.jpg)

Riyadh is running a real time policy experiment in rental stabilization: a five year freeze on rent increases for residential and commercial leases inside the capital’s urban boundary. The directive arrives after a period in which housing linked inflation outpaced the headline CPI and tenant churn accelerated. The policy intent is straightforward: cap renewal shocks, buy time for supply to arrive on formal rails, and anchor expectations for households and businesses. For investors, the consequences are just as clear: the next leg of returns in Riyadh is less about mark to market rent growth and more about operational mastery, basis discipline, and portfolio engineering.

The freeze does not operate in isolation. It is coupled with mandatory Ejar registration/renewals (cleaner cash flow data, faster dispute resolution) and an active White Land Tax (WLT) regime that prods idle plots toward development. Together, these create a policy triad that raises compliance, formalizes income streams, and lowers informational frictions for lenders. In short: fewer surprises on renewals, tighter underwriting around collections, and a clearer route to institutional scale.

Global context: controls, credit, and the supply question

Internationally, rent controls are usually reactive introduced when affordability stress becomes politically binding. Their short run effect is predictable: renewal driven rent inflation cools. The medium run outcome depends on whether formalization and supply keep pace. Where registries are universal, contracts are standardized, and land is mobilized, professional stock grows share and capital prices cash flow predictability. Where these supports are absent, informal markets proliferate and maintenance under investment follows.

Riyadh looks more like the former. Ejar is not a pilot; it is already the default rail for lease documentation and payment workflows. WLT is not theoretical; it is codified and expanding. That combination means the freeze is less a blunt cap and more an operating regime one that channels growth from headline rent to occupancy, tenure length, ancillary services, and cost control.

Regional positioning: what sets Saudi apart in the GCC

Across the GCC, governments have leaned on digital lease registries, targeted enforcement, and ad hoc tenant relief during spikes. Saudi’s differentiator is scale and cadence: more households, larger investment programs, deeper land banks and now, uniform enforcement through Ejar backed by clear penalties. That matters for capital formation. Institutional owners and lenders prize predictable renewals, bankable cash flow trails, and administrative certainty. As the freeze beds in, Riyadh’s rental market starts to resemble the kind of data rich, compliance first environment that lowers the cost of money for qualified sponsors.

Riyadh mechanics: how the rule actually changes cash flows

Under the freeze, a tenant’s renewal rent is flat in nominal terms for five years from the effective date. New to file leases can still set at market on day one; only their first renewal falls under the freeze. Because Ejar registration/renewal is compulsory, landlords and tenants operate on standardized contracts and payment rails. Disputes adjudicate faster; arrears data is visible; collections become a process rather than a negotiation. WLT keeps pressure on serviced land to enter pipeline, limiting the chance that stabilization simply shifts scarcity rents to new districts.

In this world, NOI creation redistributes. Renewal based uplift disappears; value migrates to higher retention, leakage compression, and service monetization. The best owners will grow same store NOI without touching rent: fewer lost days, lower make ready capex, tighter procurement on FM/MEP, and a services layer (parking, storage, maintenance tiers, co working nooks) that tenants buy because it solves daily problems.

A five year frame: what “good” underwriting looks like

Think in cohorts, not units. A stabilized multifamily asset in Riyadh might see ~70–80% of occupied units renew each year under flat rents, while new to file leases (the balance) set at current market. If a sponsor raises occupancy by 150–250 bps, trims gross to net leakage via Ejar enforcement, and installs efficiency retrofits that shave utility intensity 10–15% by Year 3, NOI grows even with zero renewal CPI. Add a modest contribution from services (3–5% of gross by Year 3) and portfolio level returns clear hurdle rates so long as basis is disciplined and capex cadence matches absorption.

This is not spreadsheet alchemy; it is operating craft. It begins at acquisition buying under managed stock where Ejar migration and building systems upgrades can be executed quickly and continues through the hold with KPI driven asset management (renewal propensity scores, arrears probability, service attach rates, utility kWh/m²).

Where the freeze helps and where it bites

- Helps: Predictable renewals lower variance in cash flow models, improve DSCR stability, and can tighten exit caps for fully compliant stock; retention lifts value by reducing capex leakage and downtime; lenders price the visibility.

- Bites: Top line rent growth on renewals is zero; OpEx inflation must be absorbed or neutralized; business plans reliant on rapid mark to market must pivot to mix, services, and operating leverage.

Sector read throughs

Build to Rent (BTR). The most natural beneficiary. The freeze trades rent upside for duration and data quality. Professionally managed BTR extracts value from tenure, amenities, and predictable collections exactly the levers the regime rewards.

Neighborhood retail. Base rents stabilize; tenant survivability improves. Value migrates to turnover style clauses where permitted, curation (category adjacency) that raises basket size, and center run services (IT, facilities, marketing) that landlords can charge for transparently.

Office/flex. Tenants gain cost certainty; owners can productize space (flex suites, managed IT/FM) to diversify revenue. Renewal friction falls, which lowers downtime assumptions a quiet but material boost to cash yield.

Student & workforce housing. Where demand is volume driven near universities or industrial corridors, services plus density can out earn a simple rent per sqm model. In a flat rent world, throughput and utilization become the alpha.

Practical operator playbook (kept tight)

- Contract discipline. 100% Ejar at move in and renewal; auto renew templates aligned to freeze rules; standardized deposit and arrears workflows.

- Retention design. Service bundles (maintenance SLAs, cleaning, parking) priced to save tenants time, not just add fees.

- OpEx modernization. Sub metering, VRF/heat pump retrofits, outcome based FM contracts; centralized procurement for MEP kits.

- Basis partnerships. Pair with landholders carrying WLT to secure advantaged entry and phasing aligned to infrastructure delivery.

- Data hygiene. Build dashboards for renewal propensity, arrears risk, utility intensity, and service attach rates; manage to those numbers.

Risks to underwrite without drama

- OpEx squeeze. Flat rents and rising utilities/FM require real savings, not slogans. Model energy projects with engineering grade assumptions and measured paybacks.

- Capex timing. Over investing before services attach can drag IRR. Phase upgrades with renewal cycles to capture retention and unit grade premiums.

- Compliance friction. Migrating legacy leases to Ejar can be messy; plan for onboarding effort and system training.

- Micro market divergence. New to file pricing latitude will vary by corridor; assume heterogeneity, validate with fieldwork, and avoid proxying from distant districts.

Solutions that move the needle

- Design for services from day one. Storage lockers, parcel rooms, access control, small co working nooks, and robust metering are cheap to plan, expensive to retrofit.

- Programmatic retrofits. Portfolio wide tenders for HVAC, glazing, and LED upgrades concentrate buying power and simplify maintenance.

- Tenant analytics. Renewal/arrears scoring and targeted offers (amenity credits instead of rent cuts) lift tenure and NPS essential in a flat rent regime.

- Capital structure. Favor amortizing bank debt; use mezzanine sparingly and only post de risking (lease up milestones + completion progress). Predictability is the new multiple.

Why this is investable not just survivable

A freeze that is coupled with enforcement and land activation reduces uncertainty. Predictable renewals lower the cost of capital; formal cash flows scale; lenders lean in. For equity, the upside is less speculative and more engineered: retention, services, OpEx discipline, and advantaged basis. For the city, the outcome is less churn, more build through the cycle, and a rental market that looks institution grade.

What to watch into 2026

- Ejar throughput. Monthly registrations and renewals (a tenant churn proxy) and dispute resolution cadence.

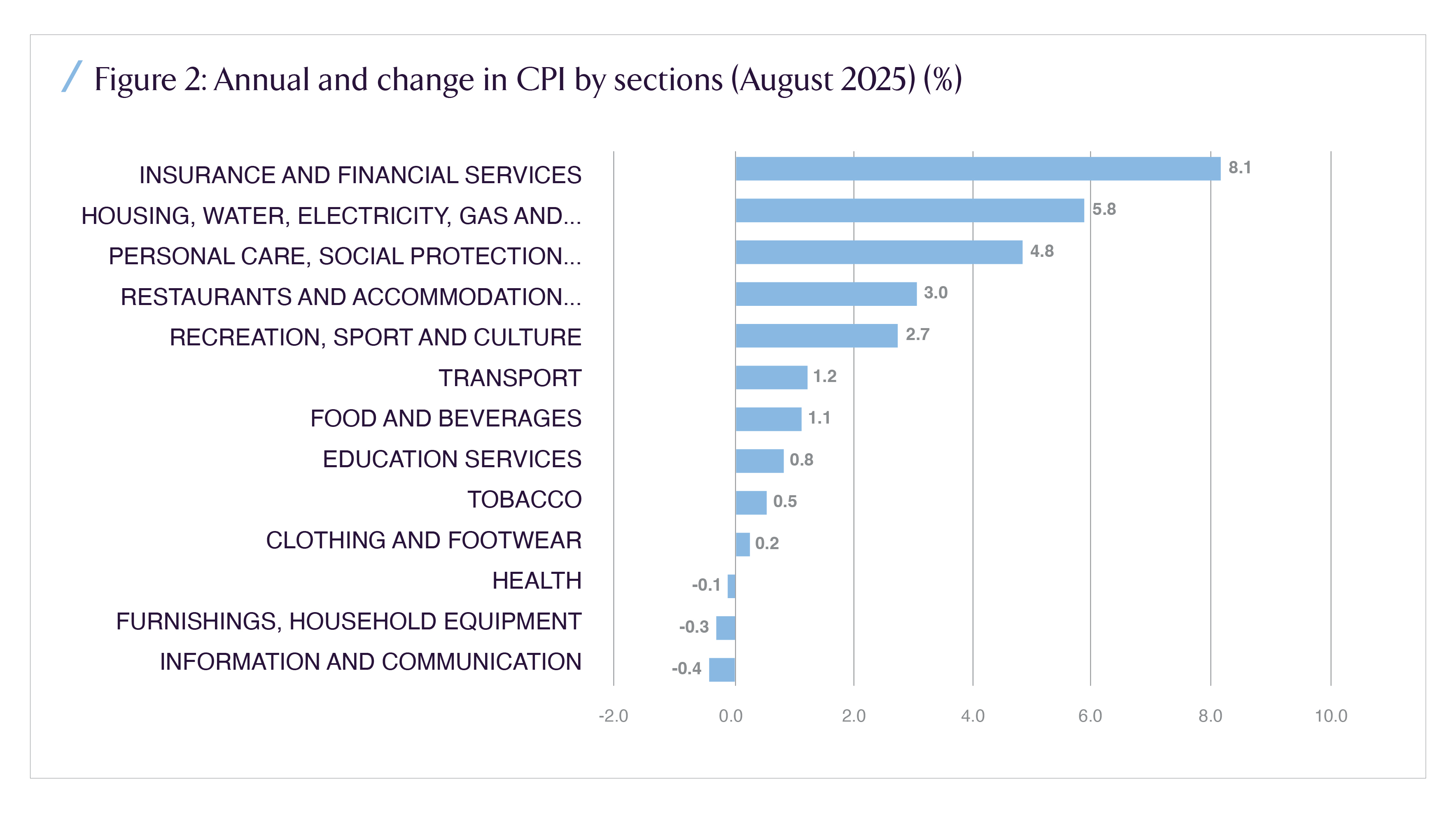

- CPI mix. “Actual rentals for housing” versus headline CPI; confirmation that renewal shocks are fading.

- Land activation. WLT disclosures, serviced plot releases, and district level permit activity especially near transit and civic anchors.

- Credit supply. Mortgage originations and finance company lending; cost and tenor of bank debt available to compliant rental platforms.

- Vacancy/time to lease. Micro metrics by corridor to refine assumptions on new to file pricing and absorption.

Recap

Riyadh’s five year freeze trades price momentum for predictability and formalization. That swap suits professional capital. Returns will accrue to owners who treat income as a management problem: raise tenure, compress leakage, modernize OpEx, and buy or build at disciplined basis with WLT and Ejar in mind. The policy is not a brake on investment; it is a roadmap for how to create value when renewal CPI = 0.