the UAE, for example, both Dubai and Abu Dhabi have recorded robust demand and rent growth in prime districts, with limited new stock and persistent pre leasing in upcoming towers.

Saudi Arabia’s office markets share some of these features, but at larger scale. Knight Frank’s GCC Office Market Review 2025 highlights three themes for the Kingdom:

- Government led investment and giga projects driving corporate expansion

- A strong preference among occupiers for modern, ESG aligned Grade A space

- A development pipeline that could nearly double stock in key markets by 2028

Within that national picture, Riyadh has emerged as the epicentre of corporate demand. In 2024 alone, more than 14,000 foreign business licences were issued, and over 675 to 780 multinational firms have either established or announced regional headquarters in the capital under the RHQ Programme. That demand concentrates pressure on a finite set of Grade A nodes: King Abdullah Financial District (KAFD), The Business District, Digital City, Granada Business Park, Laysen Valley, among others.

Riyadh’s Grade A Market: Squeeze, Submarkets, and the Pre Leasing Imperative

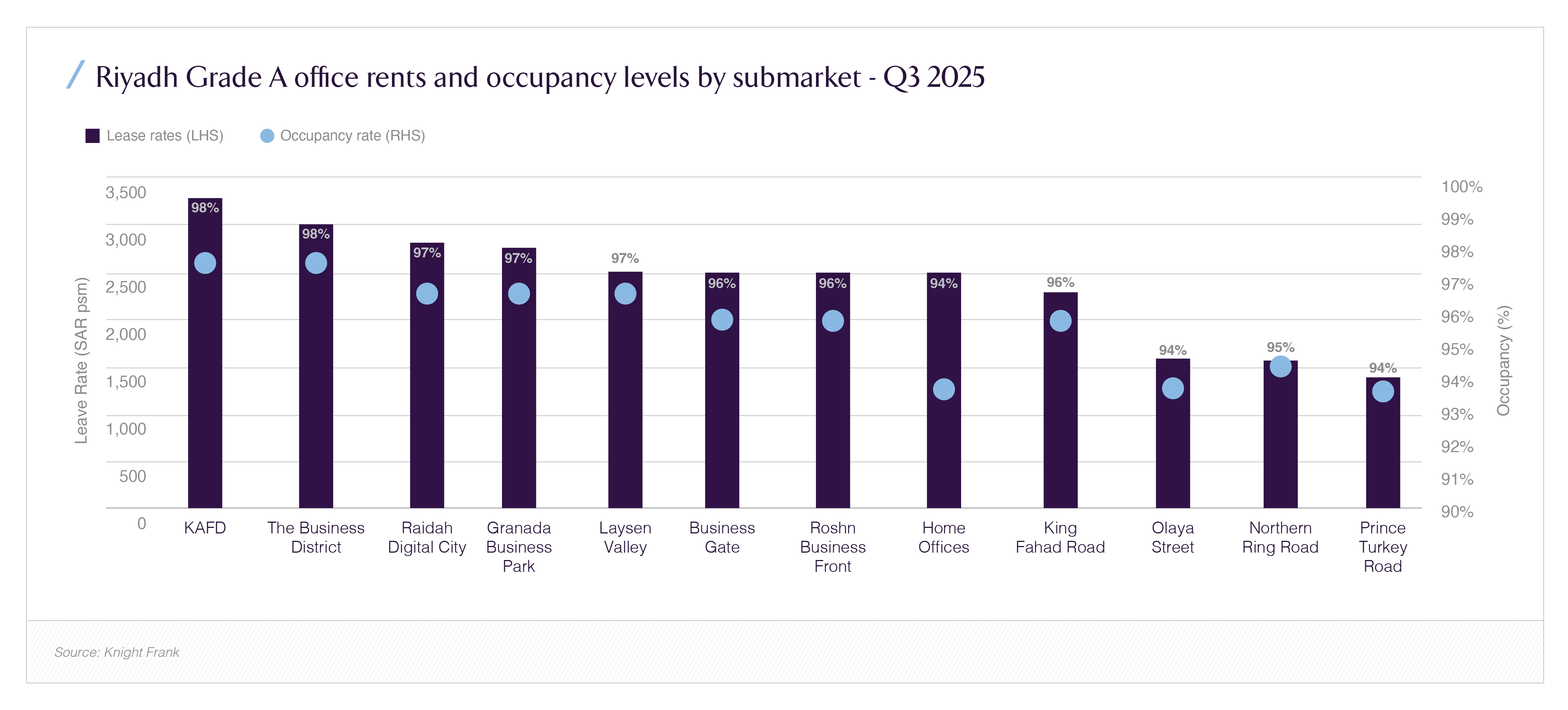

By Q3 2025, the pressure in Riyadh’s Grade A market is very visible in the submarket data. Knight Frank’s breakdown of rents and occupancy by district shows KAFD and other leading clusters operating in the mid 90s to near 100% occupancy range, with headline rents clustered between roughly SAR 2,500 and SAR 3,500 per square metre per year.

This multi year chart captures two points relevant for investors:

- Persistent outperformance of Grade A rents in Riyadh compared with Jeddah, reflecting the capital’s role as administrative and corporate hub

- Accelerating growth from 2021 onwards, culminating in strong year on year increases into 2024 and 2025 as Vision 2030 projects and RHQ migration intensified

A second view, submarket level rents and occupancy, shows how narrow the truly liquid Grade A segment is inside the metropolitan area.

In that chart, only a handful of nodes combine top quartile rents with about 98% occupancy. This is where the pre leasing battle is concentrated:

- Multinationals and government linked entities are consolidating into these clusters, often negotiating multi floor, long duration leases

- Developers with shovel ready projects nearby are increasingly unable to rely on “lease it when it opens” strategies; they are signing large anchor tenants during design and construction phases

- CBRE’s Saudi outlook describes Riyadh’s office market as having a headline occupancy rate of around 98.1% in Q4 2023, with limited immediate stock and elevated pre leasing activity in pipeline schemes, conditions that have persisted into 2024

Combined with Knight Frank’s Q3 2025 data, the message is consistent: if you want Grade A space in the right submarket, you have to reserve it early.

At the same time, the development pipeline is significant. This chart shows Riyadh’s stock stepping up materially between 2025 and 2027, mirroring Knight Frank’s national forecast of roughly 15 million sqm across major markets by 2028. For investors, this sets the clock: current scarcity is genuine, but it is not permanent. Pre leasing and pricing power are strongest before this new wave fully hits.

Saudi Investor Lens: Where Does the Risk Actually Sit?

From a Saudi allocator’s perspective, whether family office, REIT, or institutional fund, the Grade A office squeeze in Riyadh raises three categories of risk.

1) Timing Risk: Buying at the Top of a Tight Cycle

Rents in the capital have climbed sharply. Knight Frank notes an 86% cumulative rise in Grade A rents since 2019, with an additional 10% to 15% uplift in some locations just ahead of the recent five year rent freeze announcement. CBRE and JLL data from 2023 and 2024 similarly show double digit annual increases off a low vacancy base.

Paying peak prices for standing stock is defensible only if:

- the lease profile is long and secure

- tenants are high quality (RHQs, blue chip corporates, government linked entities)

- the building’s ESG and technical specs will still qualify it as core once the new pipeline is delivered

Otherwise, investors risk buying late cycle cash flows that will need aggressive capex or rent resets when newer assets arrive.

2) Concentration Risk: Demand Tied to Vision 2030 and RHQs

The demand story, giga projects, foreign RHQs, FDI, is obviously attractive. But it is also concentrated. Roughly 51% of Saudi’s office real estate market value is in Riyadh, with banking, financial services, and insurance alone accounting for about 31% of overall office demand in 2024.

If capex cycles on mega projects are rephased, or if global corporates reshuffle their regional footprints, leasing decisions can slow quickly. That does not imply a structural reversal, but it does mean investors must avoid over exposure to a single district, tenant cluster, or project sponsor.

3) Obsolescence Risk: Grade B and “Almost Grade A” Stock

As newer towers complete, often with higher ESG ratings, better floor plates, and stronger amenity packages, pressure will build on older stock that sits between true Grade A and functional Grade B. Some of this inventory may require upgrades; some may drift into permanent discount territory.

For investors, the question is not simply “Grade A or not?” but:

- Can this building still compete for RHQ type occupiers in 2028 to 2030?

- Or is its natural role shifting toward mid tier tenants, with lower rents and more generous incentive packages?

How Pre Leasing Is Reshaping Deal Structures

With scarcity in prime nodes and a visible pipeline, pre leasing is no longer a side note in term sheets, it is central to project economics.

In practical terms, the pre leasing trend in Riyadh is showing up as:

- Forward commit anchor leases: Large occupiers committing to 30% to 50% of a building’s GLA two to three years before completion, often with phased occupation rights

- Design influenced leases: Tenants locking in specifications (HVAC sizing, floor loading, data risers, ESG features) at shell and core stage, trading higher headline rent for customised configuration

- Tighter covenant requirements from lenders: Banks and credit investors increasingly requiring a minimum pre lease coverage ratio (for example 60% to 70% of GLA or rental income) before fully releasing project financing

For landlords, this strengthens pricing power today but introduces a different constraint: deliverability. Missing handover dates or failing to achieve agreed fit out performance can now directly impact creditworthiness, not just tenant relationships.

For occupiers, pre leasing is a hedge, locking in space and rent levels in clusters where Grade A options may otherwise be unavailable for years. But it also commits them to a long term view on Riyadh headcount and Saudi market exposure.

Strategic Plays for Saudi Investors

Given this backdrop, what are the more technical moves available to Saudi investors, rather than simply “buy Grade A at any price”?

- Forward fund or co develop, not just buy stabilised assets. Participating earlier in the capital stack (with clear pre lease thresholds) allows investors to benefit from development margins while still targeting core plus outcomes once schemes stabilise.

- Prioritise submarkets with durable demand triggers. Districts anchored by policy programmes (RHQ, financial services, digital economy) and strong transport and amenity access, KAFD, key King Fahd Road nodes, Business Gate, and similar, are more likely to maintain pre leasing depth across cycles.

- Underwrite break clauses and option value explicitly. In a pipeline heavy environment, tenants will push for flexibility. For investors, the modelling needs to assign real option value (positive or negative) to breaks, expansions, and contraction rights.

- Stress test rents and cap rates against the 2028 stock level. With total Saudi office GLA potentially nearing 15 million sqm by 2028, the right question is not “What’s the rent today?” but “What rent and yield are sustainable once the pipeline is fully digested?”

- Consider mixed use and ESG heavy formats as risk mitigation. Assets with hospitality, retail, or experiential components aligned with global ESG expectations are better placed to defend rents if pure office demand softens at the margin.

Benefits If You Get It Right

If investors navigate the timing, concentration, and obsolescence risks carefully, Riyadh’s Grade A squeeze offers several structural advantages:

- High visibility on demand. Vision 2030, giga projects, and RHQ migrations are not one year phenomena. They underpin decade long demand for high quality corporate space.

- Long duration, quality covenants. Many pre lease deals involve large multinationals, financial institutions, and government linked entities, offering covenant strength closer to infrastructure type assets than traditional cyclical offices.

- Embedded repricing options. Even when rent freeze rules moderate further headline growth, investors can still capture value via tenant upgrades, reconfigurations, and the repricing of older leases when they eventually roll off.

- Potential for yield compression from global capital. As international investors reweight toward growth hubs with strong demographic and policy tailwinds, Riyadh’s Grade A assets could benefit from additional cap rate compression over the medium term, particularly those with demonstrable ESG credentials and pre lease depth.

Recap: Pricing Power Today, Portfolio Discipline Tomorrow

Riyadh’s Grade A office market has moved from a simple landlord’s market, “we’re full, rents are rising,” to a more complex strategic phase:

- Occupancy near 98% and strong rent growth into 2025 reflect genuine scarcity in the right submarkets.

- A significant pipeline, however, is on track to lift total Saudi office stock to around 15 million sqm by 2028, with Riyadh at the core of that expansion.

- Pre leasing is now the bridge between these two states: it monetises today’s scarcity while underwriting tomorrow’s supply.

For investors, the game is no longer just about finding any Grade A. It is about choosing the right node, structure, and timing, making pre lease coverage and asset quality central to every investment case.

Handled carefully, Riyadh’s Grade A squeeze can be a source of durable, policy aligned cash flows for Saudi portfolios, with pre leasing used not as a buzzword, but as a disciplined risk management tool.