For two decades, the education trade in Saudi Arabia has been shorthand for “universities and K 12.” Today, the more investable story sits in the middle: technical and vocational education and training (TVET).

Three dynamics have shifted the center of gravity toward TVET:

- Vision 2030’s labor market mandate: TVET is explicitly tasked with absorbing as many Saudis as possible into job relevant programs and closing skills gaps, with a 2008 to 2030 strategic plan oriented around capacity expansion, employer alignment, and PPPs.

- Evidence that the workforce pipeline is actually moving: graduate employment rates and job placements have risen sharply since 2016, with vocational tracks playing a visible part in the Human Capability Development Program’s results.

- Data showing TVET is no longer marginal: specialist market research and national statistics point to a fast growing TVET spend base, hundreds of institutions, and sizeable annual graduate cohorts.

For Saudi allocators, that reframes TVET from “social overhead” into a scaled, policy backed deployment channel for human capital and infrastructure capital, and one whose operating loops are structurally faster than the traditional university path.

This article reads TVET as an investable system rather than a social program: we walk through global and regional context, the current Saudi build out, the constraints that matter, and the levers that can turn policy into measurable returns, whether you are backing equity, private credit, or quasi sovereign vehicles.

Global and GCC Landscape: From Degrees to Skills Loops

Globally, the post pandemic education narrative has shifted from credentials to skills and time to employment. Governments in Europe, Asia, and the GCC are converging on a similar architecture:

- Short cycle, modular TVET to plug immediate gaps in manufacturing, construction, digital, energy, and health.

- Dual and apprenticeship models tying classroom learning to paid work.

- PPP structures where employers and training providers co design curricula and co fund facilities.

For investors, that means TVET markets look more like hybrid infrastructure and B2B services than traditional education pure plays. Revenue is often anchored by public budgets, but delivery and innovation are pushed heavily toward private operators and platform providers.

Within the GCC, education demand remains structurally strong. Alpen Capital projects student numbers in the region rising from around 14.0 million to 15.5 million between 2024 and 2029. But the composition of capacity is changing. K 12 and university projects still dominate headlines, yet the policy detail increasingly talks about TVET as the instrument for aligning human capital with diversification sectors: tourism, logistics, manufacturing, renewables, and digital.

Saudi stands out as the system that has pushed TVET furthest into the center of its national economic plan.

Market Signals: TVET vs Higher Education as Asset Buckets

Two datasets from Grand View’s Horizon platform help frame TVET as a distinct market alongside higher education rather than a subset.

Analysts estimate that the Saudi technical and vocational education market generated around US$11.1 million in revenue in 2024, with projections to reach roughly US$20.6 million by 2030, implying a CAGR of about 10.9% for 2025 to 2030.

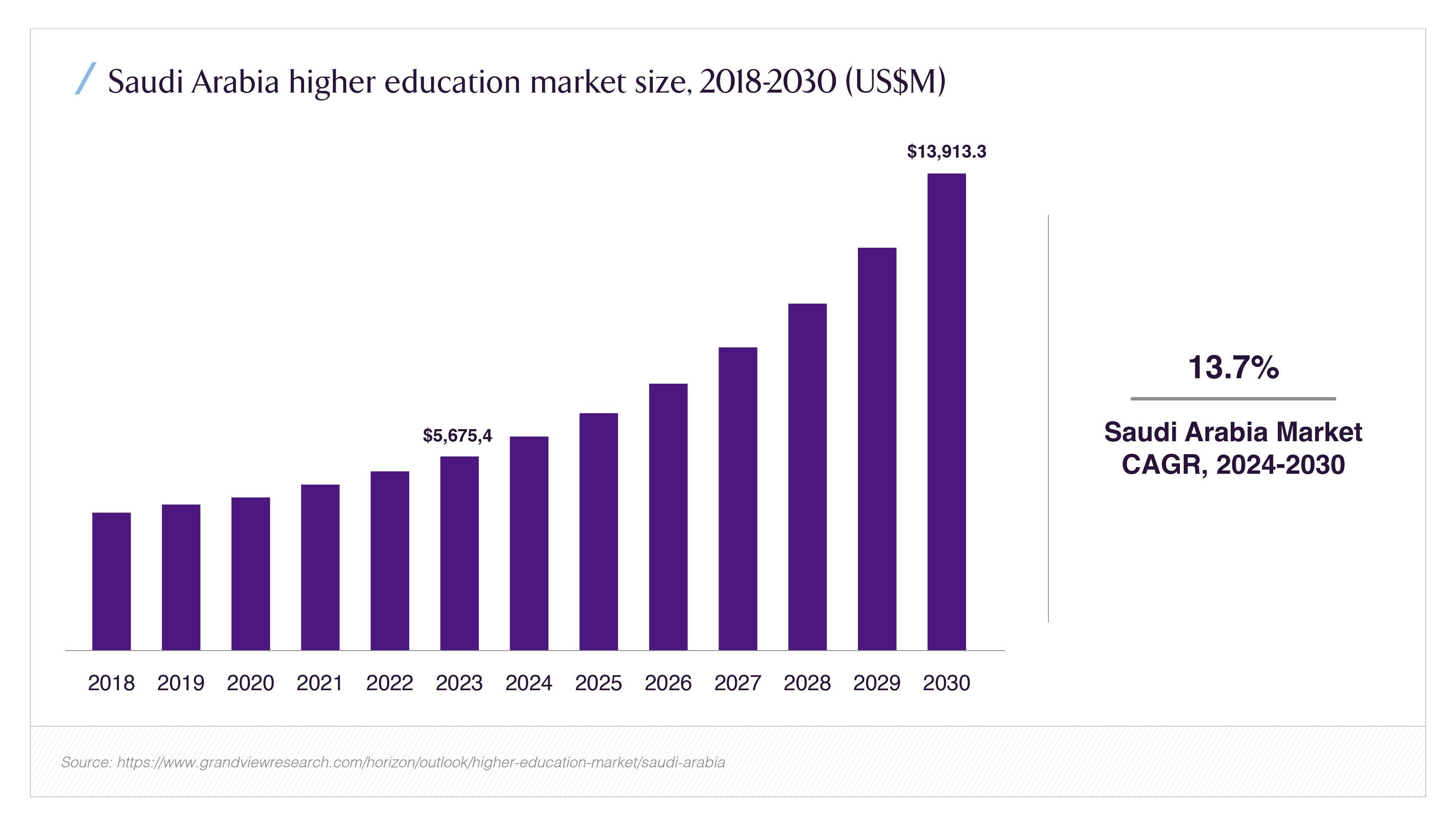

By comparison, the higher education market in Saudi is far larger in absolute terms, roughly US$5.7 billion in 2023, rising to about US$13.9 billion by 2030, at an estimated CAGR of 13.7% for 2024 to 2030.

On a pure revenue basis, universities still dominate. But from a policy and system design standpoint, three points matter for investors:

- TVET is growing from a smaller base, which means incremental capacity, new colleges, academies, and PPP campuses, translates directly into visible percentage shifts in national outputs (graduates, placements, sector specific skills).

- TVET programs are shorter and more modular, which shortens the loop between policy, capital deployment, and measurable labor market impacts.

- The market metrics above mostly capture spend, not outcomes, like job placement or productivity; TVET’s edge is in the latter.

.png)

Side by side, these two visuals do not negate the investment case for universities; instead, they highlight that TVET’s relative impact per riyal of incremental capital is likely higher, because it is being explicitly tasked with absorbing non university pathways and mid career upskilling, not just traditional school leavers.

Saudi’s TVET Scale Up: Capacity, Coverage, and Specialization

The Core System: TVTC’s National Footprint

The Technical and Vocational Training Corporation (TVTC) is the central engine of TVET expansion. Its published strategy explicitly targets accommodating the largest possible number of learners, aligning programs with quantitative and qualitative labor market demand, and deepening partnerships with the private sector.

Recent operational data shows what that ambition looks like in practice:

- 336,150 trainees enrolled across TVTC affiliated institutions in 2024, with 98,716 graduates in the same year.

- These programs were delivered through 314 institutions, including 148 technical colleges, 99 secondary and architecture or industrial institutes and prison training units, 61 strategic partnership institutes, and 6 international technical colleges.

For investors, these numbers matter as a proxy for absorptive capacity. A system that can process more than 300,000 trainees a year and graduate nearly 100,000 is a system where relatively modest capex on facilities, dorms, digital platforms, or specialized labs can translate into large, repeated human capital outputs.

The Global Academy Layer: TVET as a PPP Network

One of the clearest signs that TVET is moving faster than universities is the speed with which TVTC has embedded global technology brands directly into its colleges.

By December 2024, TVTC reported that 151,326 trainees were enrolled in international academies hosted inside technical colleges, across five global academy networks: Microsoft, Cisco, Oracle, Huawei, and SAP. These operate through 216 academy branches, staffed by more than 1,209 specialized trainers, and feed into 407 accredited professional certifications across 14 fields.

This is not just using vendor curricula. It is a structural choice: instead of waiting for universities to redesign degrees, the system is wiring vendor level skill standards directly into technical colleges.

From an investment standpoint, this is not just a nice visual; it quantifies:

- Scale of global academy participation (hundreds of thousands of learners).

- Breadth of sectors covered (IT, cloud, networking, ERP, cybersecurity).

- Depth of the PPP model (multiple global vendors embedded in the same public network).

It also underscores why TVET is a natural front door for corporate and private equity backed academies in tourism, logistics, construction, manufacturing, and healthcare. The governance and integration model already exists.

Inclusion and Specialized Tracks

Another sign that TVET is scaling faster at the system level is its ability to absorb diverse learner profiles that universities may struggle to serve at scale.

In December 2024, TVTC reported 691 trainees with disabilities currently enrolled in technical colleges and industrial secondary institutes, with 355 graduates with disabilities in the prior year, supported by tailored programs, sign language interpreters, and specializations such as office applications and computer maintenance for the hearing impaired.

While the absolute numbers are modest, they illustrate a system architecture geared toward modular program design, assistive services, and regional dispersion, properties that matter for impact oriented investors and for any future outcomes based contracting.

How TVET Is Moving Faster Than Universities

Moving faster here is not a slogan; it reflects three structural differences in how TVET interacts with the labor market compared with universities.

Time to Market and Curriculum Refresh

Most TVET programs run on one to three year cycles, with explicit mandates to track labor market demand and update specializations accordingly. TVTC frames its strategic objectives around matching quantitative and qualitative demand and expanding training in advanced fields that support national plans and technology transfer.

Universities, by contrast, operate on accreditation cycles measured in multi year increments, with far less direct employer co governance. That is changing slowly, but the governance and funding model is fundamentally different.

Direct Linkage to Employment and Entrepreneurship

The Human Capability Development Program’s 2024 annual report highlights that 44.4% of Saudi higher education graduates entered the workforce within six months of graduation in 2024, up from 13.3% in 2016, with youth employment rising from 18% to 36.2% over the same period. These gains are explicitly linked to expanded vocational training and startup support programs.

Complementing that, TVTC has reported:

- 25,171 job opportunities for TVET graduates in a single month (May 2024) through coordination with employers, plus dozens of agreements and preparation programs.

- 165 private projects created by TVET graduates in 2024 with support from the National Entrepreneurship Institute (Riyada).

The implication: TVET is wired directly into job placement flows and entrepreneurship channels, not just into academic progression. For investors assessing human capital ROI, that linkage is critical.

Infrastructure Intensity per Learner

TVET sits at the intersection of:

- Physical assets: workshops, labs, specialized equipment for mechanical, electrical, ICT, hospitality, and health trades.

- Digital infrastructure: LMS platforms, virtual labs, remote simulators.

- Partnership ecosystems: employer branded academies, assessment hubs, and certification centers.

This mix makes TVET a natural target for infrastructure plus services capital structures (for example, real assets underpinned by long term operating contracts, wrapped with software and services revenue). Universities may host similar assets, but their governance is more complex and less explicitly tied to labor market KPIs.

Challenges and Systemic Risks

For all the positive data, Saudi’s TVET scale up faces real constraints that matter both for policy and for investors.

- Quality assurance and fragmentation: Multiple entities, TVTC, the Ministry of Education, and the Education and Training Evaluation Commission (ETEC), have overlapping quality assurance roles. Coordination is improving but still a live issue, as documented in Vision 2030 delivery plans.

- Perception and social preference: Despite concerted campaigns, TVET still competes with entrenched preferences for university degrees, particularly in families who equate status with traditional professional tracks.

- Regional and sectoral imbalances: TVTC statistics show a large concentration of capacity in technical colleges and strategic partnership institutes, but less granularity on how evenly that capacity maps to emerging priority regions and sectors (tourism clusters, logistics hubs, giga projects).

- Employer execution risk: PPP academies and employer linked programs depend on sustained corporate engagement. Changes in sector cycles, tourism, construction, oil and gas services, can translate into volatility for specific tracks.

- Data transparency and outcomes measurement: While employment and enrolment stats are improving, investors still face gaps in cohort level outcomes data by region, sector, and provider, which complicates pricing of outcomes based instruments or ESG linked financing.

These constraints do not negate the thesis; they define the risk surface that capital has to be priced against.

Solution Pathways and Investor Angles

From an investor’s seat, the question is not whether TVET will expand, it already is, but how to participate in ways that align with policy and risk appetite. Several pathways are emerging.

PPP Backed Physical and Digital Infrastructure

- Campuses and specialized facilities: Build to suit technical campuses, regional training hubs, and sector specific academies (logistics, hospitality, renewable energy) under long term lease or availability payment structures backed by TVTC or relevant ministries.

- Digital platforms and content: LMS, assessment engines, simulation tools, and certification management platforms that can scale across TVTC’s 300 plus institutions and private sector partners.

These plays lean toward infrastructure funds, real asset investors, and growth stage software or platform investors.

Employer Anchored Academies and Sectoral Clusters

Multinationals and large local corporates already operate academies in technical colleges. Extending that model into new sectors (tourism, logistics, manufacturing, healthcare) opens room for:

- Capital into joint venture academies.

- Operating partnerships where investors fund capex and recoup via long term training contracts and placement fees.

This is where TVET’s faster than universities dynamic is most visible: corporates can reconfigure curricula and cohorts annually as demand shifts.

Outcomes Oriented and Human Capital Financing

As data quality improves, Saudi TVET could support:

- Income share or salary linked financing products for specific skill tracks (cybersecurity, cloud, advanced manufacturing).

- ESG or impact linked instruments tied to KPIs such as female participation, youth employment, or inclusion of people with disabilities.

The existing evidence on graduate employment and job placements, combined with TVTC’s ambitions around expanding advanced training fields, creates a pipeline of measurable indicators that can be embedded in such structures.

Benefits for Saudi Investors: Why This Matters Now

For Saudi allocators, family offices, sovereign and quasi sovereign funds, banks, and corporate investors, TVET offers a combination that is unusually attractive:

- Policy tailwinds are explicit and long dated: TVET is baked into Vision 2030, the Human Capability Development Program, and sector specific strategies, not just education plans.

- Demand is structurally underserved: even with 336,000 plus trainees in 2024, TVET still captures a minority of potential learners; targets to attract a higher share of high school graduates signal further growth.

- Returns are multi layered: physical assets with quasi sovereign tenants, software and platform upside, and labor market outcomes that feed directly into productivity and consumption.

- Alignment with Saudi economic diversification: tourism, manufacturing, logistics, digital, renewable energy all rely on mid skill and technician roles that TVET is uniquely positioned to supply.

In portfolio terms, TVET can sit at the intersection of:

- Real estate and infrastructure: through purpose built campuses and training centers.

- Private equity and growth: via platform providers, content businesses, and academy operators.

- Private credit and structured finance: through asset backed or outcomes linked lending to operators and PPP vehicles.

Recap: Key Questions for Allocators

Saudi’s TVET expansion is no longer a soft, long dated story. It is a live, data supported system with measurable throughput, global partners, and clear policy backing.

The workforce pipeline is moving faster than universities in the sense that:

- Programs are shorter, modular, and tightly wired to labor market demand.

- Employer partnerships, international academies, and PPP structures give TVET a direct line into job creation and entrepreneurship.

- Capacity expansion, new colleges, specializations, and digital platforms, can be translated into human capital outputs on a one to three year horizon, not a decade.

For Saudi investors, the core questions are no longer if or whether TVET will grow, but how to position capital:

- Which parts of the TVET stack, campuses, digital platforms, academies, financing structures, fit your risk return profile and mandate?

- How will you price policy risk, employer concentration, and data transparency when structuring deals?

- What blend of impact and financial metrics will you use to judge success in this segment between now and 2030?

The answers to those questions will determine whether TVET becomes simply another budget line in public accounts or a core, repeatable allocation theme in Saudi portfolios.