When Gaming Stops Being “Extracurricular”

In February 2026, Saudi Arabia’s education authorities moved video games from the margins of youth culture into the core of schooling. Through a set of memoranda of understanding with Savvy Games Group and national curriculum bodies, game development and esports are being integrated into the national curriculum across multiple education levels.

This is not a light-touch “edutainment pilot.” It is a formal policy decision that:

- embeds game design, coding, digital art, and esports operations into curriculum frameworks;

- leverages existing digital infrastructure, most notably the Madrasati e-learning platform; and

- links classroom activities to a broader industrial strategy around gaming, esports, and the creator economy.

For investors, this is a human-capital story rather than a narrow education anecdote. The move repositions “gaming” as a skills pathway into software engineering, 3D content, live operations, and data analytics capabilities that sit at the intersection of digital economy, AI, and media.

The key questions, from a Saudi-focused capital-allocation lens, are straightforward:

- How large and durable is the global demand signal behind these skills?

- How does Saudi’s digital-education and skills baseline compare to peers?

- What does the curriculum shift practically change in the country’s talent pipeline?

- Where do the risks sit in pedagogy, infrastructure, and equity of access?

- And where, concretely, might capital find opportunity along this transition?

The rest of this piece addresses those questions in sequence.

Global Landscape: Gaming, Skills, and the Creator Economy

Globally, the decision to treat gaming as an educational domain rather than a distraction is not happening in a vacuum. The video-games industry is one of the most scaled digital sectors, both in revenue and in time-spent terms.

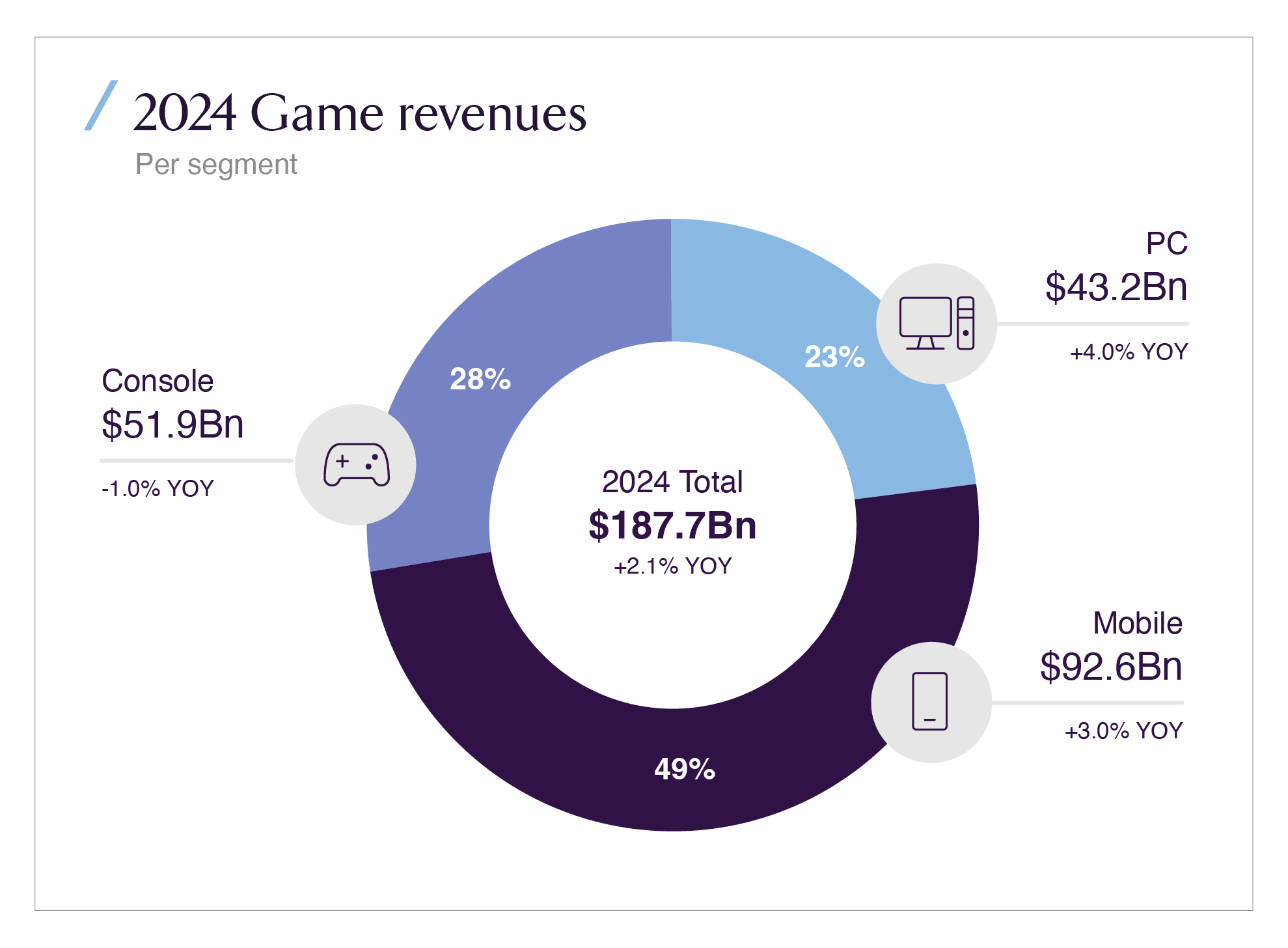

Newzoo’s 2024 Global Games Market Report estimates that the games industry generated roughly $187.7bn in revenue in 2024, up about 2.1% year-on-year. Mobile accounts for around $92.6bn (49% of the total), consoles for $51.9bn (28%), and PC for $43.2bn (23%). This is not a niche creative hobby; it is a capital-intensive, data-rich ecosystem with complex value chains: engines, tools, publishing, hardware, advertising, live operations, and user-generated content.

The visual shows PC, console, and mobile revenues by year with forecasts to 2027, highlighting the scale and growth profile of the sector.

The same tools and workflows that underpin commercial games engines, asset pipelines, real-time rendering, multiplayer netcode are increasingly the backbone of other industries: simulation, digital twins, virtual production, and immersive training. As a result, “games literacy” maps into:

- software engineering and scripting;

- 3D modelling and animation;

- systems thinking and live-ops analytics;

- community and content moderation; and

- IP and rights management in user-generated ecosystems.

In parallel, the broader creator economy has become a material labour-market phenomenon. While estimates vary, many global analyses converge on creator-economy revenues in the low-hundreds-of-billions of dollars, with gaming and game-adjacent content (streams, esports broadcasts, modding, machinima) among the fastest-growing slices. For education systems, the question is no longer whether students will engage with these platforms, but whether their interaction will be channeled into durable skills rather than purely consumption.

The policy logic behind Saudi’s move is therefore straightforward at the global level: if an industry this large is already shaping young people’s time and aspirations, steering it into formal skill-building is a rational human-capital play.

Regional Context: MENA’s Youth, Digital Adoption, and Skills Appetite

The MENA region is heavily skewed toward youth, with a large share of the population under 30 and high adoption rates of smartphones, social platforms, and online video. Gaming has ridden that wave, with countries such as the UAE, Saudi Arabia, and others frequently cited among the fastest-growing games and esports markets in emerging regions.

From a skills perspective, one useful proxy is the share of the labour force engaged in structured online learning. Coursera’s Global Skills Report 2024 ranks countries by the percentage of their labour force active on the platform. Globally, about 0.73% of the labour force is active; several MENA countries sit significantly above that baseline.

Saudi Arabia appears in the global top-20 for “online learners as a percentage of the labour force,” with roughly 1.07% of its labour force active on Coursera alongside the UAE at 2.07%. This signals that:

- there is already meaningful adult demand for digital learning; and

- The region’s workforce is not starting from zero in terms of comfort with online platforms and self-paced skills development.

The chart lists countries by share of the labour force active on Coursera, with Saudi Arabia at 1.07% versus a global average of 0.73%.

For investors, this matters because the success of any curriculum reform that leans on digital tools, new content formats, and emerging industries depends on three things:

- Baseline digital adoption are households, teachers, and students already working through screens and platforms?

- Cultural legitimacy of online learning is there a stigma, or is online training seen as a legitimate complement to formal study?

- Regional competitive pressure are neighbouring countries moving in similar directions, creating talent pull-and-push dynamics?

On all three, Saudi and the wider GCC now operate closer to the OECD norm than to a typical emerging market. That makes curriculum-level integration of gaming less of an experiment and more of an extension of ongoing digitisation.

Saudi Baseline: Digital Education and Policy as an Operating System

Saudi’s gaming-curriculum decision rests on a decade of digital-education infrastructure build-out. The Madrasati platform rolled out at scale during COVID and retained as a core system has become one of the largest national digital-education platforms globally.

The Digital Government Authority’s Q3 2024 Digital Saudi newsletter reports that Madrasati has logged roughly:

- 7.2 billion visits;

- 2.2 billion exams completed by male and female students;

- 6.4 billion assignments;

- 537 million virtual classes; and

- 2.5 billion educational activities.

These are not experimental numbers. They demonstrate that Saudi’s school-age population, teachers, and administrators can already operate at national-scale volumes in a digital environment.

Two points follow for the gaming-curriculum change:

- Delivery rail is mature. Integrating game-based modules, esports competitions, or project-based assessments into Madrasati is an incremental content and UX challenge, not an infrastructure one.

- Data exhaust is rich. Billions of completed digital activities already generate granular learning data. Adding game-based tasks expands that data into new dimensions: collaboration, problem-solving, persistence, and multi-modal creativity.

At the policy level, Saudi has also positioned itself as a digital-government and digital-experience frontrunner. DGA’s indices show the Digital Experience Maturity Index reaching an “advanced” score of roughly 85% in 2024, with platforms like Tawakkalna, Absher, and Visit Saudi ranked among the leading digital services. That governance and UX discipline is important because game-based curricula rely on secure accounts, identity, and safe online environments where Saudi has already built capabilities through other platforms.

In short, when Saudi decides to add gaming and game development to the curriculum, it is doing so on top of a functioning digital-education “operating system,” not in a vacuum.

The Reform Itself: What “Gaming in the Curriculum” Actually Means

Public reporting around the February 2026 decision highlights three main strands of the initiative:

- Curriculum integration. Game development and esports are being written into the national curriculum, not just offered as extracurricular clubs. That includes modules on coding, game-engine use, digital art and animation, narrative design, and competition strategy.

- Institutional partnerships. The Ministry of Education has signed MoUs with Savvy Games Group and key educational organisations (including the National Institute for Professional Development in Education and Tatweer Educational Services). The goal is to create interactive content, establish digital labs, and train both students and professionals.

- Platform embedding. Games and game-based learning will be embedded into Madrasati and possibly other national platforms, tying day-to-day classroom practice to the broader digital-government stack.

In other words, the move is not simply “play more educational games in class.” It is a structured attempt to:

- treat game engines as core creative-technology tools, analogous to CAD for engineers or DAWs for music;

- link esports to teamwork, strategy, and tournament operations rather than casual play; and

- surface career pathways in programming, art, production, shout-casting, event management, and digital marketing.

This is also aligned with Saudi’s wider gaming and esports strategy. Public-investment commitments to gaming, plus moves to attract game studios and publishers, have already been documented; the curriculum reform effectively pushes talent-pipeline development earlier into the schooling journey.

Challenges: Pedagogy, Capacity, and Equity

From an investor’s perspective, the upside is clear. But there are non-trivial execution risks that will shape how quickly the reform translates into real skills and economic outcomes.

1. Teacher readiness and instructional design

Most teachers were not trained to teach game development, game design, or esports strategy. High-quality implementation will require:

- large-scale professional development to move teachers from “users of games” to facilitators of project-based, interdisciplinary game work; and

- curriculum resources that are outcome-aligned, assessment-ready, and usable across very different school contexts.

Without that depth, “gaming in the curriculum” risks becoming superficialeither entertainment dressed up as education, or rote assignments thinly wrapped in a game veneer.

2. Infrastructure and hardware unevenness

Madrasati’s reach is national, but the hardware and bandwidth needed for full 3D game-engine work or competitive esports play are not uniformly distributed across schools and regions. The risk is a two-tier system:

- well-resourced schools offering full lab-based, team-oriented game development experiences; versus

- more constrained schools limited to lightweight tools that do not fully build the targeted skills.

That gap can reinforce the very inequities the reform is meant to address.

3. Content standards, safety, and IP

Game-based learning introduces exposure to user-generated content, online communities, and potentially commercial platforms. The regulator’s challenge is to:

- define acceptable content and interactions in school contexts;

- manage licensing and IP around student-created assets and games; and

- keep a clear boundary between educational objectives and commercial promotion.

Saudi’s broader digital-safety and data-governance frameworks offer a starting point, but educational settings have specific sensitivities particularly around minors, streaming, and public sharing of student work.

4. Assessment alignment

Traditional assessment systemsexams, short-answer questions, standardized testsare poorly suited to measuring the competencies game-based learning is supposed to build: systems thinking, collaboration, iterative design, and creative production.

Unless assessment evolves, there is a risk that game-based modules become “nice extras” that students and schools deprioritise when exam pressure mounts, diluting the economic rationale for the reform.

Solutions and Design Choices: How This Can Work at Scale

The policy architecture already gestures at several ways to mitigate these risks and translate intent into outcomes.

Anchoring gaming in existing digital-education rails

By embedding game content in Madrasati rather than fragmenting across disparate apps, Saudi can:

- centralise authentication and identity;

- re-use existing analytics pipelines; and

- keep teacher workflow simple (one login, one core interface).

That reduces friction and helps ensure game-based modules are not optional add-ons but part of the main instructional flow.

Using national platforms to standardise content quality

Centralised development of game-based curricula through partnerships with companies like Savvy Games Group and national pedagogical institutes allows Saudi to:

- set minimum quality and safety standards for all game content used in schools;

- negotiate licensing and IP arrangements at national scale; and

- ensure that game-based tasks align with broader competency frameworks (e.g., computing, media literacy, entrepreneurship).

For investors looking at edtech, tools, or content providers, this centralisation implies that “one good national contract” might matter more than dozens of school-by-school pilots.

Linking school-level experiences to post-secondary and workforce programs

The reform will be most powerful if schooling is tied to:

- vocational tracks in game art, programming, and technical production;

- university programs in computer science, interactive media, and digital storytelling; and

- workforce programs that retrain adults into game-adjacent roles.

Saudi’s broader TVET and skills agenda including coding bootcamps, AI-skills initiatives, and regional digital academies offer multiple connection points. The Coursera data indicating a relatively high share of the labour force already active in online learning suggests the adult side of this pipeline is capable of responding.

Data-driven iteration

Because both Madrasati and the prospective gaming modules are digital, the system can track:

- engagement (time on task, completion rates);

- performance on problem-solving and design rubrics; and

- longer-term correlations between game-based coursework and later STEM, creative, or entrepreneurship outcomes.

This creates an evidence base that can guide refinement down to the level of which engines, assignment types, or collaboration structures actually move the needle on learning and employability.

Benefits and Market Implications for Investors

If implemented well, the gaming-curriculum reform changes several aspects of Saudi’s medium-term human-capital and sector landscape.

1. Deepening the local talent pool for gaming and interactive media

Rather than relying solely on imported talent or post-secondary conversion programs, studios and platforms operating in Saudi can expect a cohort of students who have:

- touched game engines and scripting languages early;

- worked in teams on creative projects with deadlines; and

- developed familiarity with feedback loops and iterative design.

This reduces onboarding time and opens the door for more junior roles to be filled locally, particularly in areas such as QA, live operations, community management, localisation, and technical art.

2. Strengthening the broader digital and AI workforce

Skills built through game-based curricula such as simulation thinking, optimisation, and human-machine interface design translate into AI, robotics, and digital-twin work. The same students who learn to optimize game mechanics may later work on logistics simulations, industrial-process visualisations, or health-care training environments.

Given Saudi’s aggressive investment in AI, cloud, and data-centre infrastructure, a workforce comfortable with interactive systems is a strategic complement.

3. Expanding investable themes in edtech and tools

The reform creates direct demand for:

- education-safe game engines and content-creation tools;

- assessment platforms capable of capturing project-based and soft-skills outcomes;

- cloud-rendering, asset-management, and collaboration tools adapted for school settings; and

- teacher-training solutions focused on game-based pedagogy.

For investors in Saudi and the wider GCC, this opens a spectrum of opportunities from seed-stage edtech to infrastructure-level platforms that can be exported to other education systems watching the Saudi experiment.

4. Supporting the domestic creator economy

Finally, normalising game creation and digital-content production in schools lowers the barrier for students to participate in the wider creator economy whether as streamers, indie developers, or freelance 3D artists.

Here, governance becomes critical: ensuring that young creators operate in safe, rights-respecting environments, and that monetisation pathways do not undermine educational priorities. But with the right safeguards, the reform can turn “time spent gaming” into a pipeline of creators, not just consumers.

Recap: From “Play” to Human-Capital Infrastructure

Saudi’s decision to integrate video games into the national curriculum is not a cultural novelty. It is a policy choice that:

- recognises the games industry as a major global economic sector;

- leverages an already-scaled digital-education platform;

- ties classroom activities to a national strategy around gaming, esports, and the creator economy; and

- positions Saudi’s workforce for jobs that blend technical, creative, and analytical capabilities.

The move will be judged not by headlines but by execution: the quality of curriculum materials, the depth of teacher training, the fairness of access to labs and hardware, and the maturity of assessment and safety frameworks.

For investors with a Saudi lens, the key is to treat this as part of the country’s broader digital-economy and human-capital infrastructure build-out. Gaming in the classroom is, ultimately, a signal: that the education system is being rewired to produce the kinds of skills that digital and AI-driven industries and the creator economy sitting alongside them will require over the next decade.