A Regulation Shift That Reprices School Assets

Saudi Arabia’s new municipal requirements for private schools, nurseries, and learning complexes published in December 2025 are not a marginal code tweak. They redraw the physical, safety, and urban planning envelope within which private education operates: where schools can be built, how dense they can be, how much land each student must have, and whether boarding can sit on the same site.

For investors, this matters as much as tuition caps or curriculum approvals. Minimum land per student ratios, frontage on two streets, and explicit permission for on campus student housing directly affect:

- What a financially viable school footprint looks like in Riyadh, Jeddah, and secondary cities

- How many students and therefore how much revenue you can support per SAR of land and capex

- How regulators will view future expansions, conversions, and brownfield upgrades

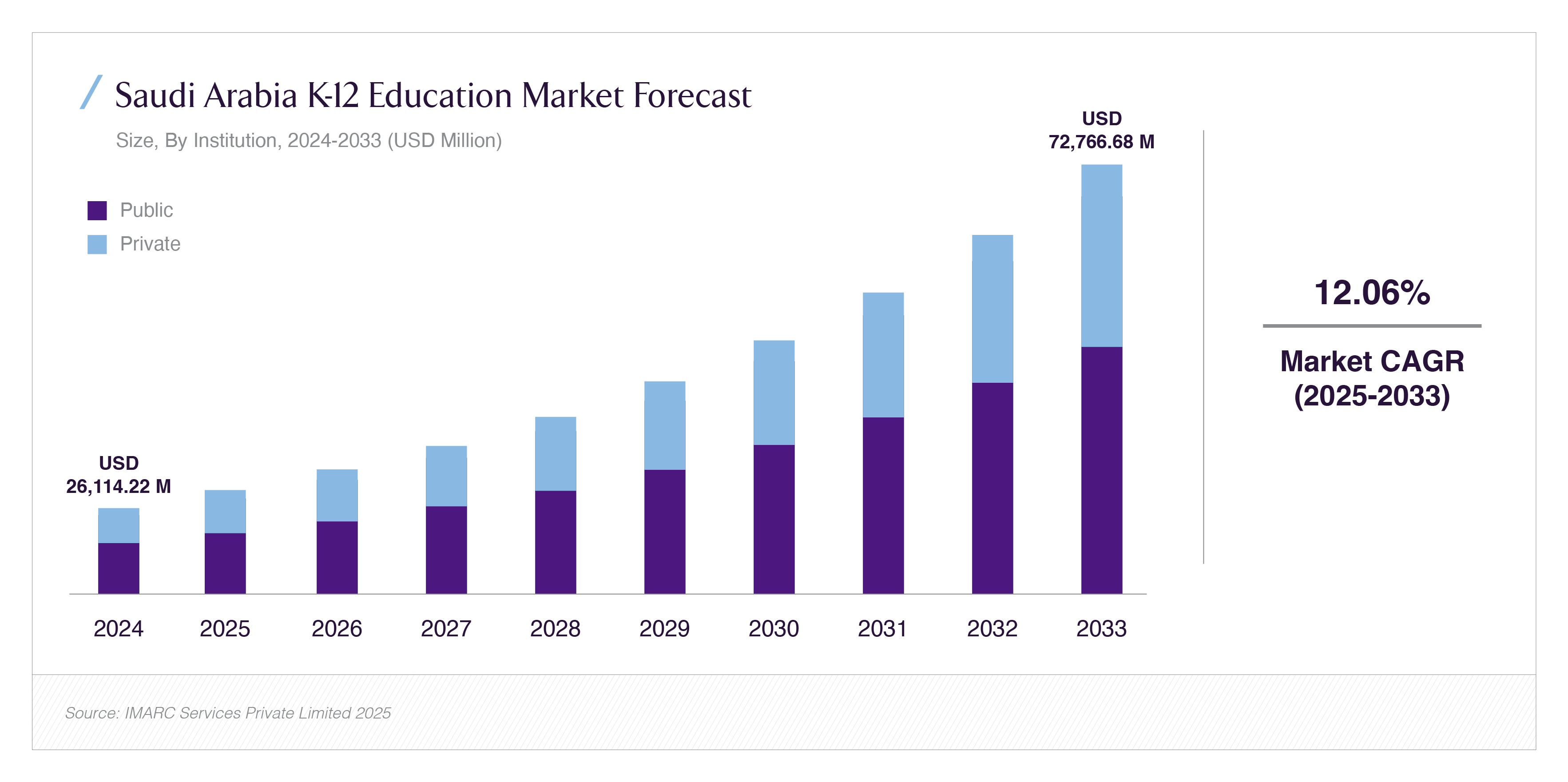

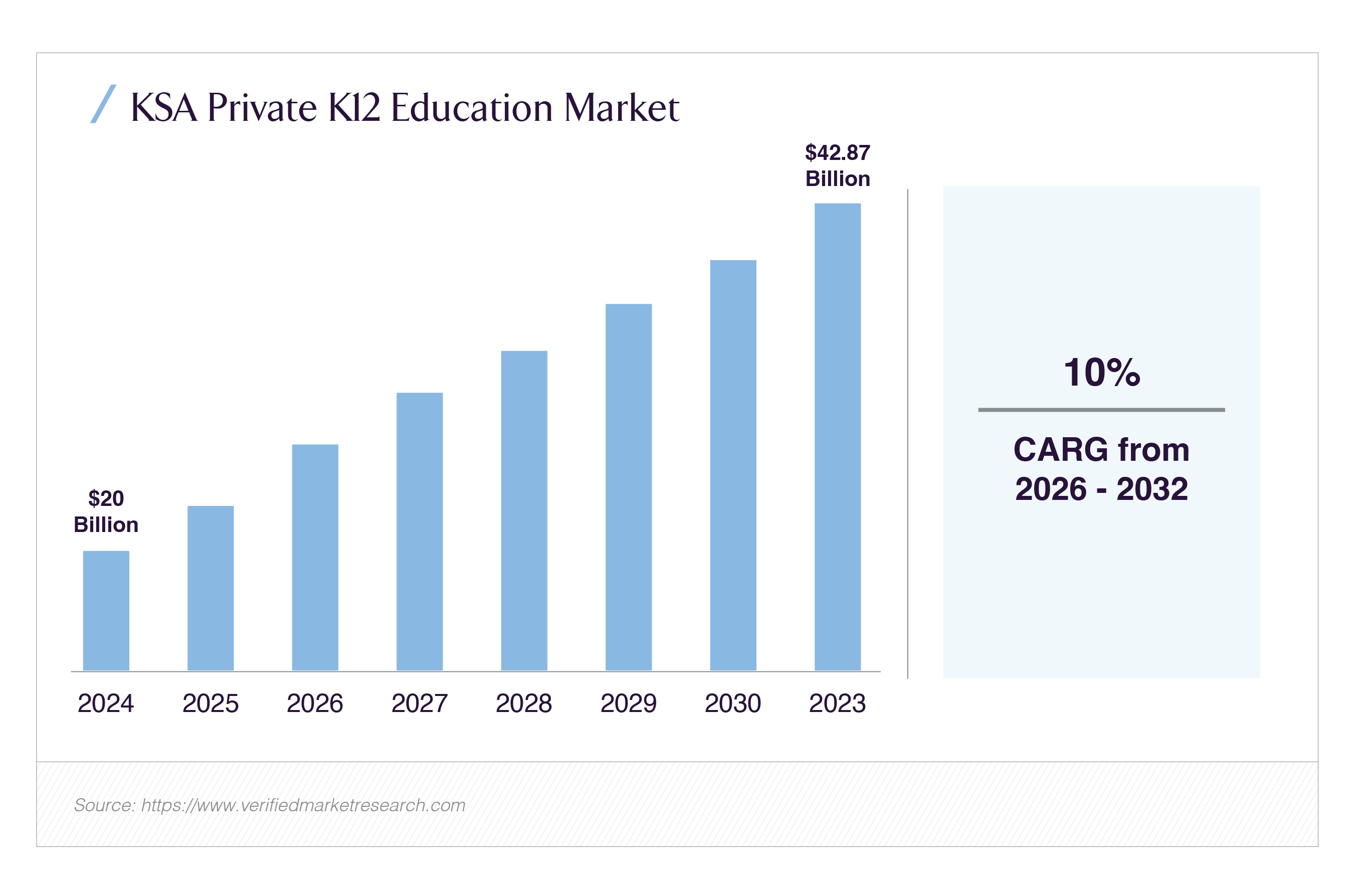

The reforms arrive against a backdrop of rapid private education growth. Saudi’s K-12 education market reached about USD 26.1 billion in 2024 and is projected to nearly triple to around USD 72.8 billion by 2033. Within that, private K-12 alone is estimated at USD 20 billion in 2024, expected to more than double by 2032. As capacity tightens and quality expectations rise, the new rulebook effectively decides which operators can scale and which assets will struggle to remain compliant.

Global Landscape: Private Education as an Infrastructure Like Asset

Globally, private K-12 has become a favored asset class for long term capital: predictable cash flows, indexation through periodic fee increases, and defensible demand in growing urban centers. Global K-12 private education is expected to grow at roughly mid single digit CAGRs through 2030, driven by rising parental preference for non state schools and international curricula.

This capital is increasingly sensitive to physical standards, not only pedagogy:

- International investors look at plot area per student, open space ratios, and safety certifications as proxies for long run capex risk and regulatory stability. OECD facility guidelines explicitly track plot area per student and building quality as core indicators.

- Governments from Europe to the UAE have tightened school building codes mandating compliance with design guidelines for private schools, regular structural inspections, and safety systems as a condition of licensing.

At the same time, private school platforms are commanding higher valuations. A recent example: CVC’s investment in International Schools Partnership at a valuation around EUR 7 billion more than triple its 2021 value illustrates how scaled K 12 platforms with quality real estate and resilient cash flows are being priced.

Against that global context, Saudi’s new municipal standards are not an outlier they are a late but decisive alignment with the way education real assets are underwritten worldwide.

GCC & Regional Landscape: Seat Gaps and Regulatory Convergence

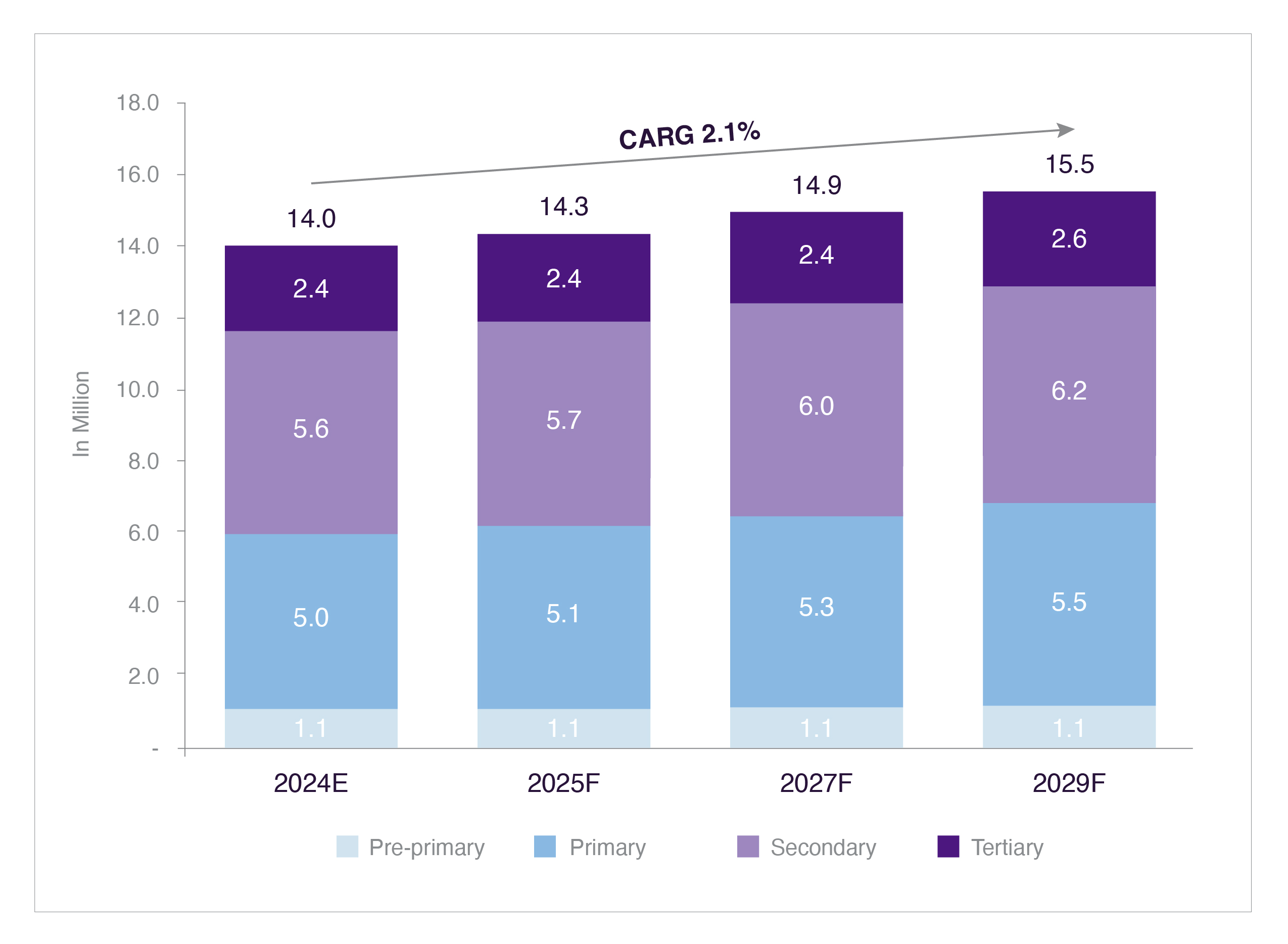

Across the GCC, student enrolment is projected to grow from roughly 14.0 million in 2024 to about 15.5 million by 2029, with K -12 accounting for most of this increase. Private K -12 enrolment is forecast to grow slightly faster than public, implying a structural tilt toward private operators and sustained demand for new campuses.

Dubai and Abu Dhabi already illustrate what a mature, rules heavy private school market looks like: granular building and facilities policies, technical design codes, and periodic inspections are now standard. These frameworks link licensing to:

- Compatibility with surrounding land uses and traffic flows

- Space standards that keep student density within defined bounds

- Documented safety and accessibility features

Saudi’s 2025 municipal rules move the Kingdom in the same direction, but with a sharper focus on land use optimisation and the ability to layer multiple educational stages and boarding onto a single site critical in a geography where land is both expensive and fragmented across city fabrics.

Saudi Private Education Fundamentals: Growth, Seat Gaps, and Asset Demand

At the system level, Saudi’s K-12 education market is already one of the largest in the region. IMARC estimates total K-12 spending at about USD 26.1 billion in 2024, with a projected CAGR of ~12% taking it above USD 72.7 billion by 2033.

Within that, private K -12 is becoming a system in its own right:

- Verified Market Research sizes the KSA private K -12 market at around USD 20 billion in 2024, forecast to reach roughly USD 42.9 billion by 2032 at a 10% CAGR. The segment spans national private schools and international schools (American, British, IB, CBSE, etc.), with growth disproportionately driven by parents seeking global curricula and smaller class sizes.

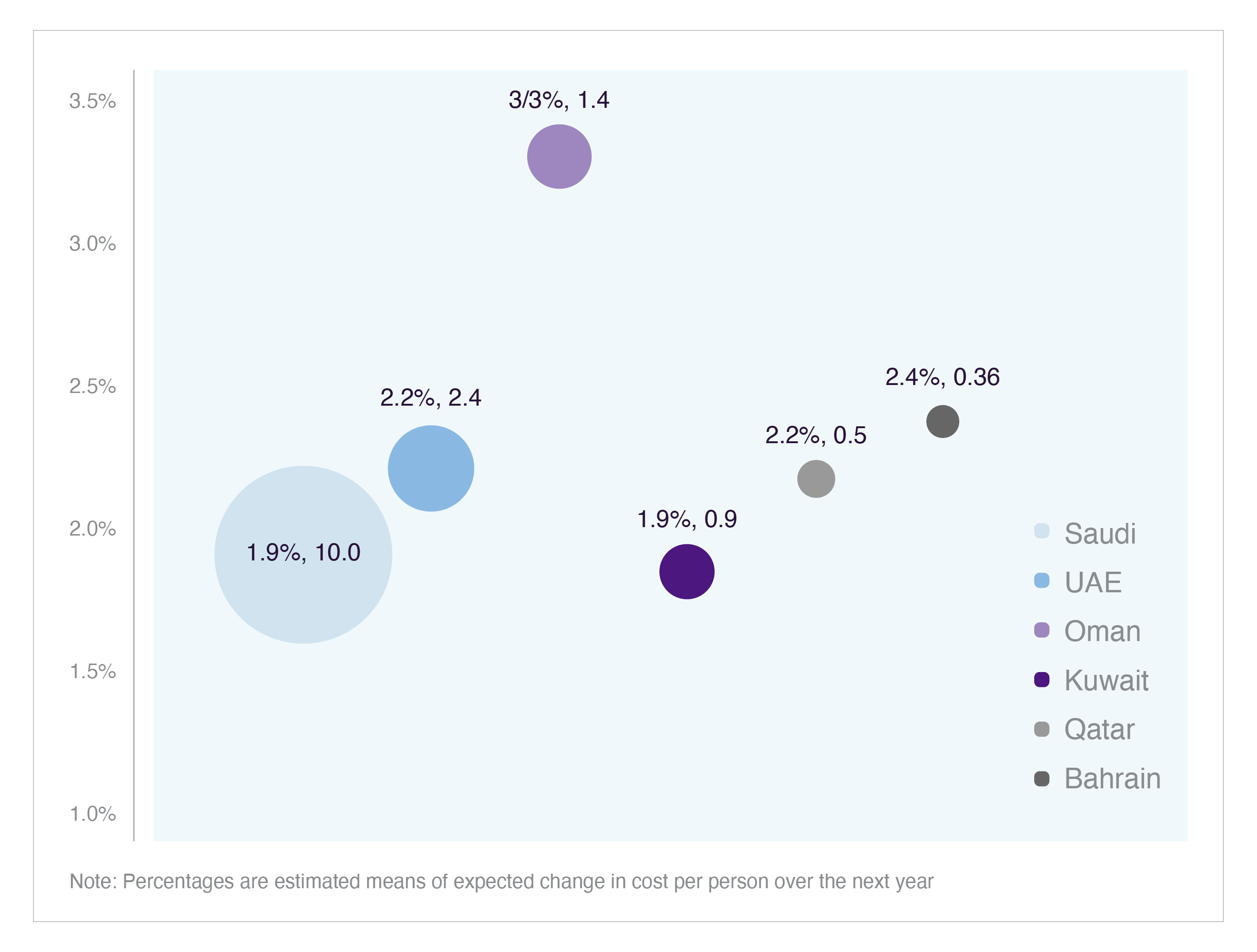

Independent estimates suggest Saudi families will require more than 200,000 additional private school seats by the mid 2030s, with Riyadh and Jeddah carrying much of that incremental demand. At the same time, a GCC wide forecast calls for more than 2,800 new schools by 2029, with Saudi expected to account for roughly two thirds of total students.

The implication is straightforward: capacity is binding. Without regulatory clarity on how dense campuses can be, where they can be built, and how multi stage schooling plus accommodation is treated, investors face significant planning risk. The new municipal rulebook is meant to remove some of that uncertainty but it also raises the floor on acceptable design.

Inside the New Municipal Rulebook: Land, Housing, and Urban Fit

The Ministry of Municipalities and Housing’s December 2025 requirements apply to nurseries, kindergartens, schools, and large educational complexes across the private sector, whether built on land zoned for education, leased government land, or even plots designated for commercial use.

Key features include:

- Two street access and urban integration

Educational buildings must front two streets, with at least one street 25 meters wide. Nurseries can be on a single street, but only if it is at least 15 meters wide and the building is standalone. This is explicitly about traffic management, emergency access, and integration into surrounding neighborhoods. For investors, it narrows the pipeline of eligible plots and increases the value of sites that already meet these criteria. - Land per student standards

The regulations define minimum land area per student, varying by region and stage. Kindergartens must allocate at least 4 square meters per student, increasing to around 5 square meters in educational complexes serving higher grades. This effectively caps density and forces developers to model revenue per square meter against an explicit regulatory ceiling on headcount. - On campus residential facilities

The headline change for many operators is permission to build internal residential facilities for students on campus, provided they are housed in a separate building from the main school. That opens a new revenue line boarding fees while also unlocking catchment areas beyond daily commuting distance, particularly relevant for international schools and for rural or peri urban locations. - Multi stage campuses and commercial plots

The rules allow more than one educational stage (e.g., primary and secondary) within the same campus, consistent with classification standards. They also extend to educational projects on commercial zoned land, provided compatibility with nearby uses can be demonstrated. This encourages master planned, multi stage schools and mixed use developments where education is part of a larger urban program. - Safety, environmental, and accessibility requirements

Municipal inspectors are instructed to enforce stricter rules on emergency exits, fire systems, ventilation, lighting, noise control, and accessible pedestrian routes especially in dense districts. These requirements translate directly into capex and ongoing compliance spend, but also give investors a clearer standard to design against.

Where earlier practice relied heavily on case by case approvals, these rules codify what “bankable” now means for Saudi school real estate.

Challenges: Where Pressure Shows Up in the P&L and Pipeline

For investors and operators, the new framework creates several pressure points:

- Land economics tighten in core cities. Two street frontage, 25 meter road width, and floor height constraints immediately disqualify a portion of existing sites and future land bank options in dense Riyadh and Jeddah districts. The result is higher unit land costs for compliant plots, particularly in neighborhoods with oversubscribed schools.

- Capex per seat rises. Minimum land per student requirements coupled with higher standards for safety systems, circulation space, and outdoor areas will push up capex per seat, even if total capacity per campus remains similar. Investors with proformas built on earlier, looser standards may have to re cut project economics.

- Legacy assets face retrofit risk. Existing schools will be expected to transition toward new standards over time. Operators that cannot finance upgrades for traffic management, accessibility, or safety may face caps on enrolment, shorter license renewals, or reputational pressure from parents and regulators.

- Operational complexity increases with boarding and multi stage models. Adding on campus residential facilities changes staff models, operating hours, and risk management. Multi stage campuses can improve economics but require more complex timetabling, safeguarding, and facility sharing.

None of these are insurmountable, but they shift the sector from opportunistic, plot by plot development toward more institutional, master planned investment logic.

Strategic Responses: How Capital Can Adapt

Experienced education and real estate investors will treat the new rules as a design constraint, not a deterrent. Several strategies stand out.

First, reframe asset selection around the new compliance envelope. Instead of searching broadly for cheap land, investors should start with regulatory filters:

- Two street access now becomes a non negotiable search criterion.

- Plot depth and corner configurations must be modelled against evacuation routes, parking flows, and separation between academic buildings and boarding.

- Land per student ratios should be embedded directly into underwriting models as hard caps on enrolment, with upside only from fee growth or supplementary income streams.

Second, use boarding to change the revenue profile. For international schools or national schools serving distant catchments, boarding can materially lift revenue per site without breaching density limits in classrooms. A well designed residential block, priced at a mid market level rather than ultra premium, can:

- Smooth seasonal utilisation of facilities (libraries, sports fields, labs)

- Raise stickiness of enrolment across grade transitions

- Support scholarship or bursary programs targeting students from underserved regions

This is closer to an education infrastructure play than pure tuition arbitrage.

Third, embrace cluster and PPP models. With land and capex constraints tightening, clusters of schools often developed under PPP frameworks can share central facilities (sports, labs, performing arts spaces) while complying with per student and safety standards. Saudi’s wider privatization agenda in education already points in this direction, with bundles of schools under long term offtake contracts designed to de risk cash flows.

Fourth, design for regulatory “headroom.” Building just to the minimum standard leaves no margin for future rule changes or enrolment surges. Well capitalized sponsors will:

- Over provision circulation space, fire egress routes, and outdoor shaded areas

- Reserve parts of the site for future expansion or modular additions

- Integrate digital monitoring (CCTV, access control, environmental sensors) to simplify compliance reporting

That creates assets that remain compliant longer and command a premium from institutional buyers if and when they exit.

Fifth, benchmark against regional leaders. Comparing MoMRAH’s rules with, for example, Abu Dhabi’s private school design guidelines helps investors see where Saudi’s standards may move next: more explicit requirements for sustainability, energy performance metrics, and learning space typologies.

System Level Benefits: Capacity, Safety, and Predictability

If implemented well, the new standards can strengthen the sector along three dimensions that matter to investors:

- Quality and safety as a floor, not a differentiator

Tighter rules around site planning, safety, and environmental conditions mean investors no longer have to guess whether a project will later be challenged on traffic or fire safety grounds. Instead, compliance is built into the design phase. This reduces tail risk, particularly for international capital unfamiliar with local permitting practices. - More predictable capacity planning

With land per student metrics codified, operators and lenders can calibrate realistic seat counts from the outset. That gives clearer ranges for revenue, staffing, and operating margins per campus. At a macro level, it supports more accurate projections of how many schools and seats the market can deliver over a given time horizon. - Better alignment with Vision 2030 and human capital goals

Higher standard campuses with adequate space, safety, and potential boarding capacity are better suited to the kind of STEM heavy, skills oriented education Saudi policy is pushing. When physical infrastructure supports flexible learning spaces, labs, and digital tools, it becomes easier to layer in new curricula and education technology initiatives without wholesale rebuilding.

For investors with a 10 20 year horizon, that combination demand growth, regulatory clarity, and better quality stock is the core of the thesis.

Recap: How to Underwrite “New Standard” Private Schools

Saudi Arabia’s updated municipal requirements for private educational buildings reset the baseline for how school assets are sited, designed, and operated. Two street access rules, explicit land per student standards, and the introduction of on campus boarding as a regulated use collectively narrow the feasible set of development plots, raise capex per seat, and lengthen planning timelines.

At the same time, the underlying market is expanding rapidly: total K-12 spending is projected to nearly triple by 2033, private K-12 revenues are expected to more than double by 2032, and GCC wide enrolment growth underscores the need for thousands of additional schools.

For Saudi and international investors, the opportunity is not in exploiting regulatory gaps, but in designing deliberately within the new standards:

- Target plots that naturally fit the two street, density, and setback rules

- Use multi stage campuses and boarding to enhance revenue per site without breaching land per student caps

- Build in safety, environmental quality, and digital monitoring to keep assets ahead of future regulatory tightening

Done well, the result is a portfolio of education assets that behave less like opportunistic real estate and more like resilient social infrastructure: long dated, cash generative, and tightly aligned with the Kingdom’s broader human capital ambitions.