A Sovereign Capital Markets Channel for Housing at Scale

On May 19, 2026, on the sidelines of the World Urban Forum in Baku, Azerbaijan, Saudi Arabia's Minister of Municipalities and Housing Majid Al-Hogail announced a strategy that reframes how the Kingdom intends to finance its housing ambitions for the remainder of the decade. Saudi Arabia plans to issue up to SAR 150 billion (USD 40 billion) in real estate sukuk in global markets by 2030, targeting annual issuances of approximately SAR 20 billion (USD 5.3 billion). The Kingdom is awaiting the stabilization of geopolitical conditions which have elevated global financing costs through their effect on benchmark rates and risk premia before commencing the annual issuance programme this year. The trigger for this strategy is not opportunistic; it is structural. As Al-Hogail explicitly stated, Saudi Arabia is relying on real estate sukuk issuances to alleviate the financing burden on its banking sector, which is facing genuine liquidity pressure from the demands of financing Vision 2030's mega-project pipeline simultaneously with the Kingdom's mortgage market expansion.

This announcement is categorically distinct from the topics Tanmeya has previously examined in its real estate finance coverage. It is not about mortgage-backed securitization, the corporate RMBS programme operated by the Saudi Real Estate Refinance Company (SRC) that converts pools of existing mortgages into tradable debt securities. It is not about the volume of mortgage lending flowing to Saudi homebuyers. It is about a government-directed sovereign debt strategy to finance housing supply at scale through the international capital markets, deliberately routing the capital formation for housing delivery away from the balance sheets of Saudi commercial banks and toward global institutional fixed-income investors who are seeking exactly this kind of Shariah-compliant, sovereign-backed, real-asset-linked exposure.

The strategy rests on a proven precedent. In February 2025, SRC a wholly owned subsidiary of the Public Investment Fund listed a USD 5 billion international sukuk programme on the International Securities Market of the London Stock Exchange and priced its first issuance under that programme: USD 2 billion in government-guaranteed sukuk, structured in two tranches of three and ten years, that was oversubscribed six times with participation from more than 300 institutional investors worldwide. That oversubscription of global demand at six times the offered volume is the empirical proof that the appetite for Saudi sovereign-linked real estate fixed income exists at scale in the international market. The USD 40 billion programme that Al-Hogail announced is the scaling of that proven channel into a structural, multi-year, sovereign-directed housing finance mechanism. This article examines why the bank liquidity constraint exists, how real estate sukuk differ mechanically from RMBS and conventional bonds, what the SAR 20 billion annual programme implies for housing delivery and unit pricing, and what the investment case looks like for institutional fixed-income allocators.

The Bank Liquidity Constraint: Why the Kingdom Needs a New Channel

To understand why Saudi Arabia is building a sovereign real estate sukuk programme, an investor must understand the specific liquidity dynamics that have emerged in the Saudi banking sector as a consequence of Vision 2030's financing demands. The constraint is real, it is documented across multiple independent sources, and it is the structural driver of the entire strategy.

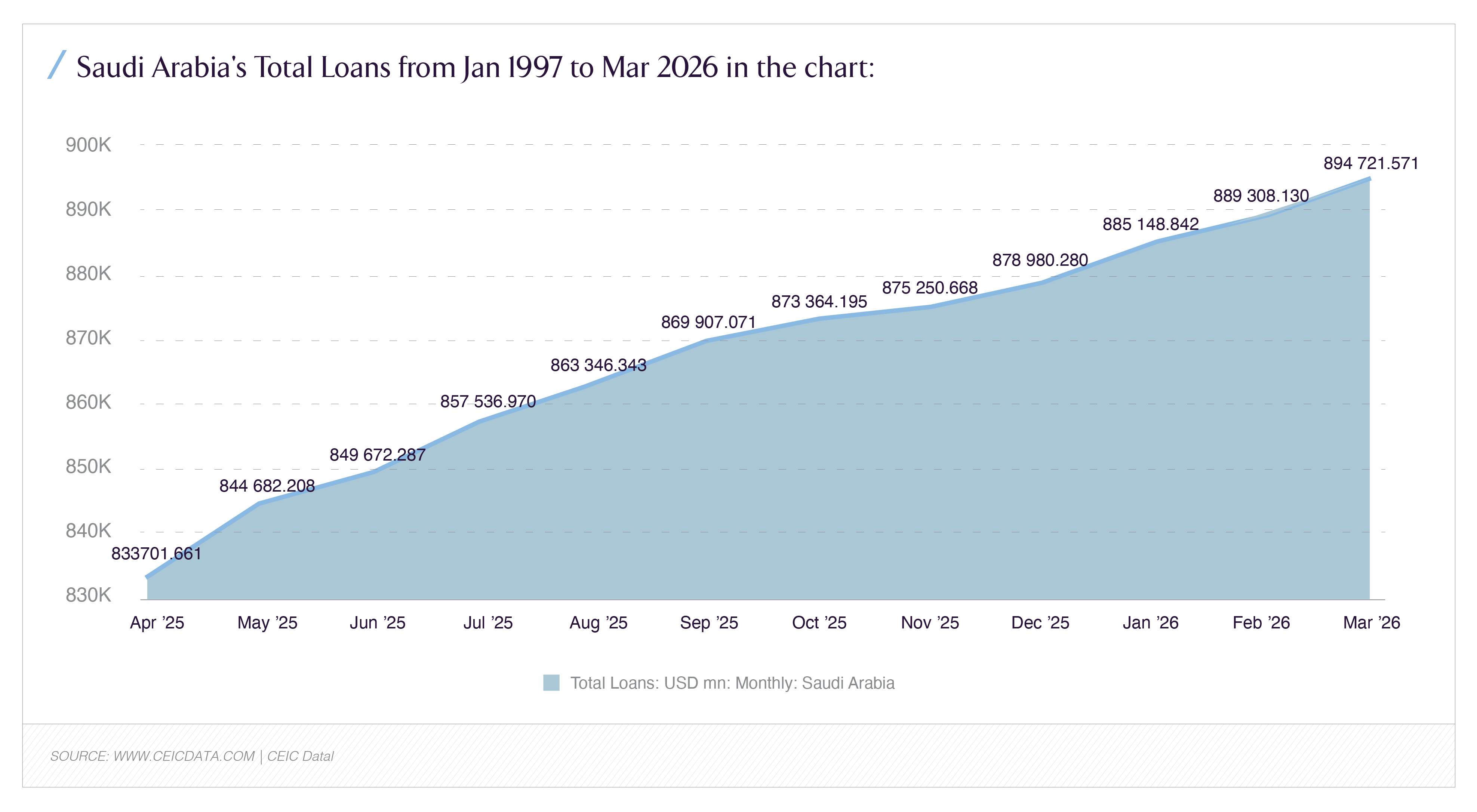

The fundamental tension is that credit growth has persistently outpaced deposit growth in the Saudi banking system. According to SAMA data, total bank loans reached approximately USD 894.7 billion (SAR 3.35 trillion) by March 2026, having grown at 16.51% year-on-year as of April 2025 the fastest pace since mid-2021. This credit expansion is dominated by two forces: corporate lending to Vision 2030 mega-projects and mortgage lending to Saudi homebuyers. Corporate loans grew 22% annually to SAR 1.72 trillion, accounting for over 55% of total credit, with real estate developers alone claiming 21.77% of outstanding corporate credit, the single largest sector concentration. Mortgage lending climbed 14.5% to SAR 932.8 billion in Q2 2025, and the overall real estate financing portfolio expanded from approximately SAR 200 billion to more than SAR 900 billion (USD 240 billion) by 2025, now accounting for 27% of Saudi banks' total loan portfolios.

The problem is that deposits have not kept pace. The IMF's 2025 Article IV mission, published in June 2025, documented the dynamic with precision: strong double-digit credit growth is leading to funding pressures and a change in the funding mix of Saudi banks, with the regulatory loan-to-deposit ratio on a sustained upward trend and the ratio of liquid assets to short-term liabilities declining. The most striking single indicator of the constraint: Saudi banks' Net Foreign Assets turned negative in 2024 for the first time since 1993, as banks increasingly relied on external borrowing bonds, syndicated loans, and certificates of deposit to bridge the gap between credit demand and deposit supply. Fitch's April 2026 assessment found that the sector's loan-to-deposit ratio reached a record 108% by late 2025, with external liabilities rising to SAR 650 billion. A further structural complication: government-related entity deposits, which account for approximately one-third of total sector deposits, became more rate-sensitive during the high-interest-rate cycle, with GRE deposits at the central bank dropping from SAR 670 billion in 2023 to SAR 460 billion by early 2025 as these entities moved funds to higher-yielding placements.

The consequence is that Saudi banks are approaching the practical limits of their capacity to fund both the mega-project pipeline and the housing mortgage expansion from their deposit base alone. Fitch forecast that bank debt issuance would exceed USD 20 billion in 2025 to bridge the funding gap. This is sustainable in the near term; the Saudi banking sector remains well-capitalized, highly profitable, and maintains exceptionally low non-performing loan ratios of 1.0–1.3%, among the lowest in the GCC. But it is not the optimal long-term structure for financing housing supply, because every riyal of housing finance that flows through a bank balance sheet consumes bank capital, competes with mega-project lending for the same constrained funding, and raises the system's reliance on increasingly expensive non-deposit funding. The sovereign real estate sukuk programme is the structural solution: it creates a direct channel from global institutional fixed-income capital to Saudi housing finance that bypasses the bank balance sheet entirely.

How Real Estate Sukuk Differ Mechanically from RMBS and Conventional Bonds

For investors and analysts to correctly price the opportunity that the USD 40 billion programme represents, it is essential to understand precisely how a sovereign real estate sukuk differs mechanically, legally, and from a risk perspective from both the conventional bond and the mortgage-backed security. These three instruments are frequently conflated, but they are structurally distinct, and the distinctions determine their respective risk-return profiles.

A conventional bond is a debt obligation: the issuer borrows a principal sum and contractually agrees to pay periodic interest (coupon) and repay the principal at maturity. The investor's return is interest on a loan, and the investor's claim is a general creditor claim against the issuer's balance sheet. This structure is not compliant with Shariah principles, which prohibit riba (interest), and therefore conventional bonds are not investable for the substantial pool of Islamic finance capital the Shariah-compliant asset management industry, Gulf and Southeast Asian Islamic banks, takaful (Islamic insurance) operators, and Shariah-screened sovereign and pension funds that constitutes a growing share of global fixed-income demand.

A sukuk is structurally different in a way that is precisely suited to real estate finance. Rather than representing a debt obligation paying interest, a sukuk represents a beneficial ownership interest in an underlying tangible asset or pool of assets, and the investor's return derives from the income generated by those assets rent, lease payments, or profit-sharing rather than from interest on a loan. In a real estate sukuk specifically, the underlying assets are property or property-linked cash flows: the sukuk holder owns a share of a portfolio of real estate assets or development financing receivables, and receives periodic distributions derived from the returns those assets generate. This is the structure that makes sukuk both Shariah-compliant and naturally aligned with real estate finance; the instrument is, by design, a claim on real assets and their income, which is exactly what housing finance produces.

The mortgage-backed security (RMBS) the instrument at the heart of SRC's corporate securitization programme examined in Tanmeya's October 2025 analysis is a specific structure in which a pool of existing mortgage loans is packaged into tradable securities, with the cash flows from homeowners' mortgage payments passed through to the security holders. RMBS is a refinancing mechanism: it allows a mortgage originator (a bank or SRC) to sell existing mortgages off its balance sheet, freeing capital to originate new mortgages. The sovereign real estate sukuk programme that Al-Hogail announced is fundamentally different in its purpose and its position in the capital stack. Where RMBS refinances mortgages that have already originated recycling capital that has already been deployed the sovereign real estate sukuk programme is designed to raise new capital to finance housing supply that has not yet been delivered. RMBS sits downstream of housing delivery, converting completed mortgage assets into liquidity; the sovereign sukuk programme sits upstream, providing the capital that funds the housing delivery in the first place.

The distinction matters enormously for the capital stack. A sovereign-guaranteed real estate sukuk backed, as the SRC precedent demonstrates, by an explicit Saudi government guarantee carries the credit risk of the sovereign rather than the credit risk of a pool of individual mortgage borrowers. SRC's standalone credit ratings (Fitch A+ stable, S&P A positive, Moody's A2 positive) already reflect strong creditworthiness, and the government guarantee elevates the sukuk's effective credit standing to the sovereign level. For an institutional fixed-income investor, this is a categorically different and more attractive risk proposition than holding the dispersed default risk of an RMBS pool. The sovereign real estate sukuk offers sovereign credit risk, real-asset backing, Shariah compliance, and exposure to one of the world's most actively developing housing markets, in a single instrument.

What SAR 20 Billion Per Year Means for Housing Delivery and Unit Pricing

The annual SAR 20 billion (USD 5.3 billion) issuance target is not an arbitrary figure it is calibrated to the housing delivery economics that the programme is intended to finance, and understanding its implications for supply timelines and unit pricing is central to the investment thesis for both the sukuk instruments themselves and the broader Saudi residential market.

Saudi Arabia's housing finance ecosystem is anchored by the Real Estate Development Fund (REDF), the largest financier of the Saudi real estate sector, with a portfolio of approximately SAR 190 billion. The REDF, alongside SRC's liquidity provision to mortgage lenders, constitutes the public-sector financing infrastructure that supports the Vision 2030 homeownership target of 70% for Saudi citizens a target against which the Kingdom has made substantial progress, rising from 47% homeownership at Vision 2030's launch to approximately 66% by 2025, according to the 2025 Vision 2030 annual report. The remaining gap to the 70% target, combined with population growth toward 40 million by 2030 and the household formation rate of a young and rapidly urbanizing population, defines the housing delivery requirement that the sukuk programme is designed to finance.

At SAR 20 billion per year, the programme provides a substantial and predictable annual capital injection into housing finance that is independent of bank balance sheet capacity. The strategic logic of routing this through sukuk rather than through the banking system is that it stabilizes the cost and availability of housing finance: when housing supply financing depends on bank lending capacity, it is subject to the funding pressures and rate volatility that the banking sector experiences, which transmits into mortgage availability and pricing for homebuyers. A dedicated sovereign sukuk channel insulates housing finance from this volatility, providing a more stable funding base that supports more predictable housing delivery timelines and, critically, more stable unit pricing.

The unit pricing implication is the element most directly relevant to residential real estate investors. Saudi residential prices have experienced significant appreciation over the Vision 2030 period. Riyadh apartment values rose 10.5% in 2025 and villa values appreciated sharply over preceding years, with the September 2025 Riyadh rent freeze introduced specifically to address affordability pressure. A core driver of this pricing pressure has been the mismatch between demand (supported by expanding mortgage availability and demographic growth) and supply (constrained by the pace of housing delivery). By providing a stable, scaled, non-bank-dependent financing channel for housing supply, the sukuk programme is designed to accelerate the delivery side of this equation, increasing the volume of housing units brought to market and thereby moderating the supply-demand imbalance that has driven price appreciation. For investors, this implies a housing market where supply growth is better funded and more predictable, which moderates the speculative pricing dynamics that characterize supply-constrained markets and supports a more sustainable long-term price trajectory.

The programme's effect on the broader capital stack is also significant for institutional real estate investors. By establishing a deep, liquid, internationally-traded sovereign real estate sukuk market, Saudi Arabia is building the fixed-income infrastructure that underpins a mature real estate capital market. A liquid sovereign real estate sukuk curve provides a pricing benchmark for all other real estate debt in the Kingdom corporate developer sukuk, RMBS, and eventually private real estate credit in the same way that sovereign bond yields anchor the pricing of all other fixed income in developed markets. The development of this benchmark is a structural enabler for the entire real estate debt capital market, reducing the cost of capital across the sector and deepening the financing options available to developers, REITs, and other real estate capital users.

The Regional and Global Context: Sukuk as the Gulf's Dominant Capital Markets Instrument

Saudi Arabia's sovereign real estate sukuk programme is being launched into a global sukuk market that has matured into one of the most significant fixed-income asset classes in the world, and understanding this context is essential for assessing the demand depth that will determine the programme's success. The global sukuk market has grown to exceed USD 900 billion in outstanding issuance, with annual issuance volumes routinely surpassing USD 200 billion, driven by sovereign and quasi-sovereign issuers across the GCC, Malaysia, Indonesia, and increasingly non-Muslim-majority jurisdictions seeking access to Islamic finance capital pools. Saudi Arabia is the world's largest sovereign sukuk issuer, and the Kingdom's National Debt Management Center has built a deep and liquid riyal-denominated and dollar-denominated sovereign sukuk curve that provides the pricing infrastructure onto which the real estate sukuk programme will be layered.

The GCC context is particularly favorable. The region's sovereign and quasi-sovereign issuers Saudi Arabia, the UAE, Qatar, and their respective government-related entities have established themselves as benchmark sukuk issuers whose paper is held by a global institutional investor base that extends well beyond the Islamic finance world to include conventional fixed-income allocators seeking GCC sovereign exposure, emerging market debt diversification, and the yield premium that GCC sovereign sukuk offers over comparable developed-market sovereign debt. The six-times oversubscription of SRC's first issuance, with participation from over 300 institutional investors, is direct evidence that this global demand base will absorb scaled Saudi real estate sukuk issuance.

The instrument's structural alignment with global institutional demand is also strengthening as a function of two trends. First, the growth of dedicated ESG and sustainable fixed-income mandates has created demand for instruments that finance socially beneficial outcomes affordable housing being a paradigmatic example and a sovereign sukuk programme that explicitly funds housing delivery for citizens is naturally positioned to attract this capital, particularly if structured with sustainability or social bond frameworks. Second, the structural growth of the Islamic finance industry, the Shariah-compliant asset pool that can only invest in instruments like sukuk continues to expand the captive demand base for high-quality sovereign sukuk, ensuring deep and stable demand for the Saudi programme's issuances over the multi-year horizon.

The Investment Case for Fixed-Income Allocators

For institutional fixed-income allocators pension funds, insurance companies, sovereign wealth funds, asset managers, and the Islamic finance institutions specifically the Saudi sovereign real estate sukuk programme presents a distinctive risk-return proposition that warrants specific analysis across four dimensions.

On credit quality, the programme offers exposure to Saudi sovereign or sovereign-guaranteed credit risk. Saudi Arabia carries strong sovereign credit ratings, and the explicit government guarantee structure demonstrated in the SRC precedent elevates the effective credit standing of the issuance to the sovereign level. For an allocator seeking high-grade emerging market sovereign exposure with a real-asset linkage, this is a structurally attractive credit profile investment-grade sovereign risk with the additional security of tangible asset backing, in a jurisdiction with a USD 1.3 trillion economy, exceptional fiscal capacity, and one of the world's strongest sovereign balance sheets through PIF's asset base.

On yield, the programme offers the GCC sovereign yield premium over comparable developed-market sovereign debt, in a hard-currency context (the riyal's dollar peg eliminates the currency volatility that characterizes most emerging market debt). The specific yield will depend on prevailing rate conditions at issuance and Al-Hogail's explicit statement that the Kingdom is awaiting geopolitical stabilization before launching reflects a deliberate strategy to issue when financing costs are favorable rather than at a moment of elevated risk premia. For allocators, this signals disciplined sovereign issuance management that prioritizes cost efficiency, which supports the long-term credit quality of the programme.

On portfolio diversification, the programme offers exposure to a real-asset-linked, Shariah-compliant, GCC sovereign instrument that has low correlation with the developed-market fixed-income and equity exposures that dominate most institutional portfolios. For a global allocator, Saudi real estate sukuk provides genuine diversification exposure to a distinct economy, a distinct asset class (real estate finance), and a distinct legal structure (sukuk) that is difficult to replicate through conventional instruments.

On the Shariah-compliant mandate specifically, the programme is one of the highest-quality sovereign-grade instruments available to the global Islamic finance industry. For takaful operators, Islamic banks, Shariah-compliant pension and sovereign funds, and the growing pool of Shariah-screened ESG mandates, high-grade sovereign sukuk with real-asset backing and a social-benefit purpose (housing delivery) is precisely the instrument these mandates are structured to hold. The captive demand from this segment provides a stable demand floor that supports pricing and liquidity across the programme's multi-year issuance schedule.

The Gaps and Risks That Define the Programme's Execution

For investors building a position around the sovereign real estate sukuk thesis whether in the sukuk instruments themselves or in the broader Saudi residential market, the programme is designed to support three execution risks that warrant specific analysis.

The first is the timing and rate of environmental risk. Al-Hogail's explicit statement that the Kingdom is awaiting geopolitical stabilization before launching the annual issuance programme reflects a real sensitivity: the cost of the programme is determined by the rate environment at issuance, and elevated global financing costs driven by both benchmark rates and the regional risk premium that geopolitical instability creates directly affect the economics. The risk for the programme is not that demand will be absent (the SRC precedent disproves that), but that the cost of capital at issuance could be higher than optimal if the geopolitical situation does not stabilize as anticipated. For investors, this timing sensitivity is a signal of disciplined issuance management, but it also means the programme's rollout pace is contingent on external conditions outside the Kingdom's direct control.

The second is the absorption and deployment risk. Raising SAR 20 billion per year through sukuk is only the financing side of the equation; the capital must then be deployed efficiently into housing delivery to generate the supply increase and the asset-backed returns that justify the instrument's structure. The Kingdom's housing delivery infrastructure ROSHN, the National Housing Company, the REDF, and the private developer ecosystem must absorb and deploy this capital into actual housing units at a pace that matches the financing inflow. Any mismatch between financing velocity and deployment velocity would undermine the programme's effectiveness and could create the perception of capital raised but not productively deployed. The institutional execution capacity of the Saudi housing delivery system is therefore a critical dependency.

The third is the interaction with the broader sovereign debt strategy. The IMF's 2025 Article IV mission explicitly noted the complex trade-offs between making greater use of central government deposits (currently around 9.25% of GDP) and new bond issuances, and the need to monitor contingent liabilities including financing obligations for giga-projects, debt guarantees, and PPPs. The sovereign real estate sukuk programme adds to the Kingdom's overall debt issuance, and while Saudi Arabia's debt-to-GDP ratio remains low by international standards, investors should monitor the aggregate sovereign and quasi-sovereign issuance trajectory to ensure the real estate sukuk programme is being executed within a coherent overall sovereign balance sheet management framework. The IMF's recommendation toward operationalizing a comprehensive sovereign asset-liability management framework is directly relevant to assessing the programme's long-term sustainability.

Conclusion: The Capital Stack Re-Architecture

Saudi Arabia's USD 40 billion sovereign real estate sukuk programme is best understood not as a single financing event but as a deliberate re-architecture of how the Kingdom finances its housing ambitions. For most of the Vision 2030 period, housing finance has flowed primarily through the banking system, bank mortgages to homebuyers, bank lending to developers, and SRC's liquidity provision to mortgage originators. That model has succeeded in driving homeownership from 47% to 66% and in expanding the mortgage portfolio to SAR 900 billion, but it has done so at the cost of mounting pressure on bank balance sheets that are simultaneously being asked to finance the largest infrastructure development program in the Kingdom's history.

The sovereign real estate sukuk programme resolves this tension by opening a direct channel from global institutional fixed-income capital to Saudi housing finance, a channel that scales the proven SRC precedent into a structural, multi-year, sovereign-directed mechanism. For the banking sector, it relieves the funding pressure that has driven the loan-to-deposit ratio to record levels. For housing delivery, it provides a stable, predictable financing base that is insulated from bank balance sheet volatility. For unit pricing, it supports the supply-side acceleration that moderates the demand-supply imbalance driving price appreciation. And for global institutional fixed-income allocators particularly the Shariah-compliant capital pool for which high-grade sovereign sukuk is the paradigmatic instrument it offers a distinctive combination of sovereign credit quality, real-asset backing, hard-currency stability, and exposure to one of the world's most actively developing housing markets.

The six-times oversubscription of SRC's first issuance demonstrated that the global appetite exists. The USD 40 billion programme is the Kingdom's decision to build a permanent capital markets channel on the foundation of that proven demand. For investors across the capital stack from the fixed-income allocators who will hold the sukuk to the residential real estate investors whose market will be shaped by the housing supply it finances, understanding this re-architecture is essential to positioning correctly in Saudi Arabia's evolving real estate economy.