The Paradox at the Center of Saudi Housing

There is a paradox sitting at the center of Saudi Arabia's housing market, one that has gone largely unpriced by institutional capital and largely unaddressed by policy. On one hand, the Kingdom has committed through its Vision 2030 framework to achieving a 70% homeownership rate among Saudi nationals, deploying resources through ROSHN, the Real Estate Development Fund (REDF), and the Saudi Real Estate Refinance Company (SRC) to make that ambition a reality. On the other hand, the structural conditions on the ground are quietly, systematically pointing in a different direction: toward renting, and toward a form of renting that the Saudi market has not yet learned to supply with institutional sophistication.

Mortgage penetration in the Kingdom stands at approximately 18% of GDP a figure that, while meaningfully higher than the 5% recorded a decade ago following the Mortgage Law reforms of 2012, remains well below the 50–80% range observed in comparable upper-middle-income economies. The 5% property transfer tax introduced in 2020 as part of fiscal consolidation has increased transaction costs for buyers, eroding affordability at the margin and systematically tilting the rent-versus-buy calculus for younger Saudis entering the labor market. In Riyadh, the Kingdom's primary economic engine, apartment rental rates rose by 19.6% year-on-year according to JLL's most recent data, while villa rents surged 17.2% over the same period. Supply is not keeping pace with the tenor or the quality of demand.

The consequence of these converging forces is a rental market projected to grow at a compound annual growth rate (CAGR) of 7.85% through 2031 (Mordor Intelligence, 2025), and yet the institutional response to that demand the purpose-built, professionally managed, amenity-rich residential rental community that has transformed real estate investment in the United Kingdom, the United States, Germany, and Australia is almost entirely absent from the Saudi market. Build-to-Rent (BTR), the asset class that has attracted over £40 billion in institutional capital in the UK alone since its inception, has no established market, no dedicated regulatory framework, and no standardized financing architecture in the Kingdom today. The Ejar platform recorded 3 million digital leases in 2024, up 35% year-on-year, creating an unprecedented data foundation for underwriting and yet no institutional actor has yet built the product to serve the demand those leases represent.

This analysis examines why BTR is the logical next asset class for institutional investors in Saudi Arabia: what the global evidence base tells us, where the regional landscape is heading, what Saudi-specific structural conditions make the case compelling, and where the gaps regulatory, financial, and operational still sit. The argument is methodological, grounded in verified market data, and oriented toward the investor who needs to understand not only whether the opportunity exists but how to access it and what to expect when they do.

The Global Build-to-Rent Phenomenon: Capital at Institutional Scale

To understand the Saudi opportunity, an investor must first understand why Build-to-Rent emerged globally and what distinguishes it from conventional residential. BTR is not simply a landlord owning apartments. It is an asset class defined by purpose-built design engineered for rental from day one, unified institutional ownership and management at scale, professionally underwritten returns, and a tenant experience calibrated to long-term retention. The distinction carries genuine economic weight: BTR assets consistently outperform buy-to-let residential portfolios on net operating income stability, void rates, and maintenance cost predictability because every element of the asset its physical design, amenity mix, lease structure, and service offering is optimized for the rental use case rather than retrofitted to it.

The United States built this asset class first. The American multifamily sector, encompassing purpose-built apartment communities under unified institutional ownership, constitutes one of the world's largest real estate investment universes. REITs, pension funds, sovereign wealth vehicles, and private equity real estate managers hold significant positions across the market, with operators such as AvalonBay Communities, Equity Residential, and Greystar operating portfolios spanning hundreds of thousands of units. The sector demonstrated exceptional resilience through the 2008–2009 financial crisis and accelerated dramatically in the pandemic's aftermath as remote work trends, lifestyle recalibration, and deepening affordability pressures drove demand for professionally managed rental housing in suburban and sunbelt markets at a pace that for-sale residential could not absorb.

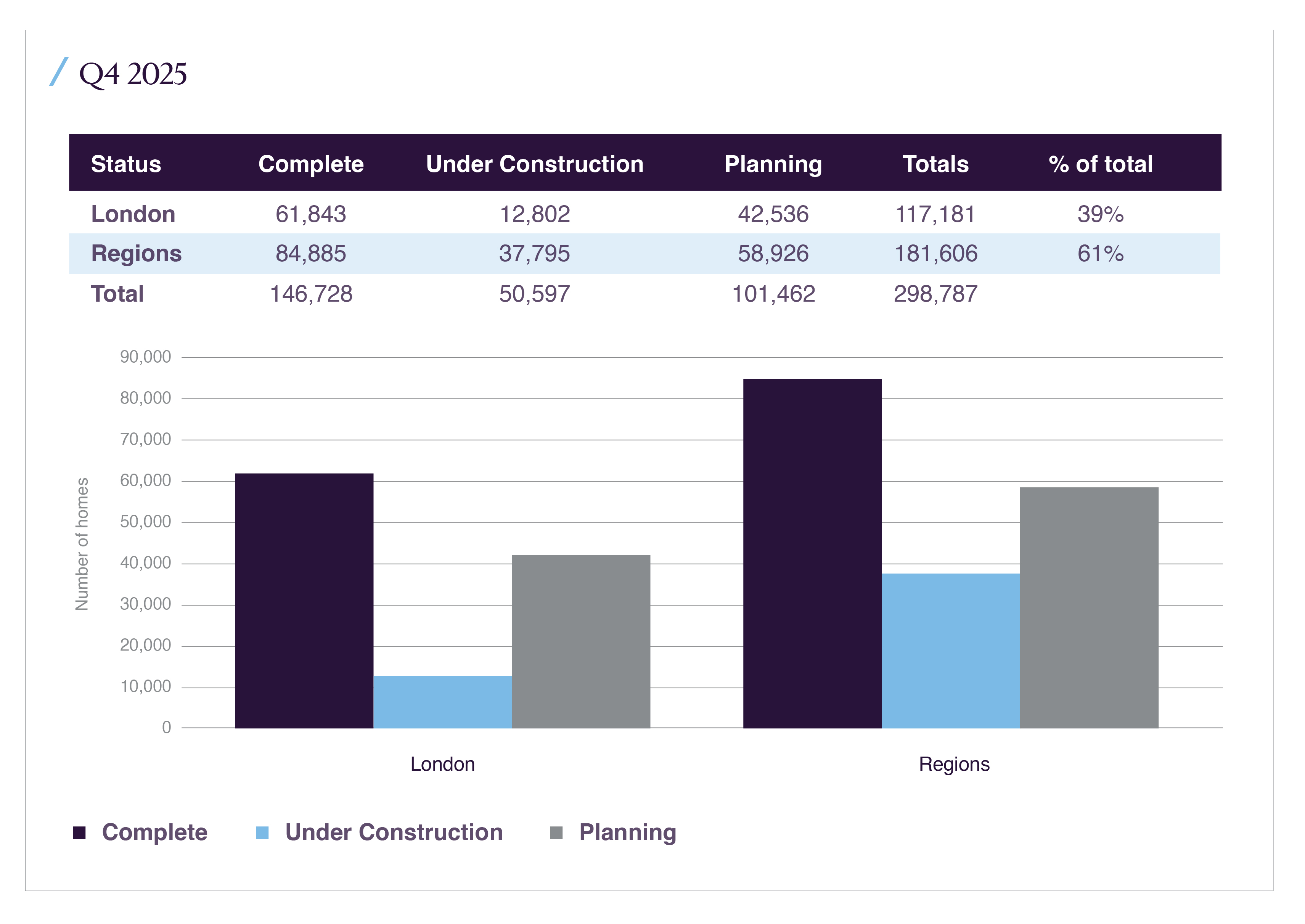

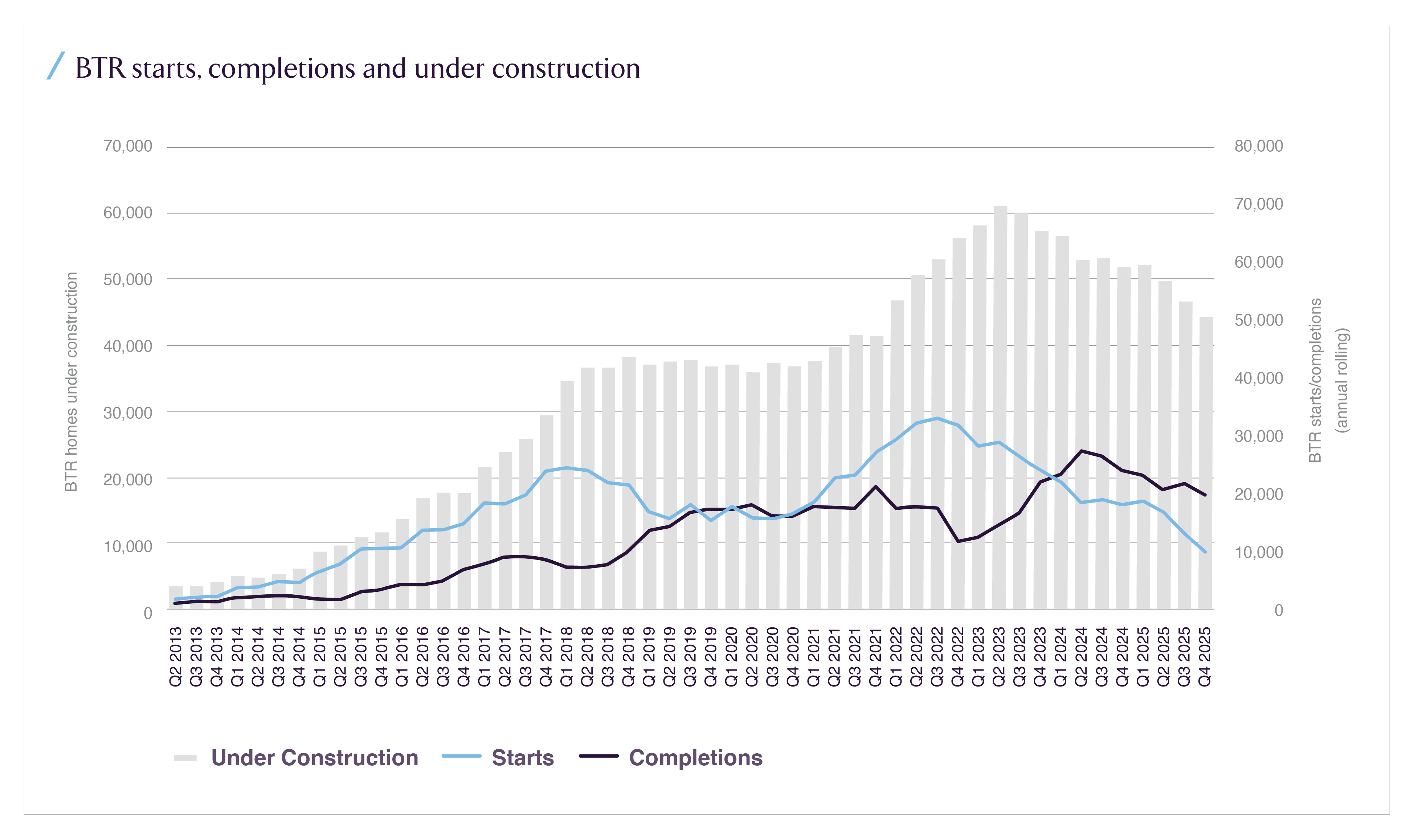

The United Kingdom offers the most instructive structural parallel for Saudi Arabia not simply because of the scale of its BTR market, but because of the speed and policy architecture through which the sector was catalyzed. As of Q4 2025, the British Property Federation and Savills' most recent quarterly dataset documents 146,700 BTR homes completed across the UK, representing 13% year-on-year growth, with an additional pipeline of completed, under construction, and planning-stage homes totaling over 273,700 units nationally. Since the sector's institutional emergence following the Montague Review of 2012, cumulative investment has surpassed £40 billion. Regional markets outside London have grown 18% year-on-year in completions as of Q1 2025, outpacing the capital's 13% growth rate, a sign that the asset class is deepening beyond its initial urban core into mainstream institutional territory. Most importantly, the BTR sector in the UK now accounts for one in ten of all new homes completed twice its contribution of five years ago cementing its status as a core component of institutional real estate portfolios alongside prime logistics and Grade A offices.

Germany's institutionalized Wohnen (residential) sector, Japan's purpose-built chintai housing model, and Australia's rapidly maturing BTR market each narrate a variation of the same structural story: when homeownership becomes structurally difficult whether due to price levels, transaction taxation, cultural evolution, or labor mobility demands purpose-built rental housing inevitably attracts institutional capital, generates stable income-producing assets, and matures into a recognized and independently traded investment category. The trajectory is not instantaneous, and it does not happen without regulatory enablement and capital market infrastructure, but the directional certainty has proven consistent across every major developed economy that has experienced it.

Most importantly for the Saudi context, this phenomenon is now expanding well beyond OECD economies. JLL's Global Living Investment Universe analysis, published in 2025, projects that over the next five years, $1.4 trillion will be deployed into living sector strategies globally encompassing BTR, multifamily, co-living, and single-family rental. Global living transaction volumes finished 2025 up 24% year-on-year according to JLL's most recent global market perspective data, with the US accounting for approximately two-thirds of total volume, EMEA representing 31%, and Asia-Pacific capturing the remaining 3%. That Asia-Pacific share is, by definition, the frontier of the frontier and the GCC sits even further ahead of where those flows are currently directed, which means the entry timing for an institutionally patient investor remains exceptional.

The asset class is globalizing. The question for Saudi Arabia is whether it will be a shaper of that wave or a recipient of it at compressed yields years from now.

Regional Landscape: The GCC's Structural Rental Economy

The GCC rental market is structurally unlike any other in the world, and understanding its particular characteristics is essential before mapping the BTR opportunity onto it. Across the six Gulf Cooperation Council member states, expatriate populations constitute anywhere from 38% to over 85% of the total population. These expatriates are, by definition, renters. They are contractually tied to employment geographies, cross-border mobile, generally unable to access long-term mortgage finance on the same basis as nationals, and across most of the Gulf restricted from purchasing freehold property except in designated investment zones. This creates a foundational rental demand base of a structural character that simply does not exist to anything like the same degree in European or North American markets, where institutional rental housing must compete for a population that has both the financial capacity and the genuine option to purchase.

The most developed institutional rental market in the region is the UAE, specifically Dubai, which has evolved a nascent managed apartment segment supported by RERA's regulatory framework, freehold zone structures, and a landlord-friendly legal environment that allows annual rent indexation. Aldar Properties in Abu Dhabi has made explicit strategic moves into the residential rental segment, acquiring and developing portfolio-scale assets with professional management overlays. Several international operators, including Greystar, have begun positioning managed apartment portfolios as institutional-grade assets in the UAE market. These developments do not yet constitute pure BTR in the institutional sense of unified ownership of purpose-built communities with full management infrastructure but they represent the directional precursor: the market demonstrating that managed residential rental can be an investable, scalable, and professionally operated product in the GCC context.

EMEA's living sector, which encompasses GCC markets, has experienced extraordinary capital flows. According to JLL's EMEA Living Market Perspectives 2026 data, living formed 30% of direct real estate investment in 2025, making it the largest real estate sector in EMEA for the second consecutive year. Private transactions rose 22% to €62.2 billion in 2025, with deals over €500 million more than doubling, reflecting the deepening conviction of large institutional capital in the residential rental thesis. Rental growth across European markets averaged 5.2% in 2025. Saudi Arabia's parallel data apartment rents in Riyadh up 19.6% year-on-year represents a structural mismatch between supply quality and demand intensity that is orders of magnitude more acute than the European conditions attracting this volume of capital. The regional implication is direct: if European living markets are attracting €62 billion in annual institutional investment at 5% rental growth, the Saudi market at four times that rental growth rate represents a dislocation that the right investment structure can capture.

Saudi Arabia: The Structural Case for an Entirely New Asset Class

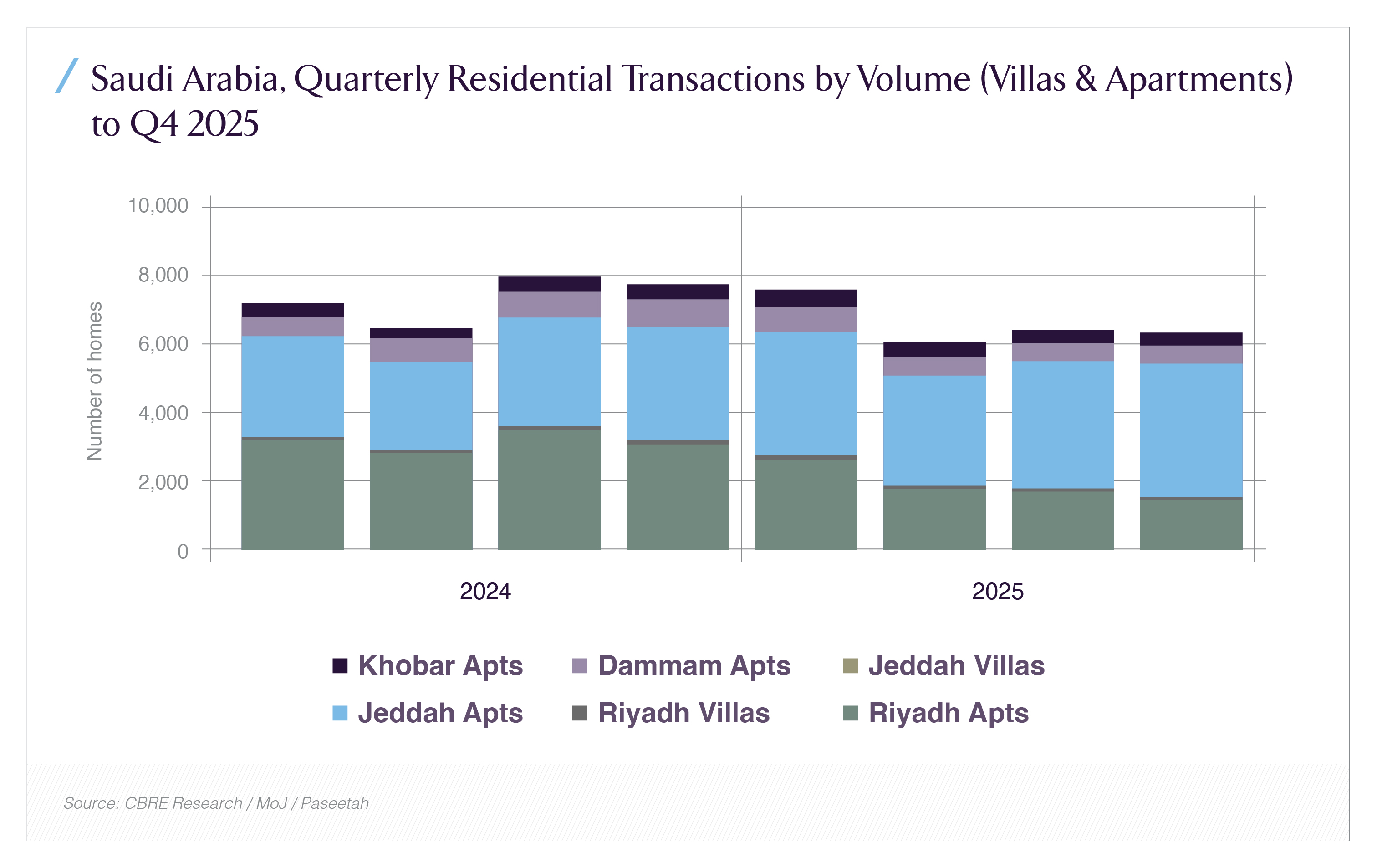

The Saudi rental market is large, growing, and deeply undersupplied in terms of the quality of product available at any price point. Saudi Arabia's total residential real estate market is estimated at USD 154.6 billion in 2025, expanding at a 6.70% CAGR to reach USD 213.9 billion by 2030 (Mordor Intelligence, August 2025). Within that total, the rental segment which held 35.4% of the market in 2024 is forecast to post the fastest growth of any sub-segment at a 7.85% CAGR through 2031. CBRE's Q4 2025 Saudi Arabia Real Estate Market Review, the most current comprehensive market analysis available, notes that the residential sector is "moving toward a period of stability" with approximately 70,000 units expected in Riyadh over the next two years, while the new foreign ownership law effective January 2026 is expected to act as a major demand catalyst as international residents gain the right to purchase in designated communities. Total residential transactions across Riyadh, Jeddah, and the Dammam Metropolitan Area reached 102,522 in 2024, with a total value of SAR 118 billion (approximately USD 32 billion), according to Deloitte's KSA Real Estate Market Review published in early 2025.

What is structurally important for the BTR thesis is not the transaction data per se, but what it reveals about the rental market's atomization. The overwhelming majority of rental supply in Saudi Arabia is owned by individual Saudi landlords, typically small investors holding one to five units in older residential buildings with no professional management infrastructure, no amenity provision, no service offering, and no institutional incentive to invest in maintenance beyond what is required to retain a tenant at minimum cost. Ejar recorded 3 million digital leases in 2024, up 35% year-on-year, an extraordinary volume of rental activity yet none of this volume is being served by purpose-built, institutionally owned, professionally managed rental products. The data infrastructure for institutional underwriting now exists, courtesy of Ejar's mandatory registration framework. The investment product does not.

The demand drivers for BTR in Saudi Arabia operate across three distinct but mutually reinforcing dimensions. The first is demographic. Saudi Arabia's population reached 35.3 million in 2024, growing 4.7% year-on-year (GASTAT). Critically, approximately 63% of Saudi nationals are under the age of 30, a cohort that is entering the labor market at a moment when housing affordability is under structural pressure from multiple directions simultaneously. Land prices in Riyadh's prime sub-markets have risen sharply over the past decade. Construction costs have increased with Vision 2030's demand for skilled labor and materials. The 5% property transfer tax adds a friction cost that disproportionately affects younger, first-time buyers who cannot absorb it against an accumulated equity position. For a 27-year-old Saudi professional earning SAR 9,000 per month, the combination of a 15–20% down payment requirement and a 5% transfer tax on every transaction means that homeownership remains a medium-term aspiration rather than an immediate possibility. In the interim, that professional needs somewhere to live that reflects their income level, lifestyle expectations, and quality standards and the current market cannot serve them.

The second driver is urbanization and internal labor mobility. Vision 2030's diversification ambitions, the expansion of the private sector, the development of tourism, entertainment, logistics, advanced manufacturing, and financial services across multiple cities are creating significant and sustained labor mobility within the Kingdom. A professional relocating from Jeddah to Riyadh for a role at a PIF-affiliated company, or from Riyadh to NEOM's emerging ecosystem, does not want to purchase property in a new city on arrival. A purpose-built rental community offering flexible lease structures, professional management, and lifestyle amenities serves that professional's needs in a way that the existing market cannot. The more mobile and diversified the labor market becomes, the more structurally important the rental sector becomes as economic infrastructure, not merely a consumer product.

The third driver is the expatriate workforce composition. Vision 2030's diversification ambitions require a sustained inflow of globally skilled talent engineers, financial professionals, technologists, healthcare specialists, educators who, even under the Kingdom's liberalized Premium Residency framework, will predominantly rent rather than purchase, at least initially. The premium and luxury rental segment in Riyadh is already under acute supply pressure: Grade A serviced apartments and villa compounds in Al Olaya, Al Nakheel, and the Diplomatic Quarter are commanding rents that reflect undersupply rather than equilibrium. Riyadh's office market, which CBRE Q1 2025 data confirms is running at 99% Grade A occupancy with rents surging 21% year-on-year, is a leading indicator of the residential demand that follows when a city transitions from a regional capital to a global business hub.

Rental yields in Saudi Arabia currently average 6.84% gross, according to the Global Property Guide's Q1 2026 survey data, with Riyadh Grade A apartments delivering approximately 6.8% in 2024 a spread of approximately 120 basis points above the 10-year Saudi government bond yield. This yield premium, combined with double-digit rental growth trajectories across prime segments, represents a real income-generating case for institutional investment that is materially more attractive than the sub-5% stabilized yields that BTR assets command in mature UK and European markets, where the consensus case for the asset class is made nevertheless.

ROSHN, the Public Investment Fund's wholly owned national housing developer, represents the closest existing analogue to what a large-scale BTR community could look like in the Saudi context. ROSHN's masterplan communities Sedra in Riyadh, Alarous in Jeddah, and multiple others in the active pipeline are designed as integrated neighborhoods with schools, retail, healthcare, parks, and community infrastructure embedded within the residential fabric. The model is sophisticated and the scale is ambitious: ROSHN holds a mandate to deliver 400,000 homes by 2030, with USD 400 million in construction contracts awarded in 2024 alone, according to Mordor Intelligence's 2025 analysis. However, ROSHN's current mandate is oriented primarily toward for-sale homeownership products; its primary customers are Saudi families purchasing under REDF-supported mortgage schemes. The BTR layer, a professionally managed, institutionally owned rental tranche within these masterplan communities does not yet formally exist, though the physical, planning, and community infrastructure for it is already in place within ROSHN's developments. The most operationally efficient path to institutional BTR in Saudi Arabia may therefore not be greenfield development from scratch, but the creation of dedicated rental tranches within existing masterplan ecosystems under long-term management agreements, a model proven extensively in the UK's mixed-tenure BTR market.

Financing Architecture, Regulatory Gaps, and the Path to Institutional Capital

Any institutional-grade asset class requires three enabling conditions to scale: a viable financing architecture, a regulatory framework that provides tenure security and operational clarity, and an exit mechanism that allows capital to recycle and markets to deepen. All three are underdeveloped in Saudi Arabia's BTR context, though the trajectory of progress on each front is positive and, in several dimensions, accelerating.

On financing, the Saudi Real Estate Refinance Company has successfully deepened the mortgage market for homeownership reporting a 16.4% increase in mortgage financing for housing support beneficiaries in 2024, reaching SAR 62.9 billion (USD 16.7 billion) according to REDF data. There is, however, no equivalent product for institutional rental finance. Permanent debt capital for large-scale residential rental assets the bread-and-butter financing mechanism for BTR in the UK and US, typically long-dated, fixed-rate senior debt from life insurers and pension funds, underwritten against stabilized rental cash flows does not exist in the Saudi market as a standardized product class. Corporate sukuk issuance and construction financing from local banks are available to developers, but the transition to long-term investment-grade debt backed by stabilized rental income requires either a specific SRC product for institutional rental financing, or the development of a private credit market for this asset class. Given the SRC's demonstrated capacity to create financial market infrastructure from scratch, a rental-backed refinancing product aligned to Ejar's data infrastructure would be a logical and high-impact next intervention.

On regulation, the Kingdom has made meaningful strides. REGA's comprehensive landlord and tenant regulations, progressively updated since 2021, provide clearer frameworks for dispute resolution and market transparency than existed even five years ago. The expanded White Land Tax detailed in August 2025 under a tiered rate structure targeting over 411 million square meters of undeveloped land is a supply-side lever that, if effectively enforced, will bring more developable land to market and reduce the land cost barrier for new residential construction. The five-year rent freeze introduced in Riyadh in September 2025 is a near-term demand stabilizer, though its longer-term implications for BTR underwriting specifically its impact on modeled rental growth assumptions warrant careful attention. There is, critically, no BTR-specific regulatory classification, no planning use class that distinguishes purpose-built institutional rental from general residential, and no concession framework for institutional landlords analogous to the UK's build-to-rent planning policies or the US's qualified residential rental project provisions. This definitional ambiguity creates friction for international institutional capital that requires precise legal classification before committing to a new asset class in a new jurisdiction.

On exit, Saudi Arabia's Tadawul-listed REIT market has 18 listed vehicles as of 2025 with aggregate market capitalization that remains thin relative to the size of the underlying real estate economy. No listed REIT has assembled a portfolio of residential rental assets at meaningful scale, and the sector lacks the depth and liquidity that would provide a credible exit mechanism for a large institutional BTR portfolio at stabilization. Breaking this circularity requires either PIF-anchored patient capital that absorbs first-mover development risk which is both feasible and consistent with PIF's demonstrated willingness to create market infrastructure in under-penetrated sectors or a regulatory incentive that reduces the transaction cost of injecting stabilized BTR assets into a REIT structure.

Defining the Investment Opportunity: Size, Yield, and the Case for First-Mover Conviction

For an institutional investor constructing a first principles view of Saudi BTR, the addressable market framework begins with Ejar's lease registry, which confirms the structural base of the urban rental population across Riyadh, Jeddah, and the Eastern Province. Even on conservative assumptions institutional BTR capturing a 5% share of total urban rental housing over a decade-long development horizon the investable universe exceeds 50,000 purpose-built units. At average development costs of SAR 500,000–750,000 per unit for mid-to-premium specification apartments, this implies a development investment horizon of SAR 25–37 billion, or approximately USD 7–10 billion. This is meaningful but entirely achievable for a market with PIF's sovereign capital base, the existing masterplan infrastructure of ROSHN, and the growing appetite of international institutional capital for GCC residential exposure.

On returns, gross rental yields averaging 6.84% in Q1 2026 (Global Property Guide) and net yields in the 4.5–5.5% range for well-located, professionally managed product compare favorably to both core commercial real estate in the Kingdom and to BTR yields in mature markets. UK BTR stabilized yields have compressed to the 4–4.5% range in prime locations, with investors accepting lower current income in exchange for inflation-linked rental growth, capital value appreciation, and long-duration income streams. Saudi Arabia's yield premium over those mature market benchmarks remains substantial, its near-term rental growth trajectory is materially stronger, and its currency risk is eliminated by the riyal's dollar peg a structural advantage that no floating-currency emerging market can replicate.

The risk framework is grounded but manageable. Demand risk is low in the conventional sense: the tenant base of young Saudi professionals, expatriate workers, corporate relocators is structural and growing, supported by demographic momentum and Vision 2030's labor diversification agenda. Regulatory risk is real for first-mover capital but is best managed through partnership structures that embed sovereign or quasi-sovereign anchors, reducing the jurisdictional uncertainty discount. Execution risk is the most significant constraint: the absence of a domestic BTR operational ecosystem means that a first institutional platform must import capability Greystar's model of entering new markets through management agreements is the most immediately accessible template or build it domestically, which carries higher cost and longer timeline. A joint venture structure between an international BTR operator and a Saudi masterplan developer, structured with a PIF-adjacent anchor and a clear sukuk-financing pathway for stabilized assets, is the most credible near-term institutional architecture.

The operational ecosystem will develop once the capital moves. It has in every other market where BTR has taken root, and Saudi Arabia's track record of constructing institutional infrastructure rapidly from the REIT framework to Ejar's digital lease registry to the SRC's mortgage securitization market, all created within a decade suggests that the operational gap is a starting-line constraint rather than a structural ceiling.

The Gaps That Define the Opportunity

The most consequential gap is not financial, it is conceptual and advocacy-based. Saudi Arabia's real estate sector, its regulators, its institutional investors, and its development community have not yet developed a shared mental model of what BTR is, why it is distinct from general residential development, and why it merits a dedicated policy and investment framework. In the UK, the intellectual groundwork for BTR was laid by the Montague Review years before the first institutionally owned BTR scheme was completed. In Australia, the Property Council's sustained advocacy for a BTR-specific tax framework preceded the first major institutional commitments by nearly five years. In Saudi Arabia, that groundwork is only beginning to emerge. REGA, MoMRAH, and the SRC have both the institutional mandate and the data infrastructure through Ejar's 3 million registered leases to lead a structuring conversation. What is needed is a private-sector investment thesis brought to that table with the analytical rigor and global comparative evidence that public-sector counterparts can act on.

The second gap is data granularity. Ejar's registration framework has been transformative, but the Saudi rental market's data architecture is not yet at the sub-market, unit-level precision that sophisticated BTR underwriting demands. Vacancy rates by sub-market, tenant profile analytics, unit-level rental growth series, and lease duration distributions are not systematically available in a commercially accessible format. Building that data product is itself a pre-competitive infrastructure project, one that REGA is best positioned to lead, and that institutional investors have a direct interest in funding or advocating for.

The third gap is operational. There is no domestic BTR property management ecosystem no operator with experience in large-scale, professionally managed residential rental communities, equipped with the service culture, digital infrastructure, preventive maintenance systems, and tenant retention practices that institutional-quality BTR requires and that underpins its superior operational economics relative to the atomized private landlord model. This gap will close as the sector develops; it has closed in every comparable market. But it is a genuine near-term cost center, and any underwriting model for the first generation of Saudi BTR platforms must account for the cost and time required to build or import that capability.

Conclusion: The Window Is Open, but It Will Not Stay Open Indefinitely

Saudi Arabia's Build-to-Rent market sits today at precisely the inflection point that characterized UK BTR in 2012, Australian BTR in 2018, and the broader EMEA living sector in 2015: the structural demand is unambiguously present and quantifiable, the policy intent is favorable, the capital is available in principle, and the regulatory framework is incomplete but improvable on a credible timeline. The Ejar platform has created the data foundation. Vision 2030 has created the demand catalyst. ROSHN has created the masterplan infrastructure. The sovereign balance sheet has created the anchor capital potential. What has not yet been created is the investment product itself, and the institutional vehicle through which capital can be deployed into it at scale.

The investor who commits to first-mover positioning in this environment who is willing to work with regulators to shape the definitional framework, partner with ROSHN or an equivalent masterplan developer to access pipeline, import international operational expertise through a management agreement structure, and design a vehicle with a credible exit path through the Tadawul REIT market will be positioned to define the asset class in the Kingdom's institutional landscape for a decade. The downside of moving early is a longer-than-projected stabilization timeline in a market where the underlying demand is structural and durable. The risk of moving too late is more consequential: in a market where PIF's appetite for infrastructure-creating investment is well-documented and international capital is beginning to pay serious attention to Saudi real estate CBRE's Q4 2025 review notes the new foreign ownership law effective January 2026 as a "major catalyst for activity" the window for first-mover economics will compress rapidly once the regulatory framework closes and the sector's contours become defined by others.

The Kingdom is building its cities, its economy, and its institutional landscape at a speed that has no precedent in modern economic development history. The question for real estate capital is whether it will also build the housing infrastructure that a modern, mobile, aspirational, and rapidly urbanizing population actually needs not what policy says people should want, but what demographics, economics, and structural market conditions are increasingly making the rational and necessary choice. Build-to-Rent is that answer. The market is waiting. The opportunity will not wait indefinitely.