Why 2026 Medical Inflation Matters for Saudi Capital

January is when Saudi employers renew benefits, insurers lock in group medical pricing, and providers feel the impact of new tariffs and reimbursement schedules flow through their cashflows. Going into 2026, this annual reset sits on top of a structural shift: global medical inflation staying in double digits while Saudi is simultaneously expanding coverage, Saudizing the health workforce, and asking private capital to fund a growing share of hospital and clinic infrastructure.

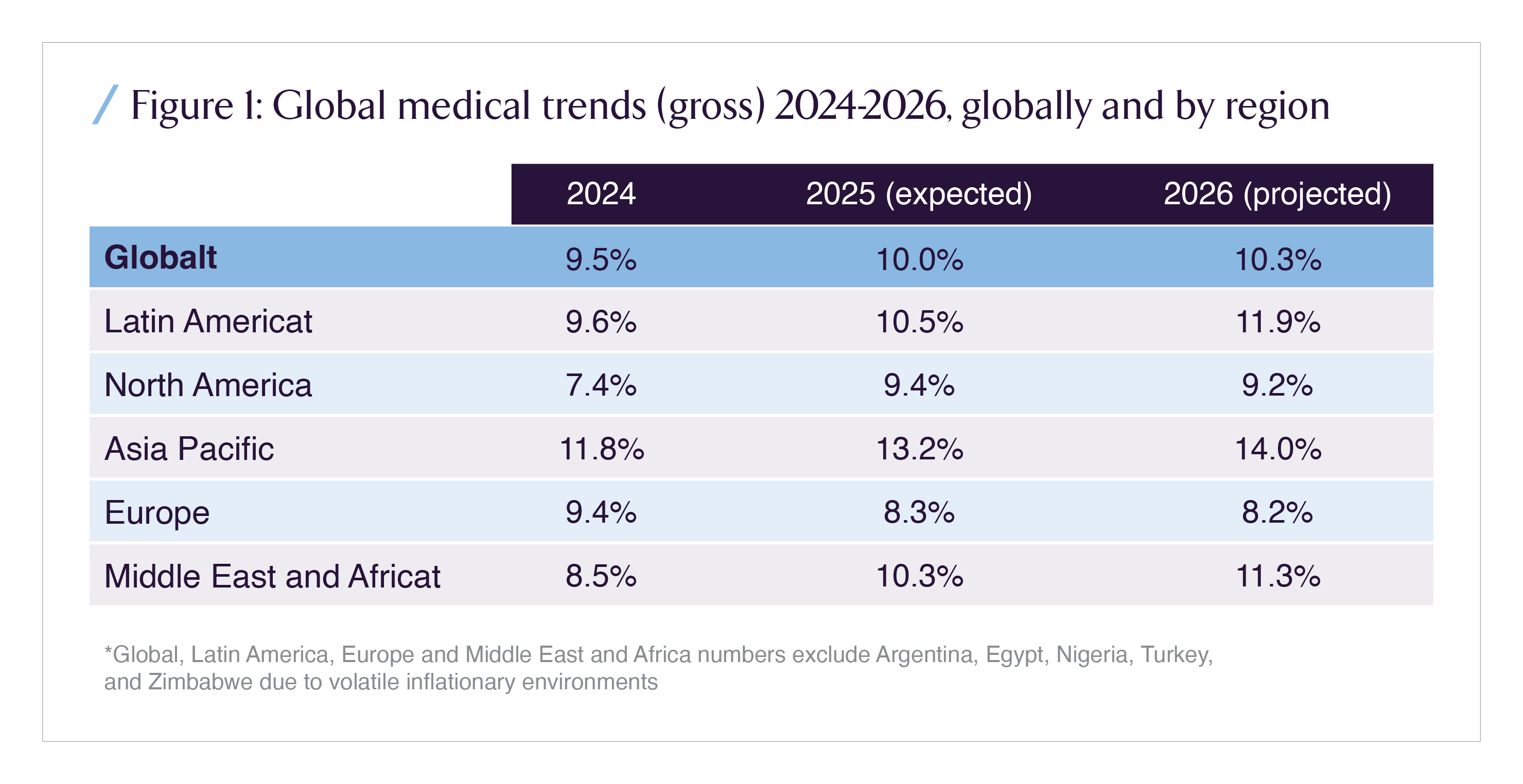

WTW’s 2026 Global Medical Trends Survey projects a global average medical cost increase of about 10.3%, with Middle East & Africa (MEA) at 11.3%, up from 10.3% in 2025 and 8.5% in 2024. Those are not one off spikes; they signal a sustained structural step up in the cost base that investors, employers, payers, and providers must price into long term plans.

In Saudi Arabia, that global story intersects with:

- near universal coverage (over 95% of the population having basic healthcare coverage by 2024),

- a health insurance market that already accounts for ~60% of total insurance GWP, with SAR 42.2 billion in health premiums in 2024 (up 9% YoY),

- and a public financing model where the Ministry of Health budget is increasingly tilted toward compensation of employees rather than programs and capex.

For Saudi investors, the question is not simply “how high will medical costs go in 2026?” but who absorbs the shock, where margins compress first, and which business models benefit from a world where medical trend persistently runs several points above headline inflation.

1. Global Landscape: Double Digit Is the New Baseline

The WTW 2026 Global Medical Trends Survey shows a world where medical cost curves have broken away from general CPI. Global medical trend is projected at 9.5% in 2024, 10.0% in 2025, and 10.3% in 2026. MEA is on a steeper path: from 8.5% to 10.3% to 11.3% over the same period, while Asia Pacific sits even higher at 14% by 2026.

This matters for Saudi allocators because most benefit design, risk pricing, and provider investment models were calibrated on mid single digit medical inflation, with volatility driven by cycle and currency rather than structurally elevated demand and technology curves.

Behind the topline numbers, the global pattern is clear:

- New medical technologies and advanced pharmaceuticals are cited by roughly three quarters of insurers as the primary drivers of medical cost increases.

- Public system strain understaffing, underfunding, and longer waiting times pushes more demand into private plans, raising utilization and unit cost.

- Chronic disease burden, particularly metabolic disease, cancer, and mental health, continues to ratchet up lifetime cost per covered life.

For large global employers with Saudi headcount, this is not a local anomaly; it is part of a worldwide repricing of healthcare risk. Any Saudi specific strategy that ignores the global cost of capital, reinsurance pricing, and multinational benefit harmonization will misread where plan design and limits are heading.

2. Regional Landscape: MEA as a High Pressure Zone

Within that global picture, the Middle East and Africa region is one of the structurally high trend zones. WTW estimates MEA medical cost increases at:

- 8.5% in 2024

- 10.3% in 2025

- 11.3% in 2026

driven by a combination of utilization growth, technology adoption, and specific local cost factors such as fraud, waste, and abuse.

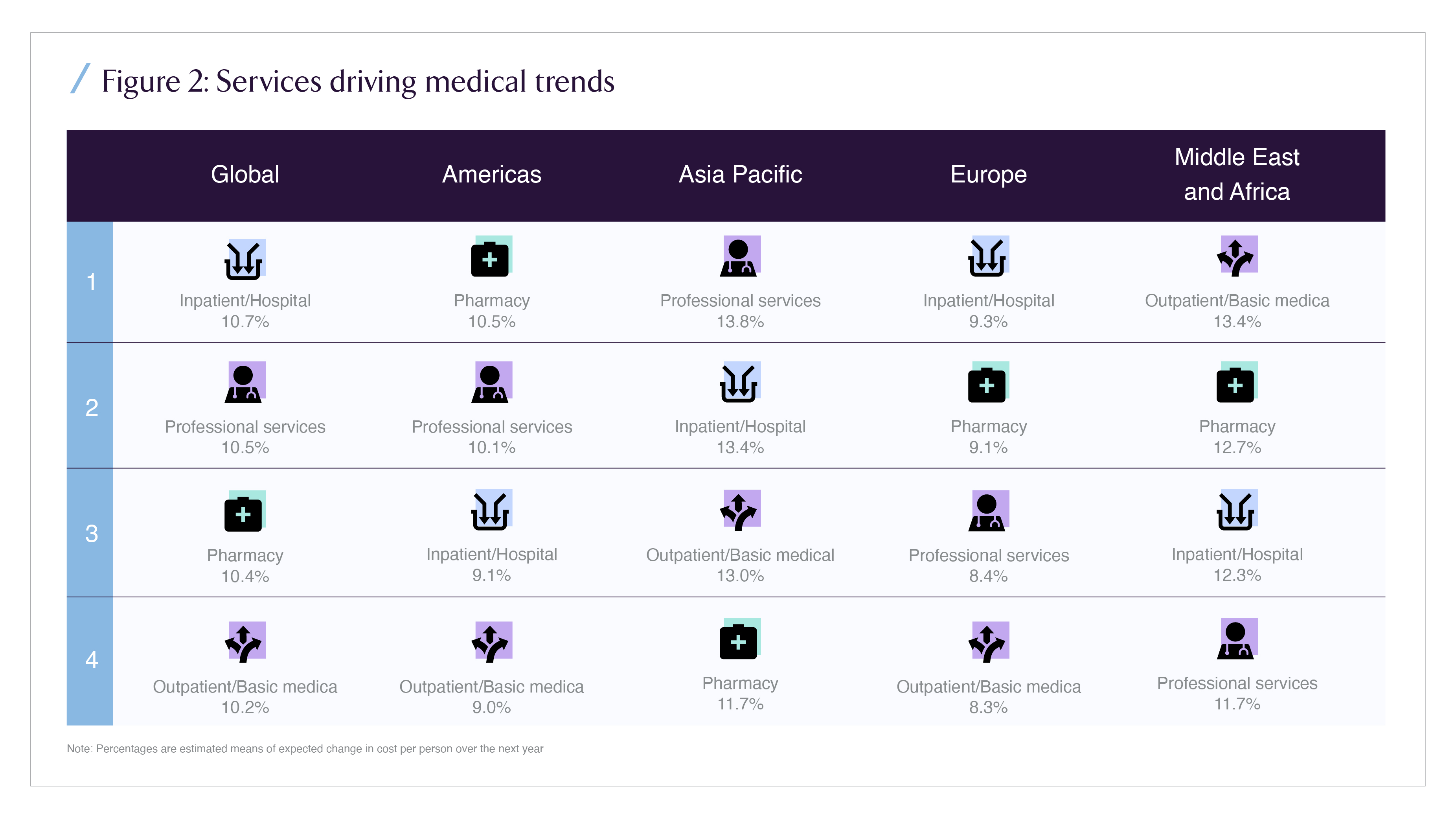

The same WTW survey breaks down which services are driving these cost increases. Globally, inpatient hospital services, pharmacy, outpatient/basic medical, and professional services all contribute; in MEA, inpatient and pharmacy stand out, with outpatient close behind.

For Saudi stakeholders, this regional pattern is instructive:

- It confirms that acute care and hospital based models remain the most inflation exposed assets in benefit plans.

- It underscores how pharmacy strategy (formulary design, GLP 1 policy, biosimilars, oncology protocols) will be at least as important as room and board tariffs in 2026.

- It highlights that fraud, waste, and abuse are not a side story; in MEA, they are cited as a top cost driver by nearly 80% of insurers, reflecting coding, billing, and behavioral issues that traditional actuarial models underpriced for years.

The underlying message: MEA is not just “catching up” with global medical inflation; it is converging at the upper end of the distribution exactly where Saudi’s health financing reforms and Vision 2030 ambitions intersect.

3. Saudi Landscape: Financing Structure, Insurance Depth, and Budget Composition

Saudi Arabia enters 2026 with a health system in mid transition: expanding coverage, shifting financing toward insurance, and gradually rebalancing public and private roles while still bearing the fiscal legacy of a predominantly state funded model.

3.1 Health Financing and Coverage

A 2024 peer reviewed review of Saudi healthcare financing highlights three structural features:

- Health expenditure intensity

- Aggregate healthcare spending reached about 5.97% of GDP in 2021, up from 4.4% in 2001.

- Public expenditure accounts for ~77% of current health expenditure; private financing (including insurance and out of pocket) makes up the balance.

- Coverage depth

- 100% of Saudi citizens and 95.9% of the total population had basic healthcare coverage by 2024, driven by a mix of MOH provision and employment based insurance under CHI.

- Insurance led growth

On the insurance side, health is the core engine of the sector. By 2024, health insurance premiums reached SAR 42.2 billion, up 9% year on year from SAR 38.6 billion in 2023. Health represented a majority share of total insurance GWP, with retention ratios in health lines approaching the high 90s.

From an investor’s perspective, this creates a highly concentrated exposure: the entire Saudi insurance sector’s earnings and capital are heavily correlated to medical claims inflation and benefit design decisions.

3.2 How the MOH Budget is Tilted

Within public financing, the Ministry of Health’s budget allocation has steadily shifted toward staff costs. Between 2010 and 2023, the share of compensation of employees in MOH appropriations increased materially, while the share for programs and projects declined.

- Rigidity in the cost base: A higher wage and allowance share, especially under Saudization, hardens fixed costs; any uplift in salaries to retain clinical talent translates directly into higher per case cost unless productivity rises.

- Less fiscal space for medicines and programs: If personnel absorbs most of the incremental budget, there is less flexibility to absorb price jumps in innovative therapies, biologics, or digital health programs without either rationing or pushing costs into insured/private segments.

- Pressure to use insurance and private capital as a release valve: As public budgets tighten, more care is either re channeled into insured private networks or pushed into mixed models (PPP hospitals, managed networks), shifting inflation risk onto insurers and employers.

By 2030, the combination of an aging population, higher NCD prevalence, and expanded coverage is expected to require thousands of additional hospital beds and greater spend on chronic care infrastructure against a backdrop where the baseline spend is already trending up.

4. Challenges: Where Medical Inflation Hits Saudi Stakeholders

4.1 Employers: Total Reward Math Under Stress

For Saudi employers especially large corporates, listed entities, and high growth mid caps double digit medical inflation collides with three realities:

- Salary & Saudization commitments: As firms upgrade talent and comply with Saudization, medical benefits are part of the total compensation narrative; cutting cover is politically and culturally harder than trimming smaller perks.

- Tightening labor markets in healthcare, technology, and specialized roles mean top candidates increasingly benchmark offers on both salary and health coverage, making aggressive cost sharing a retention risk.

- IFRS & budget visibility: Persistent 10–12% medical trend implies that, without design changes, medical benefits can consume an increasing share of payroll over a five year horizon, affecting EBITDA targets and dividend policy.

Employers who respond by simple premium shopping switching insurers without changing underlying benefit structures or behaviors will see short lived savings followed by steeper adjustments later, as carriers reprice risk after a year or two of unfavorable loss ratios.

4.2 Insurers: Pricing Risk Under a Moving Ceiling

Health insurers in Saudi face a convergence of pressures:

- Trend uncertainty: Global forecasts cluster around ~10% for 2026, but local experience can diverge especially if GLP 1 uptake, oncology pipelines, and advanced diagnostics accelerate faster than expected.

- Regulatory capital: As the Insurance Authority advances risk based capital frameworks, persistent underpricing of medical risk becomes a balance sheet issue, not just an income statement problem.

- High retention ratios in health: With health lines retaining around 96–98% of GWP in Saudi, there is limited risk transfer via reinsurance.

The typical short tail nature of medical claims gives insurers rapid feedback on pricing mistakes, but also limited time to correct course before solvency and capital allocation are affected. For listed carriers, this directly influences valuation multiples and dividend decisions.

4.3 Providers: Wage, Capex, and Reimbursement Squeezes

Providers hospitals, polyclinics, and specialized centers sit at the point where inflation in wages, consumables, and technology translates into line items on invoices. Their challenges include:

- Wage escalation under Saudization in clinical and support roles, as public and private operators compete for the same talent pool.

- Capex heavy expansion plans to address projected bed and capacity gaps, often structured around PPPs or long duration private investments with returns highly sensitive to tariff trajectories.

- Reimbursement complexity as CHI, payers, and NPHIES drive toward standardized coding, DRG style bundles, and tighter medical necessity checks, putting volume at risk for less efficient providers.

Investors backing providers must assume not only higher cost inflation but also more volatile realized revenue as utilization management and preauthorization become sharper.

5. Response Architecture: How Saudi Stakeholders Can Bend the Curve

With the 2026 inflation print largely “baked in” by global conditions, the realistic objective for Saudi stakeholders is not to eliminate medical inflation but to change where it lands on employers, on insurers, on the state, or on households and to reduce its long term slope.

5.1 Employers: From Passive Buyers to Health portfolio Managers

Sophisticated Saudi employers will increasingly behave like asset managers of their health portfolio rather than passive premium payers. Key levers include:

- Benefit design and tiering

Moving from rich, undifferentiated plans to tiered networks, centers of excellence steering, and calibrated cost sharing (co-pays, coinsurance) for non critical utilization. The aim is not to shift cost blindly to employees, but to steer demand away from low value, high cost settings. - Chronic disease management at scale

Using data from NPHIES, TPAs, and wellness programs to identify high risk cohorts (e.g., diabetics with poor control, cardiac patients with repeated admissions) and fund structured interventions disease management programs, nurse led follow up, digital coaching that reduce avoidable admissions and ER use over a 3–5 year horizon. - Contracting and analytics discipline

Treating medical benefits like any other large procurement category: multi year tenders with clear performance metrics; side letters covering GLP 1 formulary rules, oncology protocols, and high cost cases; and quarterly performance dashboards tying premiums, loss ratios, and workforce outcomes together.

These levers are most effective when HR, finance, and risk converge on a single medical benefits playbook rather than treating insurance as a siloed HR purchase.

5.2 Insurers: From Premium Cycles to Health Outcome Plays

For Saudi health insurers, sustained double digit trend raises the bar on execution:

- Underwriting sophistication must integrate employer level experience data, demographic risk, and emerging treatment adoption into pricing, rather than relying purely on past loss ratios.

- Network management must differentiate aggressive cost escalators from efficient providers, with dynamic network inclusion, steerage incentives, and alternative payment models (bundles, shared savings, case rates) for high cost conditions.

- Product innovation can separate pure risk transfer contracts from managed health offerings that explicitly price in care management services, digital triage, and virtual care, making margin less dependent on claims surprise and more on execution.

In a world where health GWP already dominates the insurance portfolio and premiums are forecast to reach SAR 65–80 billion by 2030 under baseline scenarios, the winners will be the carriers able to translate medical inflation into value added risk management, not just higher invoices.

5.3 Providers: Productivity, Case Mix, and Partnership

Providers cannot rely on across the board price increases when employers and insurers are under pressure. Instead, they will need to:

- Shift care to lower cost settings day surgery, ambulatory centers, and virtual follow up where clinically appropriate, freeing inpatient capacity for more complex, better reimbursed cases.

- Invest in operational productivity theatre utilization, LOS reduction, supply chain optimization to offset wage and consumables inflation without degrading quality.

- Co design bundled products with insurers for high volume episodes (e.g., maternity, joint replacement, cardiac procedures), where predictable protocols can underpin shared savings economics.

For investors, this favors assets with strong operating platforms and data capabilities rather than purely real estate heavy hospital plays.

6. Benefits If Saudi Gets This Right

If Saudi stakeholders respond coherently to 2026 medical inflation rather than reactively, several benefits accrue:

- For employers: Medical benefits become a competitive advantage rather than an uncontrolled cost line. Firms with data driven health strategies should see better retention, fewer productivity losses from chronic disease, and smoother budgeting even if premiums remain structurally elevated.

- For insurers: Those who move toward outcome linked products and genuine care management can defend margins, justify higher multiples, and attract capital as active risk managers rather than commodity payers.

- For providers: Operators that adopt productivity and partnership models will be better positioned to secure preferred network status, stable volumes, and access to PPP pipelines and greenfield projects tied to Vision 2030.

- For the state: A better balanced financing mix public budget, mandatory insurance, private capex reduces fiscal vulnerability to oil and macro cycles, while enabling a more targeted use of public funds for high need and vulnerable populations.

In capital allocation terms, the winners are likely to be:

- Integrated insurers with strong analytics, able to price and manage trend.

- Provider platforms with operating leverage and digital capabilities, able to turn higher nominal spend into stronger EBITDA rather than margin compression.

- Specialized service providers (TPAs, data/analytics, disease management platforms) that help bend the long term claims curve for large employer pools.

7. Recap: Medical Inflation 2026 as a Strategic Stress Test

The 2026 medical inflation outlook is not just another year’s renewal challenge; it is a stress test of Saudi Arabia’s emerging healthcare financing model. Global surveys point to another year of double digit medical trend, with MEA at roughly 11.3%. Saudi, meanwhile, is moving deeper into an insurance based system where health GWP already dominates the insurance market and MOH budgets are increasingly absorbed by personnel costs.

For Saudi investors, employers, insurers, and providers, the key questions are:

- How quickly can benefit design and network strategy adjust to structurally higher medical inflation?

- Which assets insurers, hospitals, digital health platforms are positioned to turn inflation into scale advantage rather than margin compression?

- How can capital be deployed to productivity, prevention, and data infrastructure rather than merely funding higher unit prices?

The answers will determine not only 2026 budgets, but also the valuation trajectory of Saudi health related assets over the rest of the decade.