The Largest Demand Catalyst in the Region's Healthcare History

There is a number that every institutional investor with exposure to the Gulf healthcare sector should have committed to memory: 23 million. That is the approximate number of people in Saudi Arabia who are currently not covered by formal health insurance and who, under the Kingdom's National Health Insurance (NHI) program, are targeted for coverage by 2026. To put this in comparative context, 23 million new insured lives entering a single healthcare market within a defined legislative timeframe represents a demand shock of a character that analysts at any major global healthcare fund would recognize immediately as a structural inflection the type of event that reshapes provider economics, insurer positioning, and sub-sector investment priorities for at least a decade. And yet, unlike comparable coverage expansion events in Thailand (2002), Colombia (1993), or Indonesia (2014), the Saudi NHI transition has received comparatively limited systematic attention from the institutional investment community.

The architecture of the transition makes understanding it both urgent and structurally complex. Saudi Arabia currently provides its citizens with free access to public healthcare through the Ministry of Health's network. This means that the NHI program does not address a population with zero access to healthcare it addresses a population whose access is being fundamentally restructured from a direct-provision government model to an insurance-intermediated model, with the Center for National Health Insurance (CNHI) established as the Kingdom's single national payer. The MOH is simultaneously being repositioned, under Vision 2030's Health Sector Transformation Program, from its historic dual role as regulator and direct provider into a pure regulatory function. In practice, this means that demand is not simply being created ex nihilo it is being redirected. Citizens who previously accessed government hospitals directly will increasingly access both public and private facilities through an insurance authorization and claims infrastructure. That redirection is what creates the investable opportunity: a sudden, mandatory, and governmentally backstopped shift in the channel through which 23 million people receive and pay for healthcare.

Saudi Arabia's total public and private healthcare expenditure is estimated at SAR 250 billion in 2025, representing approximately 6% of national GDP, according to PwC's Strategy& analysis published in July 2025. The formal health insurance market currently covering approximately 37% of the total population through a combination of mandatory employer-provided private insurance for expatriate workers and private-sector Saudi employees was valued at USD 10.03 billion in 2025, growing at a projected CAGR of 6.52% to reach USD 13.74 billion by 2030 according to Mordor Intelligence's 2025 sector analysis. These figures, substantial as they are, do not yet reflect the full demographic and regulatory expansion of NHI. The 23 million uninsured Saudis represent incremental demand that these market size figures substantially understate. What the NHI program triggers and what the private healthcare sector, its investors, and the insurance industry must prepare to absorb is a stepwise expansion of the insured pool at a speed that the organic market could not produce in anything less than a generation.

Global Context: Universal Health Coverage as the World's Most Bankable Healthcare Policy Trend

The trajectory of countries that have implemented universal health coverage is, by any reasonable reading of the global evidence base, one of the most reliable demand amplification mechanisms in emerging and transition market healthcare investing. The mechanism is consistent: when formal insurance coverage expands rapidly through legislative mandate, utilization rates in covered populations surge as previously unmet need is actualized, provider capacity faces acute demand pressure, healthcare investment accelerates into gap-filling sub-sectors, and the reimbursement infrastructure that connects insurers to providers becomes an enabling technology platform whose operators generate durable, recurring, and often monopolistic income streams.

Thailand's Universal Coverage Scheme, introduced in 2002, tripled outpatient utilization in underserved populations within four years of implementation. Indonesia's Jaminan Kesehatan Nasional (JKN), phased in from 2014 and covering over 250 million people by 2019, drove a documented surge in hospital bed demand, accelerating private hospital investment from domestic and international groups including Siloam and Mitra Keluarga. In each case, the investment thesis was not that the universal coverage policy was risk-free it never is but that the direction and magnitude of the demand shift was sufficiently structural and governmentally committed that first-mover capital would be positioned favorably against late entrants who waited for all regulatory ambiguity to resolve.

Saudi Arabia's NHI transition shares these structural characteristics, but has several features that make it more institutionally investable than comparable transitions in lower-income settings. The Kingdom's fiscal capacity is extraordinary; a 2023 national budget allocated SAR 174.9 billion (approximately USD 46.6 billion) to healthcare and social development, with total Vision 2030 healthcare infrastructure investment targeted at over USD 65 billion. The sovereign balance sheet available to backstop the CNHI's single-payer obligations is not comparable to Indonesia's or Thailand's at the point of their UHC transitions. The transition is occurring in a market already habituated to formal private insurance for expatriates and private-sector Saudis since 2005 and 2016 respectively meaning that provider billing systems, clinical documentation standards, and insurer-provider contracting practices exist as institutional infrastructure onto which the NHI expansion can be layered. The coverage gap in Saudi Arabia is therefore not an absence of a system, it is a gap in the population enrolled in an already-functioning system, which is a fundamentally different and more rapidly bridgeable challenge.

Regional Landscape: The GCC Healthcare Insurance Ecosystem and Saudi Arabia's Pivotal Position

The GCC as a bloc spends more on healthcare per capita than any other emerging market region in the world, and the insurance architecture through which that spending is channeled differs significantly by member state. The UAE has the most mature mandatory private health insurance framework, with Abu Dhabi's Daman and Dubai's Dubai Health Authority each operating distinct mandatory schemes that have been in place since 2006 and 2013 respectively. Qatar has its Supreme Committee-linked health coverage for its large expatriate workforce. Kuwait and Bahrain operate predominantly government-funded systems with limited private insurance penetration. Saudi Arabia, the GCC's largest economy and most populous member, operates a hybrid model that is in the process of the most significant structural reconfiguration in the region's healthcare insurance history.

The broader MENA healthcare sector is experiencing its most intensive capital formation period in recent memory. Global healthcare investment attention to the region has intensified, driven by Vision 2030's USD 65 billion healthcare commitment, the UAE's post-pandemic health infrastructure expansion, and the emerging realization that MENA's disease burden profile characterized by very high rates of non-communicable diseases (NCDs), particularly diabetes, cardiovascular disease, and obesity creates persistent, high-acuity demand for both primary and secondary care that is structurally unlike the acute-episodic demand profiles of younger, healthier emerging market populations elsewhere. Non-communicable diseases now account for over 70% of all deaths in Saudi Arabia, according to Strategy&'s 2025 analysis, and 71.8% of Saudi adults are classified as overweight or obese. This chronic disease burden is not a future risk it is a present clinical reality that the NHI program will bring into the formal reimbursed care system at scale, with direct implications for hospital utilization, pharmaceutical consumption, diagnostic frequency, and disease management platform demand.

Saudi Arabia: The NHI Architecture and the Scale of the Coverage Transition

To understand the investment implications of the NHI program, it is necessary to first understand what is being built and how the stakeholder architecture is being reorganized. The Center for National Health Insurance, established as a subordinate body under the Council of Health Insurance framework, is designed to function as the single national payer for the Kingdom's citizen population. The program is entirely state-funded; there is no premium requirement for Saudi citizens, no annual renewal, and no benefit ceiling as originally structured. The CNHI is distinct from the Council of Cooperative Health Insurance (CHI, which regulates the mandatory private insurance market for private-sector workers) and from SAMA's historical oversight of insurance companies a separation of regulatory lanes that was formalized in March 2024 when the unified Insurance Authority (IA) became the independent regulator for the insurance sector across the Kingdom.

The operational backbone of the NHI's claims and data infrastructure is the National Platform for Health and Insurance Exchange Services (NPHIES), which has already eliminated the 30–60 day reimbursement cycle that historically characterized Saudi healthcare billing, replacing it with real-time payment authorizations and standardized electronic claims processing across both public and private providers. NPHIES is not merely a billing system, it is the data infrastructure that enables risk-adjusted capitation (RAC) payments, which the CNHI is introducing as the primary reimbursement mechanism for healthcare clusters. Under RAC, providers receive fixed per-capita payments adjusted for patient risk profiles rather than fee-for-service payments tied to the volume of procedures delivered. This is a fundamental reorientation of financial incentives: where fee-for-service rewards throughput, RAC rewards outcome quality and cost efficiency, creating direct financial incentives for preventive care, early intervention, and chronic disease management precisely in the areas where Saudi Arabia faces its most acute disease burden.

The strategic logic of this reimbursement transition is compelling in policy terms, and its investor implications are significant. PwC Strategy& estimates that improved national health outcomes enabled by RAC could generate annual savings of SAR 40 to 65 billion by 2035, equivalent to 10–15% of total healthcare spending. Within that total, preventive care investment is projected to save SAR 16–26 billion annually, and the reduction of unnecessary medical interventions given that Saudi hospital admission rates of 113 per 1,000 population sit above global averages could generate a further SAR 18–30 billion in annual efficiency gains. For private providers, this framework creates both a risk and an opportunity: those with the clinical data infrastructure, the chronic disease management capabilities, and the operational efficiency to thrive under value-based contracting will capture disproportionate volumes from the CNHI's expanding insured pool. Those whose business models depend on volume-driven fee-for-service billing will face structural margin compression.

The coverage gap that the NHI is designed to close is substantial and its population is well-defined. While GASTAT's 2024 healthcare statistics confirm that 100% of Saudi citizens have access to basic healthcare through the public system, formal insurance enrollment which is the basis on which private providers are reimbursed and on which the modern healthcare financing system operates covers approximately 37% of the total population today. The CHI's mandatory private insurance framework has enrolled approximately 13 million beneficiaries in the cooperative health insurance system, drawn from the private-sector workforce and their dependents. The NHI program extends formal insurance status to the remaining Saudi citizen population estimated at 22–23 million people who currently access care through direct public provision. The transition of this population into an insurance-intermediated system, even where the payer remains sovereign, fundamentally changes the data, documentation, and billing requirements for every public and private provider serving that population, and creates a reimbursement flow through NPHIES that is measurable, trackable, and auditable in ways that direct-provision government healthcare never was.

Sub-Sector Analysis: Where the Demand Surge Lands

The NHI's demand implications are not uniformly distributed across the healthcare sector. They concentrate in specific sub-sectors in ways that institutional investors must map with precision, because the investment case for each sub-sector rests on a different causal mechanism.

Hospitals and inpatient facilities are the most direct and immediately visible beneficiary of the NHI expansion, but the nature of that benefit is more nuanced than raw bed demand. Saudi Arabia currently faces a documented hospital infrastructure deficit: the Kingdom has fewer than 2.85 hospital beds per 1,000 people, below the G20 emerging economy average, and requires an estimated 27,000 additional beds by 2030 to meet demand from a population projected to reach 45 million according to current growth trajectories. The US International Trade Administration's Saudi Arabia healthcare market guide confirms that $12.8 billion in private sector investment has been identified for the next five years across PPP healthcare projects, with 19 currently underway totaling $2.9 billion in committed capital. The November 2024 Almoosa Health Company IPO filing on the Saudi Exchange signals the appetite of private hospital operators to access public capital markets at this stage of the sector's development. Dallah Healthcare's August 2024 acquisition of Al-Salam and Al-Ahsa Medical Services demonstrates the consolidation dynamic underway as larger operators scale ahead of the NHI demand wave.

The NHI transition will, however, intensify differentiation between hospital operators who can compete effectively in a value-based contracting environment and those who cannot. Hospitals with mature clinical information systems, strong chronic disease management programs, and CBAHI accreditation the Saudi equivalent of JCI accreditation will be positioned to negotiate favorable RAC contracts with the CNHI, capturing insured patient volumes at sustainable margins. Hospitals without these capabilities will face reimbursement pressure in a market that is progressively moving away from the fee-for-service model they were built to serve. This creates a bifurcation in the hospital investment thesis that mirrors what occurred in the US managed care transition of the 1990s and the UK NHS trust market in the 2000s: institutional quality operators with scalable operating platforms outperform, while sub-scale or technology-light operators face structural stress.

The diagnostics and laboratory sector is positioned to be a disproportionate beneficiary of NHI expansion, and it is perhaps the sub-sector most systematically under-analyzed in the Saudi healthcare investment conversation. The shift toward preventive care, early intervention, and chronic disease management that RAC payment reform incentivizes is, at its operational base, a diagnostic-intensive model of healthcare delivery. Managing a diabetic patient proactively requires HbA1c monitoring, lipid panels, renal function tests, and ophthalmology screenings a recurring diagnostic workload that generates predictable, contractable laboratory revenue streams. Vision 2030 has explicitly identified laboratories as one of nine priority areas for PPP development, alongside primary care, hospitals, radiology, pharmacies, rehabilitation, long-term care, and home care. The MOH's Health Sector Transformation Program's shift toward health clusters structured as integrated care networks serves as a demand aggregator for centralized laboratory services, a model that has been proven commercially viable in comparable cluster-based health systems in the UK and Germany.

Pharmacy represents the third major beneficiary sub-sector, but with a structural complexity that makes it more analytically demanding. The current formulary and reimbursement architecture of the Saudi mandatory insurance market constrains pharmaceutical utilization in ways that the NHI's expansion of covered lives will not automatically resolve the benefit design of the CNHI's coverage, including which medications are included in the formulary and at what reimbursement rates, will be a key determinant of pharmaceutical sector upside. What is already visible, however, is the acceleration of Saudi Arabia's domestic pharmaceutical manufacturing ambitions: the Kingdom is actively pursuing local production capacity as part of its broader supply chain resilience agenda, and the NHI's guaranteed demand base provides exactly the volume certainty that makes domestic manufacturing investment economically viable. The Vision 2030 target of increasing local pharmaceutical production to 40% of domestic demand by 2030 represents a supply-side transformation opportunity that is directly enabled by the demand-side certainty of NHI.

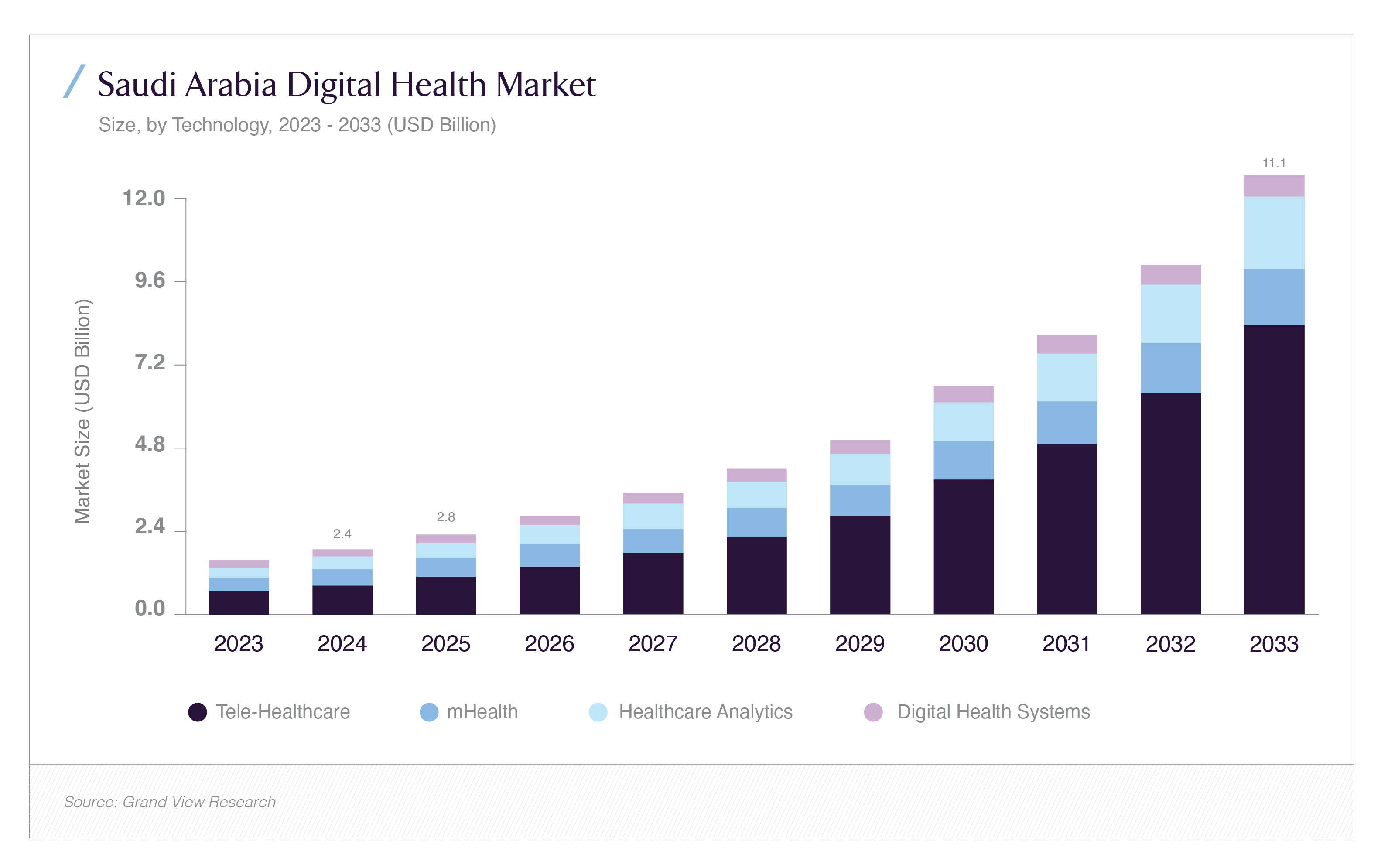

Digital health is the sub-sector where the NHI's structural transformation meets the most explosive independent growth trajectory. The Saudi Arabia digital health market was estimated at USD 2.37 billion in 2024 and is projected to reach USD 11.07 billion by 2033, growing at an 18.79% CAGR the fastest of any major healthcare sub-sector in the Kingdom according to Grand View Research's 2025 analysis. The tele-healthcare segment alone accounts for 44.98% of current digital health market revenue. The NHI's NPHIES infrastructure is, at its core, a digital health data platform, and the CNHI's ability to implement RAC payments at population scale depends entirely on the quality and completeness of electronic health records, AI-powered risk stratification tools, and real-time claims analytics across all covered providers. This dependency creates a direct procurement pipeline for digital health technology companies whose products are aligned with NPHIES integration standards and CNHI's data requirements.

Seha Virtual Hospital, launched in 2022 and now recognized as the world's largest virtual hospital, connects over 224 hospitals and delivers more than 30,000 consultations per month through AI-enabled diagnostics and remote specialist access. By 2030, Seha is targeted to expand to 500,000 consultations annually. The June 2025 new Council of Health Insurance mental health coverage mandates which now require all insurance policies to include psychological therapy and counseling services, expanding access for 4.2 million covered lives created an immediate and specific demand for telemental health platforms whose cost structures allow scalable delivery at NHI-relevant price points. This is precisely the type of policy-driven demand creation event that identifies venture and growth-stage healthcare technology companies whose timing aligns with the regulatory calendar.

The Risk-Sharing Models Being Negotiated Now

The shift from fee-for-service to value-based care under the NHI framework is being operationalized through a series of risk-sharing contractual models that insurers, providers, and the CNHI are actively negotiating, and understanding these models is essential for any investor building a position in Saudi healthcare because the financial structure of these contracts determines which operators generate durable margins and which face earnings volatility under the new reimbursement architecture.

Risk-Adjusted Capitation is the primary model the CNHI is introducing for healthcare cluster reimbursement. Under RAC, a cluster receives a fixed payment per enrolled member per year, adjusted for the health risk profile of its covered population. A cluster serving a population with high diabetes prevalence receives a higher capitation rate than one serving a healthier cohort but it must manage all the care needs of that population within the capitation envelope. The incentive structure this creates is the mirror image of fee-for-service: the cluster is financially rewarded for keeping its population healthy and out of hospital, because every avoided admission is a cost saving that improves its operating margin. For investors in healthcare cluster operators, primary care networks, and integrated care management companies, RAC creates attractive, predictable, inflation-linked income streams essentially, healthcare operators become annuity-like businesses with per-member-per-month revenue that grows with population size and risk-acuity. The downside risk is that operators who cannot manage their clinical cost base efficiently within the capitation envelope will face losses, creating a performance bifurcation in the operator market.

The private insurance market, running alongside the NHI's citizen coverage system, is simultaneously evolving its own risk-sharing structures. Bupa Arabia's 2025 launch of a no-pre-approval insurance model, the first of its kind in the Kingdom, enabling members to receive treatment at seven partner hospitals without prior authorization represents a significant operational innovation that reduces friction in the member-provider-insurer triangle. Its commercial logic is a form of risk-sharing: by removing pre-authorization requirements, Bupa Arabia accepts the utilization risk in exchange for the member retention and provider relationship benefits of a frictionless care experience. Tawuniya's AI-driven health analytics program, which reportedly reduced chronic disease costs by 28% across 1.5 million covered lives through personalized wellness plans and early intervention, demonstrates how the leading insurers are already deploying predictive analytics as a cost-containment and risk-management tool that functions as a proprietary competitive advantage in the value-based care era.

The June 2025 mental health coverage mandate from the CHI which requires all policies to include psychological therapy and counseling services is the most recent example of a regulatory intervention that creates immediate new risk for insurers (higher claims exposure) and immediate new opportunity for providers (a reimbursable service category that previously had no insurance funding). This dynamic will repeat across other previously uncovered or under-covered service categories as the NHI's benefit package is refined and the CHI continues to expand mandatory coverage requirements. Value-based insurance design, which aligns coverage generosity with clinical evidence of effectiveness, is the long-term direction of Saudi insurance benefit design and the companies that understand how to underwrite, price, and manage these expanded benefit packages at actuarially sound rates will capture disproportionate market share.

The Gaps That Define the Risk-Return Profile

For an institutional investor constructing a position in Saudi healthcare in anticipation of the NHI transition, the opportunity is compelling but the gap map is specific and must be addressed analytically rather than assumed away. The first and most operationally significant gap is workforce. Saudi Arabia currently employs approximately 26.6 physicians per 10,000 people and 59 nurses per 10,000 well below the OECD average of 116 nurses per 10,000 and the broader benchmark for a healthcare system managing the NHI's anticipated utilization surge. The MOH has set targets of graduating more than 10,000 new Saudi nurses and doctors annually by 2030, but workforce development timelines do not compress easily regardless of funding, and an NHI-driven utilization surge against a constrained clinical workforce creates both quality-of-care risk for the population and pricing power for healthcare operators who can secure and retain clinical staff. Investment in healthcare education infrastructure, nursing colleges, medical simulation centers, clinical training partnerships is a structurally necessary antecedent to the NHI's full operationalization that has not yet attracted the institutional capital attention commensurate with its strategic importance.

The second gap is the data infrastructure layer beneath NPHIES. While NPHIES has operationalized real-time claims processing, the broader electronic health record ecosystem across both public and private Saudi providers remains incomplete. As of early 2025, more than 50% of patient records have been digitized under the unified Nafis e-health platform which means that nearly half have not. For CNHI's RAC payment model to function accurately, the risk stratification algorithms that determine per-member capitation rates must be fed by complete, structured clinical data. Gaps in that data lead to miscalibrated capitation rates, creating systematic under-reimbursement for providers serving high-acuity populations and over-reimbursement for those serving healthier cohorts, a problem that compounds over time and creates adversarial dynamics between payer and provider. Investment in health information system implementation, interoperability infrastructure, and clinical documentation training is therefore not merely a digital health investment thesis; it is a foundational condition for the NHI's actuarial integrity.

The third gap is regulatory sequencing. The NHI program's 2026 target date for full citizen coverage is ambitious relative to the complexity of operationalizing a new single-payer system across a geographically large and service-fragmented healthcare market. The Insurance Authority became the unified independent regulator only in March 2024 a regulatory reform that is still being bedded down. The CNHI's RAC implementation is being introduced through phased pilots, as Strategy& recommends, beginning with shadow billing and controlled cluster rollouts. Investors should expect implementation delays relative to headline timelines, plan for a 2027–2028 effective full operationalization horizon, and size their positions accordingly. The delay is not an invalidation of the thesis, it is a calibration of the timing.

The Investment Architecture: Sizing and Entry Points

Translating the NHI thesis into investable positions requires a clear framework for sub-sector sizing and entry point logic. In the hospital sector, the PPP model is the primary vehicle: the MOH has identified $12.8 billion in PPP project investment across hospitals, primary care, laboratories, radiology, and pharmacies over five years, with 19 projects currently in execution. International investors can access these through consortium structures with Saudi development companies, through IPO participation in listed hospital operators (Dallah, Dr. Sulaiman Al Habib, Almoosa), or through private credit to hospital developers building the bed capacity that the NHI demand will fill. In the insurance sector, the concentration of the market Bupa Arabia and Tawuniya controlling 70% of written premium creates both a consolidation play for the existing leaders and a niche opportunity for specialized insurers developing products for the NHI's adjacent market segments (premium supplemental coverage, international private medical insurance for expatriates, and SME group plans, which Mordor Intelligence identifies as the highest-growth segment at 18.62% CAGR). In digital health, the investable universe ranges from growth-stage venture capital in NPHIES-integrated digital health startups Redesign Health and Sanabil Investments launched a healthcare venture studio in January 2025 targeting 20 new startups to PIPE investments in listed health technology companies as the Saudi Exchange deepens.

Conclusion: The Countdown Clock as an Investment Signal

Saudi Arabia's National Health Insurance program is not a policy aspiration in a planning document. It has a named institutional owner (the CNHI), a functional digital infrastructure (NPHIES), a defined reimbursement reform (RAC), a legislative timeline (2026 citizen coverage target), and a fiscal sponsor with one of the world's strongest sovereign balance sheets. The demand it will generate 23 million newly insured lives entering a formal healthcare financing system is not speculative. It is structural, mandated, and demographically locked-in by a population whose chronic disease burden guarantees sustained utilization at every point of the care continuum.

The investment window before full operationalization is the optimal entry point. Sub-sector leaders integrated hospital operators with CBAHI accreditation, RAC-ready clinical systems, and geographic presence in Riyadh, Jeddah, and the Eastern Province; diagnostic and laboratory networks positioned within or adjacent to MOH health clusters; NPHIES-integrated digital health platforms with credible deployment at scale; and specialized insurance operators targeting the SME, telehealth add-on, and mental health coverage mandates are building the positioning now that will determine their market share in the post-NHI healthcare economy.

Saudi healthcare is not emerging. It has emerged. What is arriving next is its institutionalization the translation of a large, government-directed, informally organized healthcare market into a data-rich, insurance-intermediated, value-based care economy that resembles the mature healthcare systems of Germany, South Korea, and Australia rather than the fragmented provider markets of earlier-stage emerging economies. The investors who recognize this transition for what it is, and who position accordingly in the remaining runway before 2026, are accessing one of the region's most consequential structural investment opportunities of this decade.