The Q3 2025 print marks an inflection in Saudi real estate: annual inflation slowed to about 1.3% year on year, down sharply from Q2’s pace. Under the hood, the residential complex cooled apartments and residential land dipped while commercial assets still advanced year on year. Quarter on quarter, the composite index fell 1.1%, a reminder that the cycle has transitioned from broad, policy driven appreciation to a more selective, fundamentals first phase.

For allocators, the new regime changes the playbook. Ticket sizes, city mix, and sector tilt now matter more than beta to a rising index. Liquidity is bifurcating between trophy urban corridors and secondary peripheries; leverage appetite is being reset by banks and lenders focused on repayment capacity; and policy is now an active macro variable, specifically rent stabilization in Riyadh and the continued rollout of transaction quality enhancements (e.g., improved REPI methodology, satellite aided classification).

The timely question is not whether the market is “up” or “down,” but where resilient cash yields, downside protected development margins, and policy tailwinds can be combined in risk balanced allocations. This article sets the global context, locates Saudi within the regional cycle, drills into the Q3 2025 sub indices and geography, and then converts the print into investable implications challenges to underwrite, solutions to execute, benefits to capture, and milestones to monitor.

The global landscape: late cycle normalization, higher real rates, tighter credit

Global real estate in 2024–2025 has been defined by three cross currents. First, inflation has moderated in most developed markets, but policy rates have plateaued at levels that remain restrictive versus the past decade. Second, lenders are discriminating: refinancing risk and debt service coverage ratios (DSCR) dominate underwriting screens, especially for assets with capex overhangs (retrofits, code upgrades, ESG compliance). Third, demand has polarized urban core housing and logistics adjacent to consumption nodes are holding up; marginal offices and speculative residential in oversupplied corridors are repricing.

Saudi sits in a structurally different place. Population growth, formalization of the rental market, and multi decade urban programs (Riyadh expansion, giga projects, logistics corridors) create a firm demand baseline. But the global backdrop still matters in pricing debt, determining foreign capital participation, and shaping relative value between sectors (residential vs. commercial) as world cash returns re set.

Global takeaways for Saudi allocators

- Treat the real rate as a binding constraint in pro forma models stress DSCR and interest coverage at today’s curve, not a mean reversion fantasy.

- Assume tighter lender selectivity; velocity of approvals will favor bank grade sponsors with transparent pre lease or sales pipelines.

- Expect cap rates to be sticky on the way down; value creation leans more on NOI growth and development alpha than yield compression.

The regional (GCC/MENA) landscape: policy is the differentiator

Across the GCC, the 2021–2023 post pandemic catch up gave way to 2024–2025 consolidation. The UAE continues to attract expatriate inflows and capital, but price momentum is fragmenting by sub market and project quality. Qatar and Bahrain are showing steady leasing with disciplined new supply. Oman’s logistics led corridors are catalysts rather than a wholesale price driver.

Saudi’s differentiator right now is policy clarity and administrative execution. Riyadh has introduced a five year rent stabilization framework (for both residential and commercial within the urban boundary) and tightened Ejar registration, sending a signal of predictability for occupiers and a blueprint for other cities if and when required. Meanwhile, data transparency improved further with GASTAT’s updated REPI methodology (base year 2023, multi source transaction linkage, geospatial AI classification), enabling more precise city and sub type analytics.

Regional highlights to anchor allocations

- GCC demand is still migration and job led; Saudi’s domestic drivers (household formation, national programs, logistics and services expansion) reduce cyclicality versus pure external inflow markets.

- Saudi policy mix rent stabilization in Riyadh + better measurement supports longer dated underwriting and more credible lease up assumptions.

- For cross GCC portfolios, Saudi offers scale and depth; UAE offers liquidity and velocity; blending them can smooth cycle risk.

Saudi landscape: what Q3 2025 actually says

GASTAT’s Q3 2025 release provides three high signal lenses: sector split, residential composition, and regional dispersion. Each has direct allocation implications.

Sector split (YoY): Commercial rose 6.8% year on year, led by commercial land (+7.2%), with buildings and showrooms positive but milder. Residential fell 0.9% year on year as residential land ( 0.9%) and apartments ( 1.7%) softened; villas ticked slightly higher (+0.2%) and residential floors rose (+0.3%). Agricultural showed strength quarter on quarter (+7.3%), but its investability is more specialized.

Quarter on quarter composite: The total REPI declined 1.1% vs. Q2, with both residential ( 1.1%) and commercial ( 1.6%) down on the quarter pragmatic confirmation that momentum has cooled into year end.

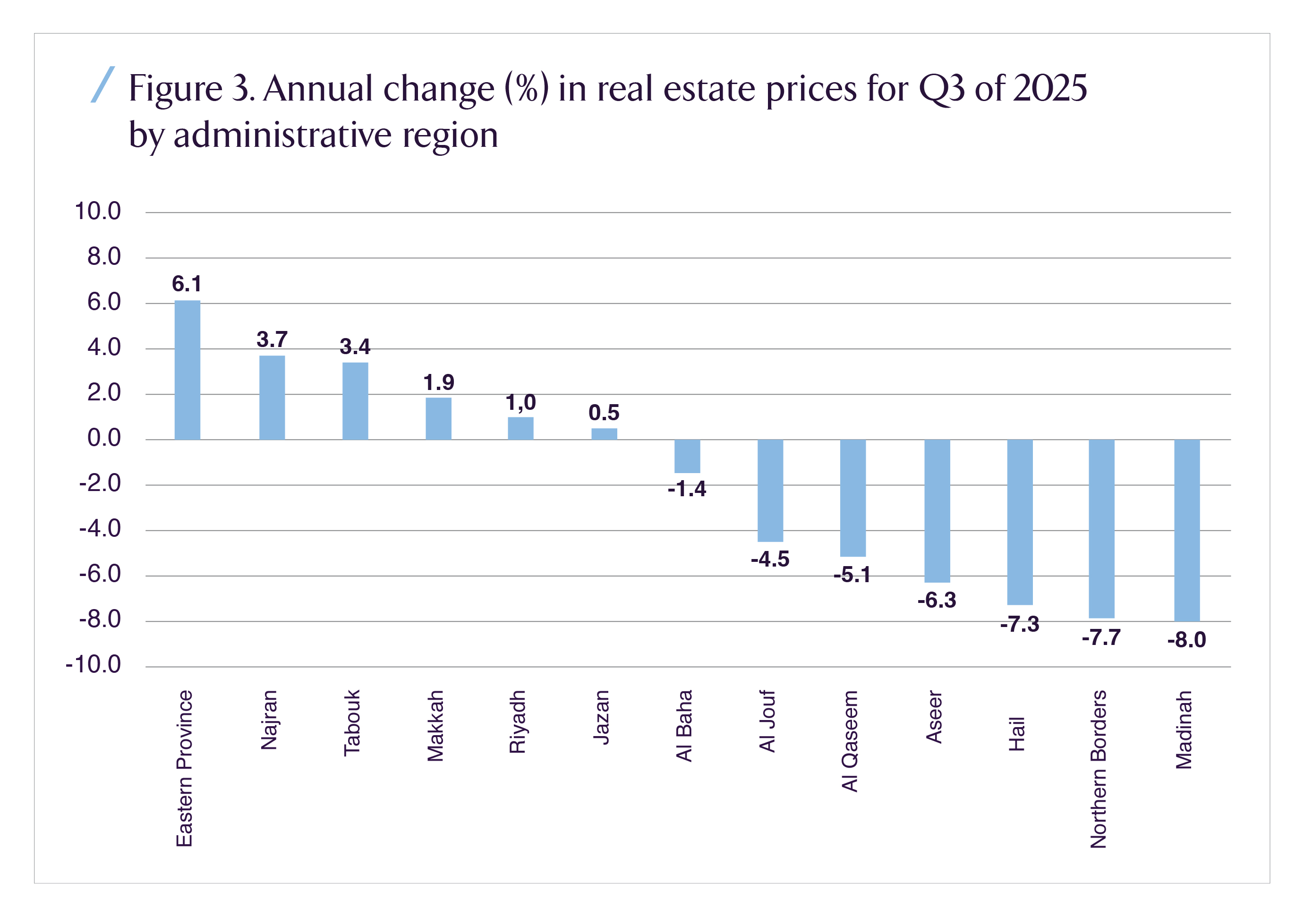

Regional dispersion (YoY): Eastern Province posted the strongest annual gain (+6.1%), followed by Najran (+3.7%), Tabuk (+3.4%), and Makkah (+1.9%). Riyadh rose +1.0% YoY but slowed from Q2’s +3.6%. Hail, Northern Borders, and Madinah printed the steepest declines ( 7.3%, 7.7%, and 8.0%, respectively).

How to read these prints like an allocator

- Beta vs. alpha: The time for riding index beta has passed; selection alpha (sub type, micro location, asset quality) is now the driver of returns.

- Commercial skew: Year on year resilience in commercial especially land reflects positioning along logistics and retail nodes linked to population growth and new corridors. But quarterly softness warns against extrapolation; prioritize pre lease or covenant strength over pure land banking.

- Residential mix: Apartment softness confirms affordability friction at prevailing rate structures; villas’ flat to slightly positive print suggests high income, low elasticity demand pockets endure in specific precincts.

- Geography matters: Eastern Province’s breadth (industrial supply chains, energy services, Khobar Dhahran Dammam triangle) underpins outperformance; Riyadh is growing but policy (rent stabilization) and base effects temper near term prints; the Hejazi belt (Makkah/Jeddah) remains a selective, corridor led story.

Challenges: what sophisticated capital must underwrite

1) Affordability and credit transmission. The step up in real rates has collided with faster price appreciation since 2021, pressuring first time buyers and leveraged move ups. Lenders are tightening repayment ratio thresholds and emphasizing fixed income resilience. Mortgage origination volumes in mid 2025 were uneven, and while stock growth remains positive, the flow is more selective affecting absorption assumptions for for sale product.

2) Rent stabilization in Riyadh. The five year freeze within the urban boundary anchors tenant expectations and reduces renewal driven NOI volatility. For stabilized rental assets, that’s a feature (stickier occupancy), but for value add strategies tethered to rapid market rent capture, it is a constraint. Outside Riyadh, policy may be extended selectively; underwriting should include scenarios.

3) Supply arrival risk. Pipeline projects across major cities are sizable. Where pre sales have been aggressive, construction to delivery execution risk is non trivial, especially in sub markets with rising competing inventory and limited differentiation (design, amenities, community services).

4) Fragmented data quality at the micro level. While REPI is improving, micro parcel comparables in peripheral districts can still be noisy. Over reliance on headline prints can blind investors to on the ground heterogeneity (build quality, HOA/service charge regimes, transport connectivity).

5) Execution capacity. Rapid scaling across multiple cities strains contractor benches, MEP suppliers, and supervision teams. Capex creep and schedule drift can overwhelm thin development margins, especially where land was acquired at peak cycle pricing.

6) Liquidity and exit optionality. Portfolio construction that assumes deep secondary liquidity across all geographies may disappoint. Exit routes trade sale to REITs, strata sell down, or refinance into term debt require deliberate pre planning.

Challenge checklist (for IC memos)

- Stress NOI growth with and without rent cap effects; show DSCR under static rents and rising op ex.

- Require proof of depth in pre sales/pre leases at realistic price points.

- Include a schedule contingency and supplier diversification plan.

- Validate comps with field level audits; don’t proxy from distant districts.

- Map exit paths city by city; assume lower velocity outside top corridors.

Solutions: converting Q3 2025 into a forward allocation plan

Re tier the city mix. Tilt toward Eastern Province corridors with demonstrated occupational depth (Khobar corniche adjacent mid rise apartments; Dammam logistics served retail/showroom; Dhahran proximate villas in established community fabrics). In Riyadh, focus on stabilized, well located multifamily where rent caps lock in occupancy and reduce churn accepting slower NOI growth in exchange for lower volatility. In Makkah/Jeddah, emphasize brownfield and completion risk trades with visible keys in hand dates rather than early stage land positions.

Right size ticket sizes. Avoid lumpy, single asset concentration; favor programmatic, repeatable projects in 100–300 unit brackets (multifamily) or 10–30 k sqm GLA brackets (neighborhood retail) where phasing can be matched to absorption. For development, structure options to expand rather than obligations to complete large phases at fixed cadence.

Sharpen residential segmentation. For sale apartments should re price specs and amenities to the median borrower’s serviceable payment (post rate cap recalibration by banks). For rent multifamily, pursue operational levers tenant services, bundled utilities, maintenance SLAs that raise retention in a rent capped environment.

Commercial with covenant first. Year on year strength in commercial land is not a license for undisciplined greenfield. Prioritize end user anchored build to suit, medical/education adjacencies, and retail in catchments with rising daytime population (government service hubs, university nodes). Land banking is only justified where zoning catalysts or infrastructure delivery are dated and funded.

Capital structure discipline. In the current cost of capital regime, stack leverage should be sized for stability, not maximal IRR. Blend senior bank debt with mezzanine only where lease covenants are investment grade. For development, prefer equity heavy JV structures front loaded with contingency capital; activate mezzanine only after de-risking milestones (e.g., 50% pre lease/pre sale and 30% construction progress).

Data and diligence upgrade. Pair the headline REPI signals with micro surveys: building by building mystery shopping, HOA reserve adequacy checks, op ex benchmarking, and transit/time to CBD mapping. Treat satellite aided classifications as a starting point; validate on site.

Execution playbook (operators and funds)

- Pipeline control: Stage releases to match genuine demand; keep a “stop/go” on each tranche.

- Operating leverage: Centralize procurement (MEP kits, finishes) to reduce cost variance.

- Policy aware leasing: In Riyadh, shift value creation toward occupancy/retention, service upsells, and ancillary income; outside Riyadh, maintain headroom for market rent growth scenarios.

- ESG/retrofit edge: Bake energy efficiency and water saving retrofits into underwriting utility savings become the new “cap rate compression” in rent stabilized contexts.

Benefits: why this regime is investable not just survivable

Stability with selective upside. Cooling prints curb speculative froth and re anchor price discovery in cash flows. Investors willing to do suburb and corridor level work can buy resilience at reasonable entry yields.

Policy driven predictability. Riyadh’s rent framework, tighter Ejar enforcement, and measurement upgrades reduce legal and data uncertainty. That improves lender confidence and can lower funding spreads for qualified sponsors.

Human capital and services multiplier. Delivering rental communities, neighborhood retail, and mixed use nodes in growth corridors catalyzes service sector jobs and small business formation supporting local absorption and stickier occupancy across cycles.

Portfolio construction advantages. A cooler, more dispersed market allows institutional buyers to accumulate at scale without igniting price spikes especially in Eastern Province and Hejazi sub markets building diversified cash flow streams that travel well into a REIT wrapper or long term core fund.

What to watch into 2026

- Monthly mortgage flow and bank guidance. Track new origination series and lenders’ repayment ratio policies; these directly map to apartment absorption velocities and achievable price points.

- Riyadh rent rule implementation. Monitor Ejar enforcement and any extensions or clarifications (e.g., treatment of upgrades, vacancy resets, exception cases). Adjust NOI growth ladders accordingly.

- Delivery cadence vs. pre sales. Overlay project completion timetables with pre sale/pre lease intake; focus on corridors with widening pre sale gaps (supply risk) or sustained intake (pricing power).

- Regional divergence. Eastern Province’s run rate vs. Riyadh normalization will shape 2026 city weights; watch whether Makkah’s positive print broadens beyond select districts.

- Macro rate path. Any downward drift in funding costs would expand affordability bands; be ready with shovel ready phases and line of credit headroom.

Recap

Q3 2025 confirms that Saudi real estate has moved from a momentum dominated upcycle to a fundamentals dominated allocation game. The headline annual inflation rate slowed to ~1.3%; residential sub components softened (apartments and land), while commercial stayed up year on year. Quarter on quarter, both sectors cooled. Regionally, Eastern Province outperformed; Riyadh moderated; several regions posted negative prints. The takeaway for professional capital is clear: lean into selection alpha sector, sub type, corridor, covenant and lean into operator discipline phasing, policy aware leasing, and cost control. In return, you buy stability, policy predictability, and scalable platforms ready to compound into the later cycle phase.