A Correction by Design

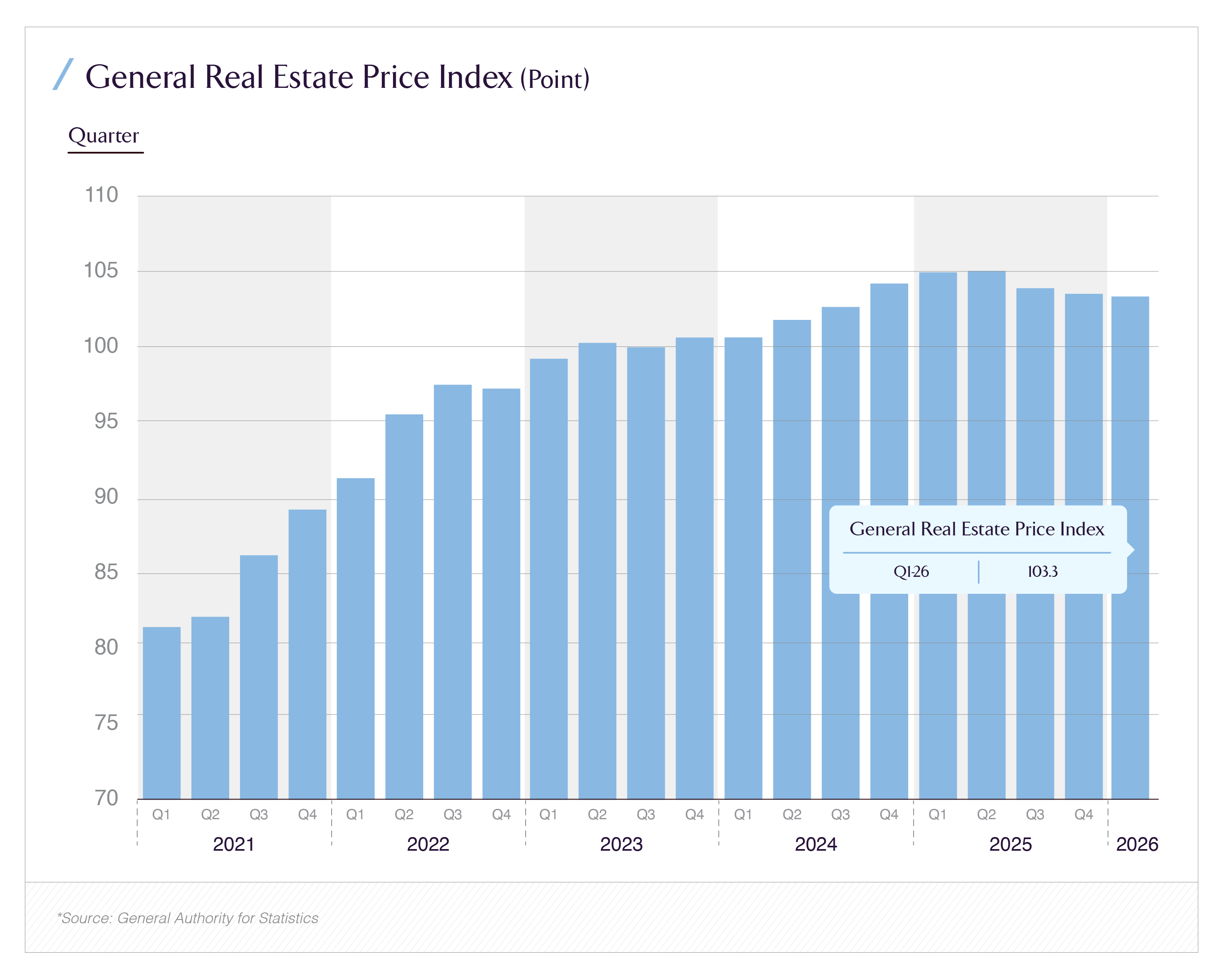

In May 2026, Saudi Arabia's real estate market produced the clearest dataset yet confirming a phenomenon that distinguishes it from virtually every other major property market correction in recent memory: this is a downturn that the government deliberately engineered, and is continuing to engineer, as a matter of explicit policy. The General Authority for Statistics' Q1 2026 figures show the national real estate price index down 1.6% year-on-year, with residential prices falling 3.6% and Riyadh values declining 4.4%. Residential transactions, according to Ministry of Justice data, halved against Q1 2025 just 29,000 homes sold, a 50% drop, with March 2026 transactions falling 62% year-on-year to 7,200 homes. Knight Frank's tracking of the same Ministry of Justice records put the national residential sales decline at 53%, with Riyadh specifically down a striking 83%.

For an investor trained on conventional real estate cycle analysis, these numbers would read as a crisis: a halving of transaction volume combined with falling prices is the textbook signature of a demand collapse, a credit crunch, or an asset bubble unwinding. But that interpretation would be analytically wrong in the Saudi case, and getting the interpretation right is the entire point of this article. This correction is not a demand shock. It is the intended outcome of a coordinated suite of government interventions the September 2025 five-year Riyadh rent freeze, the expansion and tripling of the White Land Fee, and now, finalized in May 2026, the extension of the fee regime to cover vacant built properties for the first time all explicitly designed by Crown Prince Mohammed bin Salman to address what he publicly described as an "unacceptable" level of house price growth and to force a recalibration of the market toward affordability.

The mechanism the government has now completed is the vacant property fee. In May 2026, the Ministry of Municipalities and Housing approved the executive regulations extending the White Land and Vacant Property Fees regime to cover unused built properties, adding a fee of 1% to 5% of equivalent rental value on buildings left vacant on top of the existing levy of up to 10% of land value on undeveloped land. Over 60,000 White Land Fee invoices have already been issued in Riyadh in the first 2026 billing cycle. This article examines what this regime does and why it forces supply into the market, analyzes the Q1 2026 correction as a policy outcome rather than a demand collapse, helps investors distinguish between a temporary correction and a structural repricing, and identifies which asset categories are most insulated from the engineered downturn.

The Vacant Property Fee Regime: How It Forces Supply Into the Market

The single most important regulatory development underpinning this correction and the one that distinguishes the Saudi approach from any conventional price-cooling intervention is the dual-layer vacancy fee architecture that the Kingdom has now completed. Understanding its mechanics is essential because it explains why this correction is structurally different from a cyclical downturn: the government is not merely cooling demand; it is actively forcing latent supply into the market.

The framework's legal foundation was laid on May 12, 2025, when the Saudi Council of Ministers issued Resolution No. 758 alongside Royal Decree No. M/244, approving substantial amendments to the original White Land Tax Law of 2015 and renaming it the "White Land and Vacant Property Fees Law." The amendments accomplished two things. First, they overhauled the existing white land fee the levy on undeveloped urban land replacing the previous flat 2.5% rate with a tiered structure ranging up to 10% of land value for maximum-priority development zones, scaling down to 2.5% for low-priority areas. This effectively quadrupled the maximum levy on undeveloped land in the most strategically important urban zones. Second, and more consequentially for the current correction, the amendments introduced for the first time a separate fee on vacant properties completed but unoccupied buildings at rates of 1% to 5% (with provision for up to 10%) of the property's equivalent annual rental value.

The implementing regulations for the white land component were published in 2025, and enforcement began in earnest with the January 2026 first billing cycle that issued over 60,000 invoices to Riyadh landowners. The vacant property fee executive regulations were finalized in May 2026, completing what one regulatory analysis aptly termed a "dual-layer vacancy control mechanism spanning the entire real estate lifecycle." The white land fee targets pre-development stagnation raw land held undeveloped for speculative appreciation. The vacant property fee targets post-construction inefficiency completed units held off the market, whether for speculative price appreciation or simply through inertia. Together, they make holding either undeveloped land or vacant completed buildings progressively expensive, creating a powerful financial incentive to either develop, sell, or lease the asset.

The supply-forcing logic is direct and deliberate. Saudi Arabia's real estate market, particularly in Riyadh, has historically been characterized by significant land banking by large landowners holding undeveloped urban parcels for long-term speculative appreciation rather than development and by a meaningful inventory of completed but deliberately unoccupied units held off the market in anticipation of further price gains. Both practices restrict effective supply and contribute directly to the price inflation that the government has identified as the problem. By imposing a continuous annual carrying cost on both undeveloped land (up to 10% of value) and vacant buildings (1-5% of rental value), the fee regime makes the hold-and-wait strategy financially unsustainable. Landowners subject to the fee must either pay the assessed amount, commence development within one year, or sell to someone who will. The regulations explicitly state their intent: to "encourage the utilization of vacant buildings and increase the supply of residential and commercial units, thereby helping to curb practices that negatively affect market equilibrium." The revenues collected are allocated to support housing projects, creating a self-reinforcing affordability mechanism.

This is the mechanism behind the transaction and price data. The 50% transaction slump and the price declines are not the symptoms of collapsing demand, they are the symptoms of a market in the early stages of a forced supply expansion meeting a deliberately moderated demand environment, with buyers and sellers repricing expectations as the new policy regime is digested. As more land is forced into development and more vacant units are forced onto the market over the coming years, the supply increase is designed to moderate prices toward the affordability levels that Vision 2030's 70% homeownership target requires.

Reading the Correction as Policy Outcome, Not Demand Shock

The analytical discipline this market demands is the ability to separate the policy-driven component of the correction from the genuinely demand-driven component because the two have entirely different implications for investment timing and entry. The Q1 2026 data, read carefully, reveals that both forces are present, but the policy component is dominant and the demand component is more nuanced than the headline numbers suggest.

The clearest evidence that this is a policy-driven correction rather than a demand collapse is the divergence between residential and commercial performance within the same GASTAT dataset. While residential prices fell 3.6% year-on-year in Q1 2026, commercial property prices rose 3.4% year-on-year, driven by a 3.6% increase in commercial land prices. If this were a broad demand shock, a recession, a credit crunch, a confidence collapse both segments would decline together. The fact that commercial real estate appreciated while residential corrected confirms that the residential decline is specific to the residential market, which is precisely the market targeted by the rent freeze, the affordability agenda, and the supply-forcing fee regime. Commercial real estate, which is driven by the corporate demand from the Regional Headquarters Program, the Grade A office shortage, and Vision 2030 business expansion, continued to strengthen because no policy intervention was directed at cooling it.

The regional divergence within the residential data tells the same story. The Eastern Region recorded the highest price increase in Q1 2026 at 6.9%, while Riyadh fell 4.4% and peripheral regions like Al-Baha (-9.2%), Hail (-8%), and the Northern Borders (-6.6%) saw the steepest declines. Riyadh's decline is the direct consequence of it being both the epicenter of the preceding price boom where apartment prices nearly doubled since 2019 and villa prices climbed over 50% and the primary target of the policy interventions, including the rent freeze and the most aggressive white land fee enforcement (the 60,000 Riyadh invoices). The capital's 83% transaction decline, far steeper than the 53% national figure, reflects a market where buyers, anticipating the supply increase and price moderation that policy is engineering, have rationally stepped back to wait for better entry points a transaction freeze driven by expectation, not by inability to transact.

Knight Frank's MENA research head Faisal Durrani articulated the underlying dynamic precisely: the slowdown was already underway before geopolitical tensions emerged in early 2026, and "housing affordability is at the heart of declining activity rather than geopolitics." Incomes have not kept pace with the house price growth of the preceding five years, which curbed transaction volumes and the government's intervention is explicitly designed to realign prices with the affordability ceiling. Knight Frank's research puts that ceiling at approximately SAR 1.5 million per home for Saudi nationals, with high-net-worth foreign buyers willing to stretch to around USD 1 million (SAR 3.75 million). The correction is the market moving toward these affordability anchors, pushed by policy and pulled by the income-price gap.

There is, however, a genuine demand-side component layered on top of the policy correction, and honest analysis must account for it. The early-2026 regional geopolitical tensions did dampen near-term transaction activity and investor confidence. March's 62% transaction decline, occurring after tensions escalated, was steeper than the quarter's overall 50% decline, suggesting a geopolitical overlay on the underlying policy-driven slowdown. This demand-side component is the more cyclical and reversible element: as the regional situation stabilizes, the geopolitical drag on transactions should ease, while the policy-driven structural recalibration continues on its intended multi-year trajectory.

Temporary Correction or Structural Repricing? The Critical Distinction

The most consequential analytical question for any investor evaluating entry into Saudi real estate in 2026 is whether the current correction represents a temporary, reversible dip after which prices resume their previous upward trajectory or a structural repricing that permanently resets the market to a lower, more affordable, more sustainable level. The answer determines everything about entry timing, and the evidence points clearly toward the latter with important nuances.

The historical precedent provides the base case. During Saudi Arabia's last major real estate downturn, from 2015 to 2019, residential property prices declined roughly 25% to 30% from peak to trough according to the GASTAT price index, and the recovery took approximately three to four years before the index returned to positive year-over-year growth, with a full rebound to pre-decline levels arriving only around 2022. That downturn, however, was driven by external macro forces collapsing oil prices and weak economic growth rather than by deliberate policy. The current correction is different in its causation, which changes its likely trajectory: because it is policy-engineered with a specific affordability target rather than macro-driven, its endpoint is not a return to the previous price levels but a stabilization at the new, lower, affordability-aligned level that the policy is designed to achieve.

This is the crucial insight for entry timing. The government's objective is not a temporary price dip followed by renewed appreciation; it is a permanent recalibration of price levels toward the affordability ceiling, accompanied by a structural increase in supply that prevents the return of the speculative dynamics that drove the 2019-2025 boom. An investor who treats the current correction as a temporary dip to be bought for a return to 2024 peak prices is misreading the policy intent. The more accurate framework is that prices in the most overheated segments Riyadh residential, particularly villas (which fell 6.1% in Q1 2026) and high-end apartments are being structurally reset to a sustainable level, and the investment opportunity is not a quick rebound trade but a long-term entry at post-correction prices into a market with genuine structural demand.

That structural demand is the reason the repricing is not a collapse. Even Knight Frank, documenting the 53% transaction decline, emphasizes that the medium-term outlook points to a continuing housing shortage: Saudi Arabia will require an estimated 830,000 housing units by 2034 simply to meet population growth needs. The demographic demand is real and durable, a population growing toward 40 million by 2030, household formation among a young population, and the homeownership target that remains national policy. The correction is therefore best understood as a transition: from a speculative, supply-constrained, price-inflated market to a higher-volume, better-supplied, affordability-aligned market. The price level resets downward, but the transaction volume and the structural demand recover and grow as affordability improves. The investor's entry point is into the new equilibrium, not back into the old peak.

The two-sided risk for investors is timing the bottom of the repricing. Enter too early while the supply-forcing fee regime is still pushing inventory onto the market and prices are still adjusting downward and the entry price will be above the eventual stabilization level. Wait too long until the affordability recalibration is complete and the foreign-ownership-driven demand wave (following the January 2026 foreign ownership law and the SAR-denominated target of USD 85 billion in annual foreign property investment by 2030) has begun to absorb the increased supply and the entry opportunity at trough prices will have passed. The optimal entry window is during the active repricing phase, in the specific asset categories where the structural demand is most durable and the policy-driven supply increase is least likely to create oversupply.

The Asset Categories Most Insulated From the Correction

Translating this analysis into actionable positioning requires identifying which asset categories are most insulated from the engineered correction and which carry the most exposure to it. The GASTAT data, the policy design, and the structural demand drivers together produce a clear hierarchy.

Logistics and industrial real estate is the most insulated category, because it is entirely outside the scope of the residential affordability agenda that is driving the correction. The policy interventions the rent freeze, the white land fee, the vacant property fee are oriented toward residential and, to a lesser extent, commercial real estate within urban boundaries. Logistics demand is driven by entirely different forces: the e-commerce expansion, the Vision 2030 manufacturing and industrial diversification agenda, the development of the Kingdom as a regional logistics hub, and the supply chain localization that Saudi industrial policy is driving. Logistics real estate in Saudi Arabia has experienced strong rental growth and occupancy, and none of the cooling measures directed at the residential market apply to it. For investors seeking Saudi real estate exposure insulated from the managed correction, logistics is the cleanest expression.

Grade A office is the second most insulated category, and the GASTAT data directly supports this: commercial property prices rose 3.4% year-on-year in Q1 2026 even as residential fell 3.6%, with commercial land up 3.6%. The Grade A office market in Riyadh is structurally undersupplied relative to the demand created by the Regional Headquarters Program (over 780 RHQs established by end-2025) and the broader corporate expansion, running at occupancy levels near 99% with rental growth that has outpaced almost every other real estate segment. The corporate demand driving Grade A office is contractually anchored (RHQ commitments are legally binding) and structurally growing, and it is entirely independent of the residential affordability dynamics driving the correction. The risk in office is the supply pipeline delivering over the next two to three years, which warrants attention to specific sub-market saturation, but the demand fundamentals remain among the strongest in the Saudi real estate market.

Mid-market residential is the most interesting category within the residential segment itself, because it is the direct beneficiary of the affordability agenda that is driving the correction in the premium segments. The policy interventions are designed to push the market toward the affordability ceiling of approximately SAR 1.5 million per home for Saudi nationals which means that residential product priced at or below this level, serving the genuine mass-market demand of the 830,000-unit structural shortage, is positioned to benefit from the affordability recalibration rather than be harmed by it. The villa segment (down 6.1% in Q1 2026) and the high-end apartment segment are bearing the brunt of the correction precisely because they were the most overheated and the most misaligned with affordability. Mid-market residential, by contrast, is where the policy-driven supply increase meets the most durable structural demand, and where the post-correction equilibrium is most favorable for well-positioned developers and investors.

The most exposed categories are speculative land holdings and premium/luxury residential in Riyadh. Speculative land is directly targeted by the white land fee the entire purpose of the up-to-10% levy is to make undeveloped land holding financially punitive. Premium and luxury Riyadh residential is the epicenter of the correction, having appreciated most during the boom and being most subject to the affordability recalibration. Investors holding these exposures should expect continued pressure as the policy regime runs its course, and investors considering entry should price in further downside in these specific categories before stabilization.

The Gaps and Risks in the Managed Correction Thesis

For investors positioning around this analysis, three risks warrant specific consideration before committing capital to the entry-timing thesis.

The first is the policy calibration risk. A government-engineered correction is, by definition, dependent on the government calibrating the intervention correctly, cooling prices enough to achieve affordability without triggering a deeper decline that damages developer balance sheets, undermines the construction sector, or creates negative equity dynamics for recent buyers. The aggressiveness of the white land fee (up to 10%), the addition of the vacant property fee, and the rent freeze together represent a powerful set of interventions, and the risk of overcorrection is real. Saudi Arabia retains the policy flexibility to moderate the interventions if the correction deepens beyond intent the fee tiers can be adjusted, enforcement can be paced but investors should monitor the policy signals carefully, because the trajectory of the correction is more dependent on government calibration decisions than on autonomous market forces.

The second is the supply-absorption risk. The fee regime is designed to force supply onto the market, and the foreign ownership law is designed to bring new demand to absorb it. The timing alignment between these two forces is critical: if supply is forced onto the market faster than the new foreign and domestic demand can absorb it, the result is a deeper and more prolonged price decline than intended. The approximately 63,000 homes scheduled for completion across 2026 and 2027, combined with the supply forced out of land banks and vacant inventory by the fee regime, must be matched by demand absorption from the foreign ownership opening and the affordability-driven domestic demand recovery. A mismatch in either direction: too much supply too fast, or demand absorption delayed by continued geopolitical drag would alter the correction's trajectory.

The third is the segment-specific oversupply risk. The hospitality supply analysis and the residential completion pipeline both point to specific sub-markets where supply is concentrated. Riyadh's residential completion pipeline, combined with the fee-forced supply increase, creates a genuine risk of localized oversupply in specific Riyadh sub-markets and product types particularly in the premium and villa segments that are already correcting most sharply. Investors must underwrite at the sub-market and product-type level rather than at the national or even city level, because the correction's impact is highly differentiated across these dimensions.

Conclusion: The Opportunity in the Engineering

Saudi Arabia's Q1 2026 real estate data tells a story that most cyclical analysis frameworks would misread. A 50% transaction slump and falling prices are not, in this case, the signature of a market in distress; they are the measurable output of one of the most deliberate, coordinated, and policy-driven market recalibrations any major economy has undertaken in recent years. The government identified house price growth as "unacceptable," set an affordability target, and deployed a precise toolkit: the rent freeze, the expanded white land fee, and now the vacant property fee explicitly designed to force supply into the market and reset prices toward sustainability. The correction is the intended result.

For investors, the implications are clear and actionable. This is not a market to fear, but it is a market to read correctly. The correction is structural rather than temporary in the overheated segments of Riyadh premium and villa residential where prices are being permanently reset toward the affordability ceiling, not temporarily dipped before renewed appreciation. The most insulated categories, logistics, Grade A office, and mid-market residential aligned with the affordability target offer exposure to Saudi real estate's durable structural demand without the policy-driven downside that the premium residential segment carries. And the optimal entry window is during the active repricing phase, in these insulated categories, before the foreign ownership demand wave and the eventual affordability-driven domestic recovery absorb the policy-forced supply increase and stabilize the market at its new equilibrium.

The investor who understands that Saudi Arabia is not experiencing a real estate crisis but engineering a real estate transition from a speculative, supply-constrained, inflated market to a higher-volume, better-supplied, affordability-aligned one is the investor positioned to enter at the trough of a managed correction into a market whose structural demand remains among the strongest in the world. The 830,000-unit shortage by 2034 has not gone away. The government has simply decided to meet it at prices its citizens can afford. That decision is the correction. And the correction is the opportunity.