Saudi Arabia’s life-sciences market is no longer a “volume plus subsidies” story. It is becoming a tightly supervised, data-rich, price-controlled ecosystem in which regulatory governance is itself a strategic asset.

Two developments crystallise that shift:

- A new SFDA Law in 2025 that formally establishes the Saudi Food and Drug Authority as an independent regulator with financial and administrative autonomy, reporting directly to the President of the Council of Ministers.

- A targeted amendment to the SFDA Law and board composition, highlighted in early-2026 legal commentary, which tightens how the Authority is overseen and how decisions are escalated.

For investors in pharmaceuticals, biotechs, medical devices and health-adjacent consumer products, this is not a narrow legal tweak. It is a signal that the Kingdom wants FDA-style governance density while simultaneously localising manufacturing and deepening clinical research.

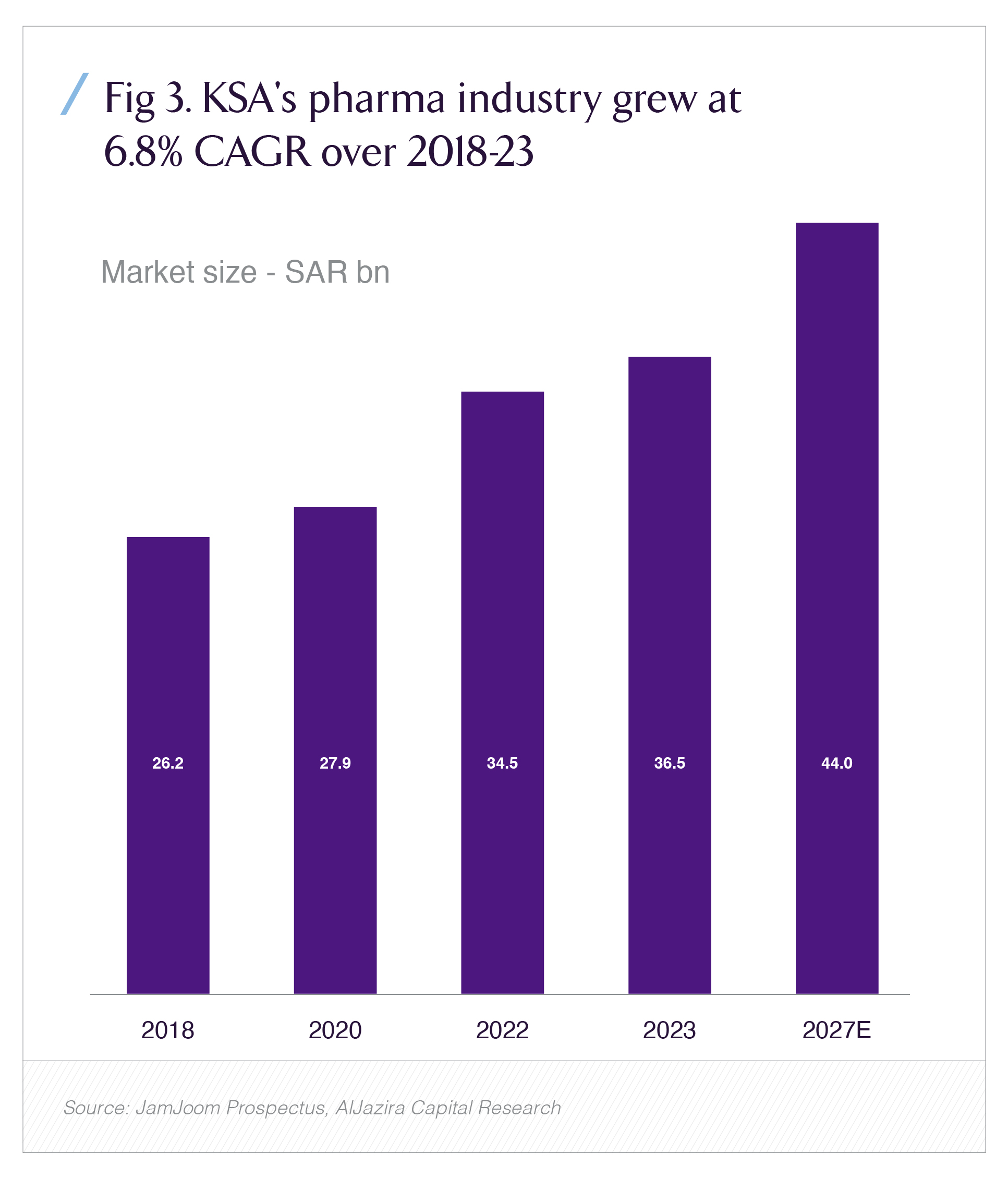

The opportunity set is large enough to matter. KSA’s pharma market reached roughly SAR 36.5 billion by 2023 and has grown at around 6.8% CAGR since 2018, with projections out to 2027 based on IQVIA data and local research. That growth is anchored in chronic-disease prevalence, population aging and Vision 2030 health-system investment sectors where SFDA is the gatekeeper.

This article unpacks what the new governance architecture means in practice: the global context, Saudi’s specific regulatory trajectory, the friction points that remain, and how institutional investors should read the signal.

Global context: Regulators as system architects, not just gatekeepers

Globally, the last decade has pushed health regulators into a more strategic role:

- Biologics, gene therapies, cell-based products and complex combination devices need deeper specialist review and post-market surveillance.

- AI and software-as-a-medical-device have blurred the line between code release and clinical intervention.

- Supply-chain fragility (COVID-19, geopolitics, API concentration) forces regulators to worry about resilience and localisation, not just safety.

Major regulators have responded by upgrading governance rather than just adding headcount. Examples include:

- The US FDA created a dedicated Office of Digital Transformation and establishing cross-centre governance around data, analytics and IT modernisation.

- The EMA strengthens cross-committee coordination for advanced therapies, with more explicit risk-benefit governance for small-population indications.

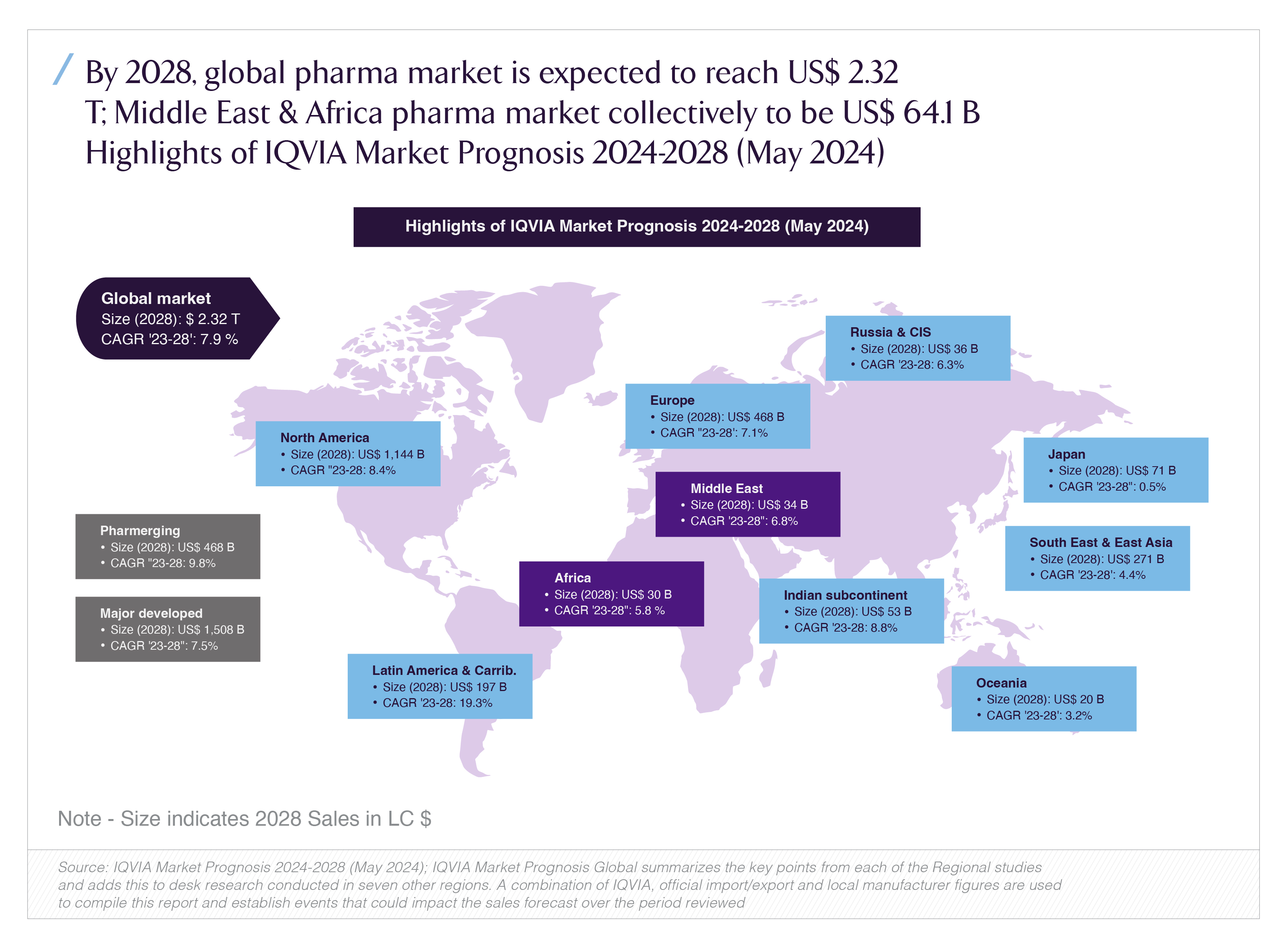

At a macro level, the industry these regulators supervise is still expanding. IQVIA’s 2024 Market Prognosis expects the global pharmaceuticals market to reach roughly USD 2.3 trillion by 2028, with the Middle East and Africa together around USD 64 billion, growing at about 6.8% CAGR over 2023–2028.

The takeaway for investors: regulators are becoming portfolio managers of risk and innovation, not passive “yes/no” agencies. Governance structurewho sits on the board, who they report to, what they can delegatematters for time-to-market, pricing outcomes and predictability.

Regional landscape: GCC health regulators move up the value chain

Across the GCC, regulatory capacity is being upgraded as health spending rises and localisation targets tighten:

- Gulf markets have steadily raised their share of global pharma demand; IQVIA’s MEA data show double-digit growth in several regional markets and rising shares for local and regional manufacturers.

- Tender markets (NUPCO in KSA, unified procurement in Egypt) increasingly embed regulatory criteriaGMP compliance, pharmacovigilance performance, traceabilityinto commercial access.

In this environment, Saudi’s SFDA is already an outlier in terms of scope: it covers food, drugs, medical devices, cosmetics, water, pesticides and a range of health-related products under a unified umbrella. The new SFDA Law codified that breadth and gave the Authority clearer regulatory, executive and monitoring functions, with its own legal personality and budget.

GCC peers are moving in the same direction, but with different speeds and structures. For investors, that makes KSA both a reference market and a testbed: if an asset can navigate SFDA’s governance, it is better positioned for regional scaling.

Saudi landscape: A bigger mandate, a sharper board

1. The new SFDA Law (2025): regulatory independence and scope

The 2025 SFDA Law, as summarised by legal commentary, does three things that matter directly for capital allocation:

- Confers legal personality and autonomy

SFDA can contract, manage its own budget and operate independent laboratories and regional branches. This positions it as a true independent authority, not just an administrative arm of the Ministry of Health. - Codifies a wide mandate

Article-level detail spells out coverage of drugs, biologicals, devices, cosmetics, food, water and pesticides, plus responsibilities for standards, licensing, post-market surveillance and public awareness. - Clarifies regulatory, executive and monitoring roles

The Law separates policy-making, execution and oversight functions inside SFDA, which is a precondition for robust governance and risk management.

This legal upgrade is happening against a market backdrop of meaningful scale and growth. According to Aljazira Capital’s 2025 KSA pharma sector report, drawing on IQVIA data, the Saudi pharma market reached about SAR 36.5 billion in 2023, growing at roughly 6.8% CAGR over 2018–2023.

The same report highlights that pharma imports have accounted for close to 40% of total chemical-sector imports over 2015–2023, while locally produced drugs cover only about a third of total consumption, with targets to reach at least 40% domestic production by 2030.

That import dependency plus localisation ambition is exactly the kind of structural tension that a stronger regulator is built to manage.

2. Targeted board-composition changes (2025 amendment; 2026 commentary)

Alongside the new framework law, a 2025 amendment and subsequent commentary in early 2026 describe “targeted changes” to SFDA’s board composition rather than a wholesale restructuring.

Even without the full article text, the public summaries signal three important shifts:

- More explicit governance architecture: The amended law clarifies the board’s role as a high-level oversight body, with regulatory, strategic and financial stewardship functions tightly delineated from day-to-day operations.

- Stronger linkage to national priorities: Board membership is structured to align SFDA’s decision-making with broader Vision 2030 programs (health-sector transformation, industrial strategy, localisation and digital government).

- Potentially higher technical density: Law-firm commentary emphasises the inclusion of members with specialised expertise, implying a tilt toward more technical and sector-fluent governance rather than purely administrative representation.

For investors, the message is simple: board decisions are likely to become more systematic, more anchored in multi-year industrial policy, and less vulnerable to ad-hoc swings.

Regulatory performance: throughput and enforcement are already moving

Governance only matters if it shows up in throughput and enforcement.

Recent SFDA communications for Q1 2024 point in that direction: the Authority reported double-digit growth in the issuance of licenses for factories and pharma/cosmetics warehouses (around 16% growth), a 25% increase in product classifications, and strong growth in marketing and health-education approvals. Licensing timelines for some services have reportedly been reduced to about three working days, aided by updated frameworks and digital processes.

The combination of a more autonomous authority, a sharper board and improving operating metrics is the core of the “governance gets sharper” story: it is about capacity and discipline, not only about new rules.

Key challenges the new governance must still solve

Even with a stronger law and a more intentional board structure, several structural challenges remain for SFDA and for market participants:

- Complexity of product pipelines

Advanced therapies, biosimilars, combination products and software-based devices all require nuanced scientific review, risk-based post-market surveillance and sometimes adaptive licensing models. - Localisation versus dependency

Saudi Arabia still relies heavily on imported APIs and finished products. Oversight has to support localisation (through predictable standards, GMP enforcement and pricing clarity) without over-protecting local manufacturers or compromising quality. - Data integration and real-time insight

Track-and-trace (RSD), adverse-event databases, clinical-trial registries, customs data and tender outcomes still sit across multiple systems. Turning those into a single risk-monitoring picture is a governance challenge, not just an IT one. - Workforce and expertise depth

Governance changes can mandate specialised committees and risk frameworks, but SFDA still needs enough biostatisticians, pharmacovigilance experts, device engineers and data scientists to make the model work at scale.

These are precisely the areas where board-level oversight, committee structures and escalation rules matter. A more technical, strategy-aware board is better placed to direct investment towards the highest-risk bottlenecks.

How sharper SFDA governance changes the operating environment

For life-sciences and health-adjacent companies, the governance shift translates into a different operating logic along several dimensions.

1. From “document compliance” to risk-based supervision

The new Law’s separation of regulatory, executive and monitoring functions, combined with a more empowered board, makes risk-based supervision more credible.

- High-risk products and facilities can be subjected to more intensive pre-approval review, GMP inspections and post-market monitoring.

- Lower-risk products (certain OTCs, low-risk devices) can be channelled through streamlined pathways, provided traceability and labelling standards are met.

Over time, investors should expect capital-light, compliance-lite products to enjoy faster market access, while complex or higher-risk assets face a more structured but potentially more predictable regime.

2. Stronger link between regulatory decisions and industrial strategy

KSA’s pharma-sector strategy explicitly targets higher local production shares and more resilient supply chains.

Under sharper governance, SFDA’s pricing, tender eligibility and manufacturing requirements are more likely to be aligned with:

- Local-content targets (e.g., thresholds for tenders or reimbursement).

- Incentive structures for local R&D and clinical research, particularly in chronic-disease areas that dominate the domestic burden.

- Long-term commitments to GMP upgrades and technology transfer.

Investors in manufacturing, CDMOs and local partnerships should read this as a tilt toward “regulated localisation” rather than unstructured protectionism.

3. Enhanced transparency and accountability

A law that defines SFDA’s powers, duties and definitions in detail and a board structure that is publicly discussedreduce regulatory opacity.

For institutional capital, that typically means:

- Clearer expectations around documentation, timelines and escalation pathways.

- More stable jurisprudence on pricing, substitution and pharmacovigilance obligations.

- A regulatory environment that can support sophisticated risk-sharing contracts and value-based arrangements as the market matures.

Implications and opportunities for investors

For Saudi and international investors, the governance changes at SFDA open several strategic lanes.

1. Scaling compliant local manufacturing

As SFDA and other agencies push toward higher local-production shares, facilities that can demonstrate “over-compliance” on GMP, environmental and safety standards will be better positioned to secure:

- Long-term supply contracts via NUPCO and other tendering bodies.

- Preferential treatment in localization-linked incentives and industrial-land allocation.

- Stronger negotiating power in co-manufacturing and tech-transfer deals with multinationals.

The governance reforms make it more likely that such advantages are rooted in clear, published criteria, something institutional investors can underwrite.

2. Clinical-research and biotech platforms

SFDA has highlighted growth in clinical-research activity, particularly for biotech products, in recent communications.

A board that is more technically literate and more integrated with national science and innovation strategies can:

- Signal clear expectations for trial design, ethical standards and data requirements.

- Coordinate with SDAIA and other bodies on data governance, particularly for genomics and real-world data, where privacy and AI-use questions cross institutional boundaries.

That clarity reduces non-technical risk for investors backing CROs, SMOs and biotech platforms based in the Kingdom.

3. Health-adjacent consumer and food sectors

The SFDA Law’s scope explicitly includes food, water and many consumer products.

Stronger governance here affects:

- Nutritional-labelling and transparency requirements (with commercial implications for FMCG and food-service chains).

- Marketing and advertising approvals for health-linked products, where the Q1 2024 data show rapid growth in permitted campaigns but tighter oversight.

Investors in these segments should view SFDA less as a hurdle and more as a co-architect of product portfolios and brand-positioning strategies.

What sophisticated investors should do now

In practical terms, a sharper SFDA governance model should push investors to:

- Re-rate regulatory risk in models

Instead of blanket “KSA regulatory” discounts, differentiate based on product class, local-content strategy, and alignment with SFDA’s enforcement priorities. - Diligence governance fit as part of deal screening

When evaluating assets in KSA, ask: “How does this business model sit under the new SFDA Law and board priorities?” That includes pricing exposure, tender dependence, and post-market surveillance obligations. - Engage early on compliance operating models

Portfolio companies will increasingly need robust QMS, pharmacovigilance frameworks, data-governance policies and board-level compliance committees that can interact credibly with SFDA. - Monitor implementing regulations and board practice

The Law is a framework. The real texture will come from implementing regulations, circulars and how the board uses its agenda. Systematic monitoring is now a core part of the thesis, not a legal afterthought.

Recap: Governance as the new risk premium in Saudi life sciences

Saudi’s SFDA is moving from “powerful but opaque regulator” toward a codified, autonomous authority with a sharpened board and measurable performance gains. The 2025 Law and targeted board-composition changes are not cosmetic they are part of a larger effort to align regulatory oversight with Vision 2030’s industrial, health and localisation objectives.

Three messages stand out for investors:

- Regulatory risk is becoming more structured and more predictable. That supports larger, longer-duration capital commitments in manufacturing, clinical research and health-adjacent consumer sectors.

- Governance is now a competitive differentiator. Companies that align early with SFDA’s expectations on quality, traceability, pricing discipline and data will have an edge in tenders, approvals and reputational standing.

- Scale and complexity justify the effort. A multi-tens-of-billion-riyal pharma market, embedded in a fast-growing MEA region and backed by sovereign-level industrial policy, is increasingly governed at a level comparable to leading global regulators.

For Saudi and global investors alike, reading SFDA governance correctly and building portfolios that fit under that arc is now a central part of the life-sciences and healthcare thesis in the Kingdom.