The Largest Pharmaceutical Market in the Region and the Most Import-Dependent

Saudi Arabia presents one of the clearest structural paradoxes in the entire MENA healthcare investment landscape. It is the largest pharmaceutical market in the Gulf, accounting for approximately 29% of all pharmaceutical purchases across the GCC, with a market valued at USD 10.6 billion in 2025 and projected to reach USD 17.7 billion by 2035, according to Future Market Insights. It has the region's largest economy, its largest population, a rapidly modernizing healthcare system, and one of the world's most ambitious national transformation programs. And yet, despite all of these advantages, roughly 80% of the pharmaceuticals consumed in the Kingdom are imported, and only about 30% of medicines consumed are domestically produced. The Kingdom that aspires to be the region's healthcare and biotechnology hub remains, in the most fundamental sense, dependent on foreign manufacturers in the U.S., Europe, China, and India for the medicines its population requires.

This is not merely an inefficiency, it is a strategic vulnerability that Vision 2030 has explicitly identified and targeted. The COVID-19 pandemic demonstrated to every government in the world the national security dimension of pharmaceutical supply chain dependency, and Saudi Arabia internalized that lesson with characteristic ambition. The Kingdom has set an explicit industrial localization target to raise domestic pharmaceutical production from its current level toward 40% of total demand, with a parallel goal of localizing 70% of essential medicines by 2030. This is one of the most aggressive pharmaceutical localization agendas of any major emerging market, and it is now being backed by sovereign capital, regulatory reform, and a wave of multinational manufacturing partnerships that signal the early stages of a structural reconfiguration of the Saudi pharmaceutical value chain.

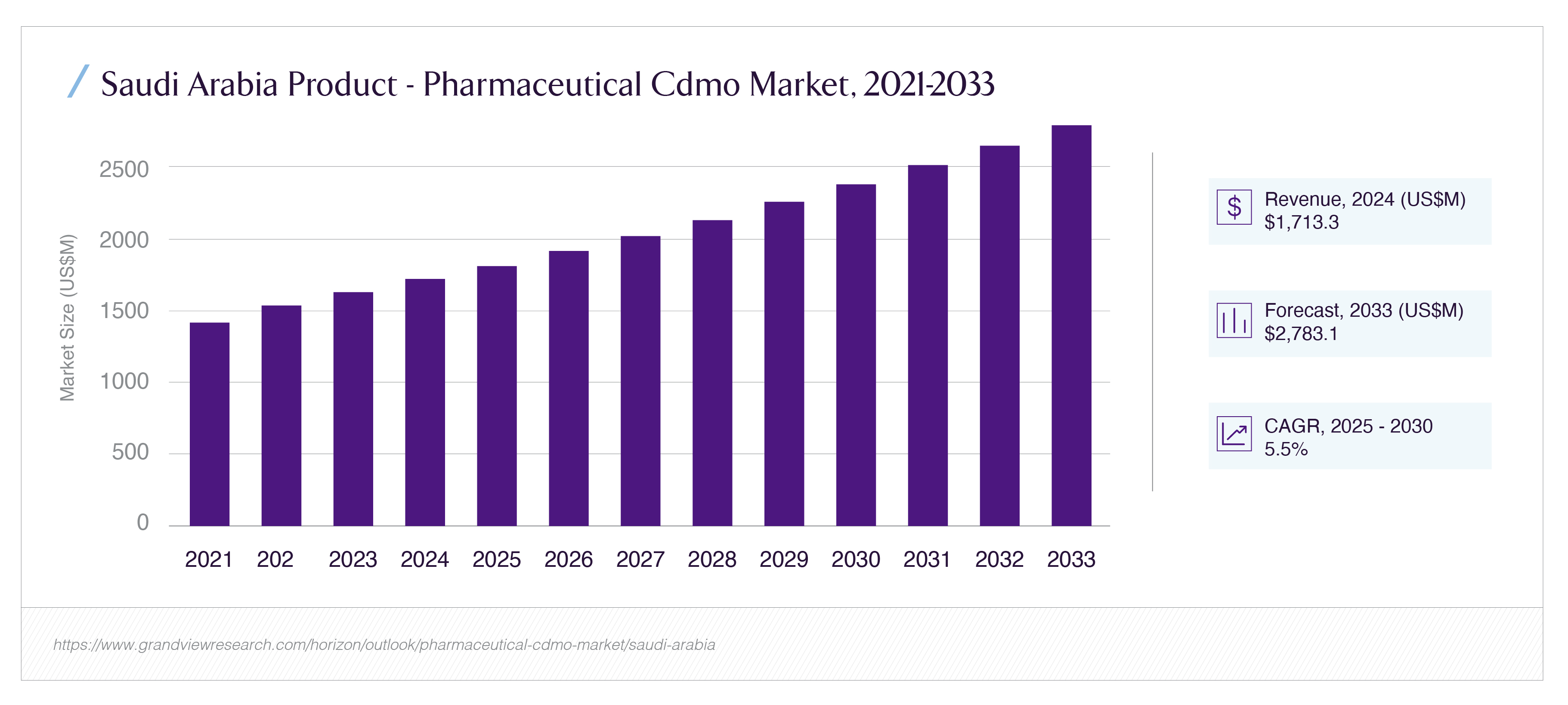

The capital has begun to move decisively. The Public Investment Fund established Lifera, a commercial-scale contract development and manufacturing organization (CDMO), to anchor the domestic biopharmaceutical industry. Pfizer, Novartis, Sanofi, and Novo Nordisk have all moved to establish or expand Saudi manufacturing arrangements. The Saudi Food and Drug Authority has approved over 55 pharmaceutical factories. And the CDMO market, specifically the contract manufacturing ecosystem that enables both multinational and domestic players to produce locally without each building dedicated facilities, sits at approximately USD 1.62 billion in 2024, projected to reach USD 2.24 billion by 2030 at a 5.45% CAGR. This article quantifies the import gap and explains why it persists, maps the regulatory and fiscal incentives drawing manufacturers in, examines the Lifera model and what it signals for CDMO partnership opportunities, and identifies where private capital can enter the pipeline across generics, biologics, and specialty drugs.

Why the Import Dependency Persists: The Structural Diagnosis

To understand the investment opportunity in pharmaceutical localization, an investor must first understand why the import dependency has persisted despite years of stated policy intent to reduce it. The answer lies in a combination of historical, economic, and structural factors that localization policy is now systematically dismantling.

The first factor is the economics of pharmaceutical manufacturing scale. Pharmaceutical production particularly for the branded, specialty, and biologic medicines that constitute the highest-value segment of the market is characterized by enormous fixed costs, stringent quality and regulatory requirements, and economies of scale that favor large global manufacturing facilities serving multiple national markets. For decades, it was simply more economical for global pharmaceutical companies to manufacture in centralized facilities in Europe, the U.S., and increasingly India and China, and export finished products to Saudi Arabia, than to build dedicated local manufacturing capacity for a single national market. The Saudi market, while large by regional standards, accounted for only approximately 0.7% of the global pharmaceutical market in 2024, not large enough, on its own, to justify dedicated local manufacturing investment under conventional commercial logic.

The second factor is the historical structure of the domestic industry. Saudi Arabia's existing local pharmaceutical manufacturers SPIMACO (Saudi Pharmaceutical Industries and Medical Appliances Corporation), Tabuk Pharmaceuticals, Riyadh Pharma, and Jamjoom Pharma have historically concentrated on generics and essential medicines, the lower-value, higher-volume segment of the market where local production is most economically viable. The high-value segment branded innovator drugs, biologics, biosimilars, and specialty therapies remained almost entirely the domain of imports, because domestic players lacked the technology, the regulatory track record, and the capital to manufacture these complex products, and global innovators saw no compelling reason to transfer that capability to Saudi Arabia. The result is a market where local production captures the low-value tail while imports dominate the high-value, high-growth segment precisely the inverse of what an industrial localization strategy requires.

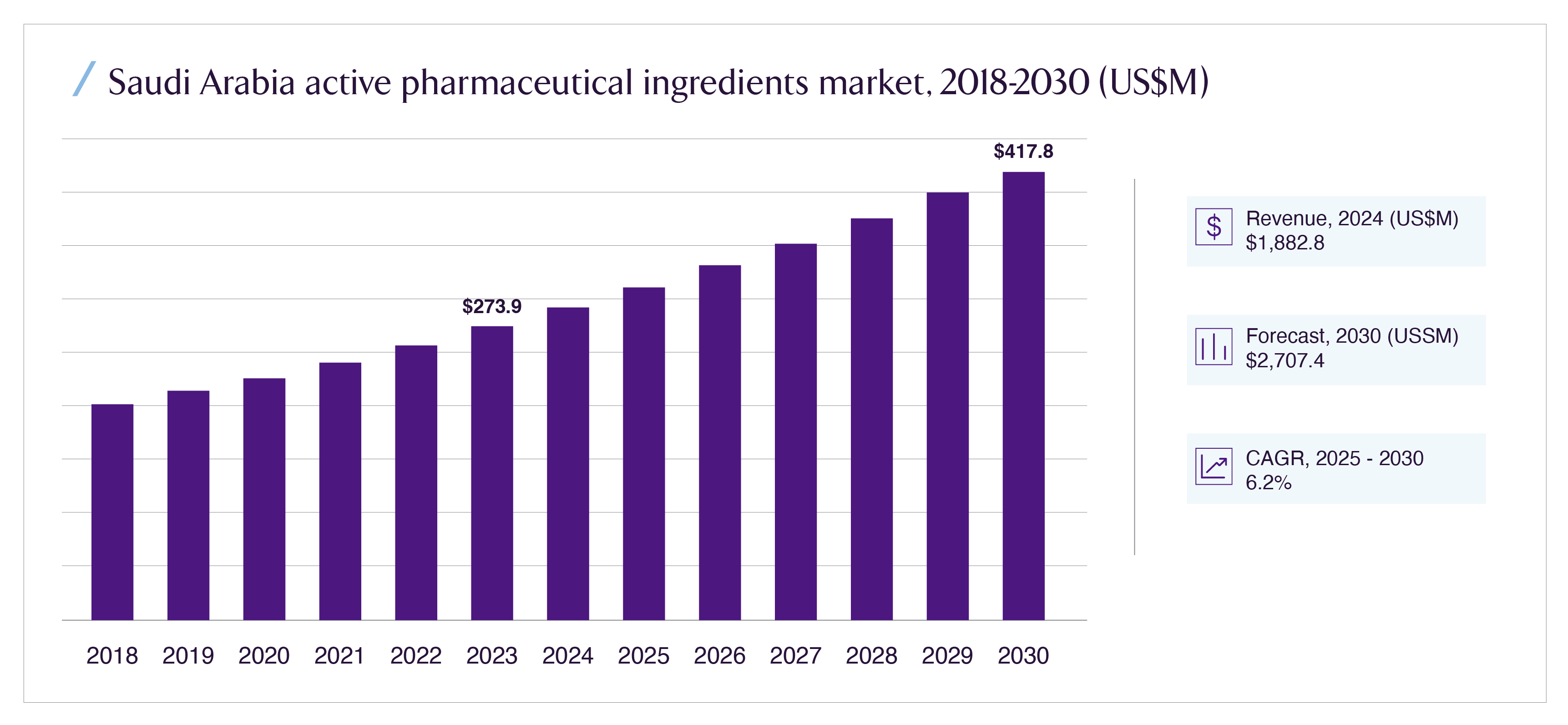

The third factor is the active pharmaceutical ingredient (API) dependency. Even the medicines that are "manufactured" in Saudi Arabia are frequently formulated from active pharmaceutical ingredients imported from abroad predominantly from India and China, which dominate global API production. Grand View Research's analysis confirms that the Saudi pharmaceutical industry is "primarily reliant on medicines imported from the U.S., Europe, China, and India," and that even domestic formulation depends heavily on imported APIs. This means that genuine pharmaceutical localization requires building not just finished-dose manufacturing but the upstream API and intermediate manufacturing capability, a far deeper and more capital-intensive industrial undertaking. The API segment is, accordingly, both the deepest gap and the most strategically valuable localization opportunity, which is reflected in the fact that API accounted for 81.39% of the Saudi CDMO market's revenue in 2024 and is identified as the fastest-growing segment.

These three factors together explain why import dependency has been so durable. They also explain why the current localization push is structurally different from previous efforts: it directly addresses each factor. The scale economics are being overcome by sovereign capital (PIF/Lifera) absorbing the fixed-cost investment that conventional commercial logic would not justify. The domestic industry structure is being upgraded through technology-transfer partnerships that bring multinational manufacturing capability into local joint ventures. And the API dependency is being targeted through explicit investment in upstream manufacturing capability under the National Biotechnology Strategy. The localization agenda is not asking the market to do what it has previously declined to do on its own; it is changing the underlying economics that previously made import dependency rational.

The Regulatory and Fiscal Incentives Drawing Manufacturers In

The mechanism converting Saudi Arabia's localization ambition into actual manufacturing investment is a coordinated suite of regulatory and fiscal incentives that materially change the commercial calculus for both multinational and domestic pharmaceutical companies. Understanding these incentives is essential for assessing the durability of the manufacturing investment wave and the opportunity it creates.

The first and most powerful incentive is procurement preference through NUPCO, the National Unified Procurement Company. NUPCO is the centralized procurement entity for Saudi Arabia's public healthcare system, which constitutes the dominant share of total pharmaceutical demand in the Kingdom. By directing procurement preference toward locally manufactured products guaranteeing volume offtake for medicines produced domestically NUPCO transforms the demand-side economics of local manufacturing. A manufacturer evaluating whether to build local capacity is no longer facing the uncertain demand of an open market; it is facing a guaranteed institutional buyer that has committed to preferentially purchasing locally produced medicines. This volume certainty is the single most important factor making local manufacturing investment commercially viable, because it resolves the demand risk that historically made dedicated local capacity uneconomic. Strategic agreements with NUPCO are explicitly transitioning pharmaceutical imports to local production.

The second incentive is the SFDA's streamlined and fast-track licensing framework. The Saudi Food and Drug Authority which has achieved World Health Organization Maturity Level 4 status, the highest global classification for regulatory systems, has developed expedited pathways for pharmaceutical registration and manufacturing licensing. Products already approved by recognized stringent regulatory authorities (the FDA, EMA, and other reference regulators) benefit from streamlined recognition pathways, reducing the time and cost of bringing locally manufactured products to market. The SFDA's approval of over 55 pharmaceutical factories demonstrates the throughput of this licensing infrastructure. For a multinational considering local manufacturing, the regulatory predictability and the expedited pathway materially reduce the time-to-revenue and the regulatory risk that would otherwise weigh against the investment.

The third incentive is the Vision 2030 industrial localization framework, including investment incentives, technology-transfer requirements, and the broader National Biotechnology Strategy. Saudi Arabia has committed over USD 65 billion to healthcare infrastructure investment under Vision 2030, and SAR 214 billion was committed to health and social development in 2024 alone. The industrial localization framework offers manufacturers a combination of capital incentives, access to PIF co-investment, industrial land and infrastructure in dedicated zones (such as the manufacturing clusters being developed in Sudair and around Riyadh), and the workforce development support necessary to staff advanced manufacturing facilities. Critically, the framework links market access to local investment: the implicit and increasingly explicit expectation is that multinational companies seeking to maintain and grow their share of the Saudi market, particularly their access to NUPCO procurement, will need to demonstrate commitment to local manufacturing and technology transfer. This transforms localization from a voluntary commercial decision into a condition of sustained market access, which is the most powerful incentive of all for companies whose Saudi revenues are material.

The demand-side fundamentals reinforce these incentives. Saudi Arabia's chronic disease burden is severe and growing: the National Health Survey found that nearly 19% of adults live with at least one chronic condition, with diabetes at 9.1% and hypertension at 7.9% among the most prevalent. These conditions require continuous, lifelong medication, creating predictable, recurring pharmaceutical demand that underpins the volume certainty local manufacturing requires. The expansion of universal health coverage under the National Health Insurance program will bring previously undertreated patients into the formal healthcare system, further expanding pharmaceutical demand. And the 40% increase in clinical trials in Saudi Arabia in 2024 (per SFDA data) signals the deepening of the broader pharmaceutical R&D and manufacturing ecosystem that makes local production increasingly viable.

The Lifera Model: What Sovereign-Anchored CDMO Signals for Partnership Opportunities

The single most important structural development in Saudi pharmaceutical localization is the establishment of Lifera, the Public Investment Fund's commercial-scale contract development and manufacturing organization. Understanding the Lifera model is essential because it reveals the mechanism through which Saudi Arabia intends to overcome the scale-economics barrier that has historically blocked localization, and because it defines the partnership opportunity structure that private capital and multinational manufacturers can access.

Lifera's strategic logic is to function as the sovereign-anchored manufacturing platform that absorbs the fixed-cost investment and demand risk that conventional commercial logic would not justify, and then to partner with global pharmaceutical companies to bring their products, technology, and manufacturing expertise into Saudi-based production. As a PIF entity, Lifera has access to patient sovereign capital that does not require the near-term commercial returns that a private CDMO would demand, allowing it to build manufacturing capacity ahead of demand and to absorb the early-stage losses inherent in establishing a new manufacturing base. This is the same sovereign-anchoring model that PIF has deployed across multiple Vision 2030 sectors using sovereign capital to create the infrastructure that catalyzes private and multinational investment that would not occur on its own.

The partnership wave Lifera has catalyzed demonstrates the model in action. In September 2023, Lifera and Resilience announced a joint venture to build a large-scale cGMP sterile injectables facility in Riyadh, including mRNA and monoclonal antibody production capability directly targeting the high-value biologics segment that has been entirely import-dependent. In May 2025, Lifera partnered with Novo Nordisk to localize the production of insulin and GLP-1 medications the latter being the explosively growing class of diabetes and obesity drugs (including semaglutide) for which Saudi Arabia, with its severe diabetes and obesity burden, represents a major and growing market. In 2025, Pfizer and Lifera signed a memorandum of understanding to explore local drug manufacturing and workforce development. And in October 2025, at the Global Health Exhibition in Riyadh, Lifera announced a potential joint venture with Jamjoom Pharma targeting the local development, manufacturing, and commercialization of vaccines, biologics, and biosimilars directly supporting the National Biotechnology Strategy.

The Lifera model signals a specific and replicable partnership opportunity structure for private capital and multinational manufacturers. The structure is a joint venture in which Lifera (or another sovereign-backed entity) provides the capital, the local infrastructure, the regulatory navigation, and the NUPCO procurement access, while the partner provides the product portfolio, the manufacturing technology, and the technical expertise. This structure resolves the key barriers for each party: the multinational gains guaranteed market access and a local manufacturing footprint without bearing the full capital risk, while Saudi Arabia gains the technology transfer and the local production capability it requires. For private equity and growth capital investors, the opportunity sits in the ecosystem around these joint ventures in the domestic CDMO operators (such as Tabuk Manufacturing Company), the specialty manufacturing capability providers, the cold-chain and pharmaceutical logistics infrastructure, and the contract research organizations that support the clinical and regulatory work the expanding manufacturing base requires.

Beyond Lifera, the broader localization ecosystem is attracting parallel investment that confirms the breadth of the opportunity. In December 2024, the Ministry of Investment announced a SAR 1 billion (USD 266 million) partnership with Vertex to build a gene and cell therapy manufacturing facility in Riyadh, complete with viral vector and cell production lines positioning Saudi Arabia in the most advanced and highest-value segment of the global pharmaceutical industry. In December 2024, Bio-Thera Solutions partnered with Tabuk Pharmaceuticals to manufacture and commercialize a ustekinumab biosimilar in Saudi Arabia. In June 2025, King Faisal Specialist Hospital and Research Centre and Germfree Laboratories announced the establishment of the first Advanced Therapy Medicinal Product (ATMP) manufacturing campus in Riyadh. Saudi Arabia launched its first dedicated oncology pharmaceutical plant in Sudair city. The pattern across all of these is consistent: the localization push is moving up the value chain, from generics toward biologics, biosimilars, cell and gene therapies, and specialty oncology the highest-value, highest-margin, and most strategically significant segments of the pharmaceutical industry.

Where Private Capital Can Enter: Generics, Biologics, and Specialty Drugs

For investors evaluating the pharmaceutical localization opportunity, the entry points differ substantially across the three principal product categories, each with a distinct risk-return profile, capital intensity, and competitive dynamic.

Generics represent the most accessible but most competitive entry point. Local generics manufacturing is the most established segment; the existing domestic players (SPIMACO, Tabuk, Riyadh Pharma) have decades of experience, and the technology and regulatory barriers are lowest. The localization push provides generics manufacturers with NUPCO procurement preference and volume certainty, improving the economics of capacity expansion. For investors, the generics opportunity is principally a consolidation and capacity-expansion play: backing the established domestic operators as they scale to capture the volume that localization policy is directing toward local producers, or supporting new generics capacity targeting the essential medicines list that the 70%-by-2030 localization target prioritizes. The returns are steady rather than spectacular, the demand is underwritten by NUPCO, and the competitive dynamic favors scale and operational efficiency. This is the lower-risk, lower-return tier of the localization opportunity.

Biologics and biosimilars represent the highest-growth and most strategically significant entry point, and the one where the Lifera-anchored partnership model is most active. Biologics complex, large-molecule drugs including monoclonal antibodies, insulin, vaccines, and advanced therapies constitute the fastest-growing segment of the global and Saudi pharmaceutical markets, and the segment where import dependency is currently most complete. The biologics and biosimilars CDMO segment is growing at approximately 9.8% CAGR, far outpacing the overall CDMO market, and it commands higher pricing, longer contracts, and deeper customer lock-in than generic manufacturing. The entry points include co-investment alongside Lifera and its joint-venture partners, investment in the specialized manufacturing infrastructure (sterile injectables facilities, viral vector production, cell production lines) that biologics require, and growth capital for the domestic players (such as Jamjoom Pharma) positioning to capture the biosimilar opportunity as blockbuster biologics lose patent protection. The capital intensity is high and the technical complexity is significant, but the strategic value and the growth trajectory are commensurately greater. This is the segment where the localization push is most transformative and where the highest-value opportunities concentrate.

Specialty and advanced therapies oncology drugs, cell and gene therapies, and other high-complexity, high-value medicines represent the frontier entry point, with the highest value per unit, the deepest current import dependency, and the most significant first-mover advantage. The Vertex gene and cell therapy facility, the KFSHRC ATMP manufacturing campus, and the Sudair oncology plant signal that Saudi Arabia is investing to build capability in precisely these segments. For investors, the specialty and advanced therapy opportunity is the most capital-intensive and the longest-horizon, but it is also the one most aligned with where global pharmaceutical value is migrating and where Saudi Arabia's combination of sovereign capital, severe disease burden (particularly in oncology and metabolic disease), and ambition to be a regional biotechnology hub creates the strongest case for first-mover positioning. The KFSHRC research and clinical ecosystem provides the clinical and scientific infrastructure that advanced therapy manufacturing requires, and the partnership models being established now will define the competitive landscape for a decade.

The cross-cutting opportunity across all three categories is the enabling infrastructure: the API and intermediate manufacturing capability that addresses the upstream import dependency, the pharmaceutical cold-chain and logistics infrastructure (the Saudi pharmaceutical logistics market is growing at 9% CAGR toward USD 1.19 billion by 2030), the contract research organization capability supporting the 40% annual increase in clinical trials, and the specialized workforce development and training infrastructure that all advanced manufacturing requires. These enabling layers are lower-profile than the manufacturing facilities themselves, but they are necessary conditions for the localization strategy to succeed, and they offer entry points with lower capital intensity and clearer near-term commercial models than the manufacturing facilities they support.

The Gaps and Risks in the Localization Thesis

For investors building a position in Saudi pharmaceutical localization, three structural risks warrant specific analysis before committing capital.

The first is the workforce and technical capability gap. Advanced pharmaceutical manufacturing, particularly biologics, biosimilars, and cell and gene therapies requires a deep pool of specialized technical talent: process engineers, quality assurance specialists, regulatory affairs professionals, and manufacturing scientists with experience in complex bioprocessing. Saudi Arabia's domestic pool of this talent is currently limited, and the CDMO market analysis explicitly identifies the skills gap as a constraint that "hinders the ability of CDMOs to scale up production, implement advanced manufacturing processes, and adopt new technologies efficiently." The reliance on foreign expertise and the cost of training and retaining qualified professionals adds operational complexity and cost. The localization strategy's success depends substantially on the parallel success of the workforce development programs, and investors should treat workforce capability as a key execution risk and a potential investment opportunity in its own right.

The second is the economic sustainability of subsidized localization. The sovereign-anchored model that overcomes the scale-economics barrier does so by deploying patient capital that does not require near-term commercial returns. This is a powerful catalyst, but it raises a long-term question: will the localized manufacturing capacity be economically self-sustaining once it must compete on cost with the global manufacturing scale of established import sources? If local production remains structurally higher-cost than imports as it may, given Saudi Arabia's smaller scale and higher labor costs relative to India and China then the localization will require continued procurement preference and implicit subsidy to remain viable. Investors should assess whether the specific manufacturing investments they are considering can achieve genuine cost competitiveness at scale, or whether they remain dependent on policy support that could change.

The third is the demand-concentration risk inherent in the NUPCO-anchored model. The volume certainty that makes local manufacturing viable derives substantially from NUPCO's procurement preference. This is a powerful demand underwriting, but it also concentrates demand risk in a single institutional buyer whose procurement policies, budget allocations, and preference frameworks could evolve. A manufacturer whose local production economics depend on guaranteed NUPCO offtake is exposed to changes in NUPCO's procurement strategy, pricing pressure, and budget constraints. Diversification of demand through private healthcare channels, export markets, and regional GCC sales is the mitigant, and investors should favor manufacturing investments with credible paths to demand diversification beyond the domestic public procurement channel.

Conclusion: From Import Dependency to Manufacturing Hub

Saudi Arabia's pharmaceutical import dependency 80% of drugs foreign-made, only 30% domestically produced is not a static market condition but a structural gap that the Kingdom has identified, targeted, and begun to close with sovereign capital, regulatory reform, and a coordinated industrial strategy. The gap exists because the economics of pharmaceutical manufacturing historically favored centralized global production over dedicated local capacity for a single national market. The localization push is succeeding because it is changing those economics: sovereign capital through Lifera absorbs the fixed-cost and demand risk, NUPCO procurement preference provides volume certainty, SFDA fast-track licensing reduces regulatory friction, and multinational technology-transfer partnerships bring the manufacturing capability that domestic players lacked.

The investment opportunity is real, substantial, and differentiated across the product spectrum. Generics offer a steady consolidation and capacity-expansion play underwritten by NUPCO demand. Biologics and biosimilars offer the highest-growth opportunity, anchored by the Lifera partnership model and growing at nearly double the overall CDMO market rate. Specialty and advanced therapies offer the frontier opportunity, with the deepest current import dependency and the strongest first-mover advantage. And the enabling infrastructure API manufacturing, cold-chain logistics, contract research, and workforce development offers lower-capital-intensity entry points across the entire value chain.

The CDMO market, growing from USD 1.62 billion toward USD 2.24 billion by 2030, is the structural entry point, the mechanism through which both multinational and domestic players can produce locally without each building dedicated facilities, and the layer where private capital can most readily access the localization opportunity. The Lifera model has demonstrated that the sovereign-anchored partnership structure can attract the world's largest pharmaceutical companies Pfizer, Novartis, Novo Nordisk, Vertex into Saudi-based manufacturing. The question for investors is no longer whether Saudi Arabia will localize pharmaceutical manufacturing, but how quickly, in which segments, and through which partnership structures the transition will occur. The Kingdom that has been the region's largest pharmaceutical importer is building the capability to become its manufacturing hub. The capital that positions in that transition now across generics, biologics, specialty therapies, and the enabling infrastructure is accessing one of the most strategically significant industrial localization opportunities in the global pharmaceutical industry.