In early November, Saudi Arabia’s Ministry of Health (MoH) and its flagship Seha Virtual Hospital (SVH) moved from “interesting case study” to system level reference point. At the 8th Zimam Digital Health Forum in Dubai, Seha Virtual Hospital and the Innovation Empowerment Center were named Digital Health Organization of the Year 2025, a regional award that explicitly recognizes strategy, scaled execution, and measurable outcomes in virtual care.

Within days, the MoH also announced a collaboration with procurement specialist Efficio to professionalize healthcare supply chains, improve procurement governance, and advance local content objectives across hospitals and clinics. In parallel, King Faisal Specialist Hospital and Research Centre (KFSHRC) deepened its cooperation with the National Unified Procurement Company (NUPCO) around digital supply chain platforms and medical logistics.

Taken together, these are not isolated press releases. They amount to a “November print” for Saudi digital health: an external validation of virtual care performance, plus concrete steps to harden the procurement and logistics backbone that keeps a digital first health system running under stress. For investors, the question is not whether Saudi digital health is growing that is already a given but how far the current trajectory is from a mature, outcomes priced infrastructure asset.

Global Digital Health and Telehealth: A Market Moving to Scale

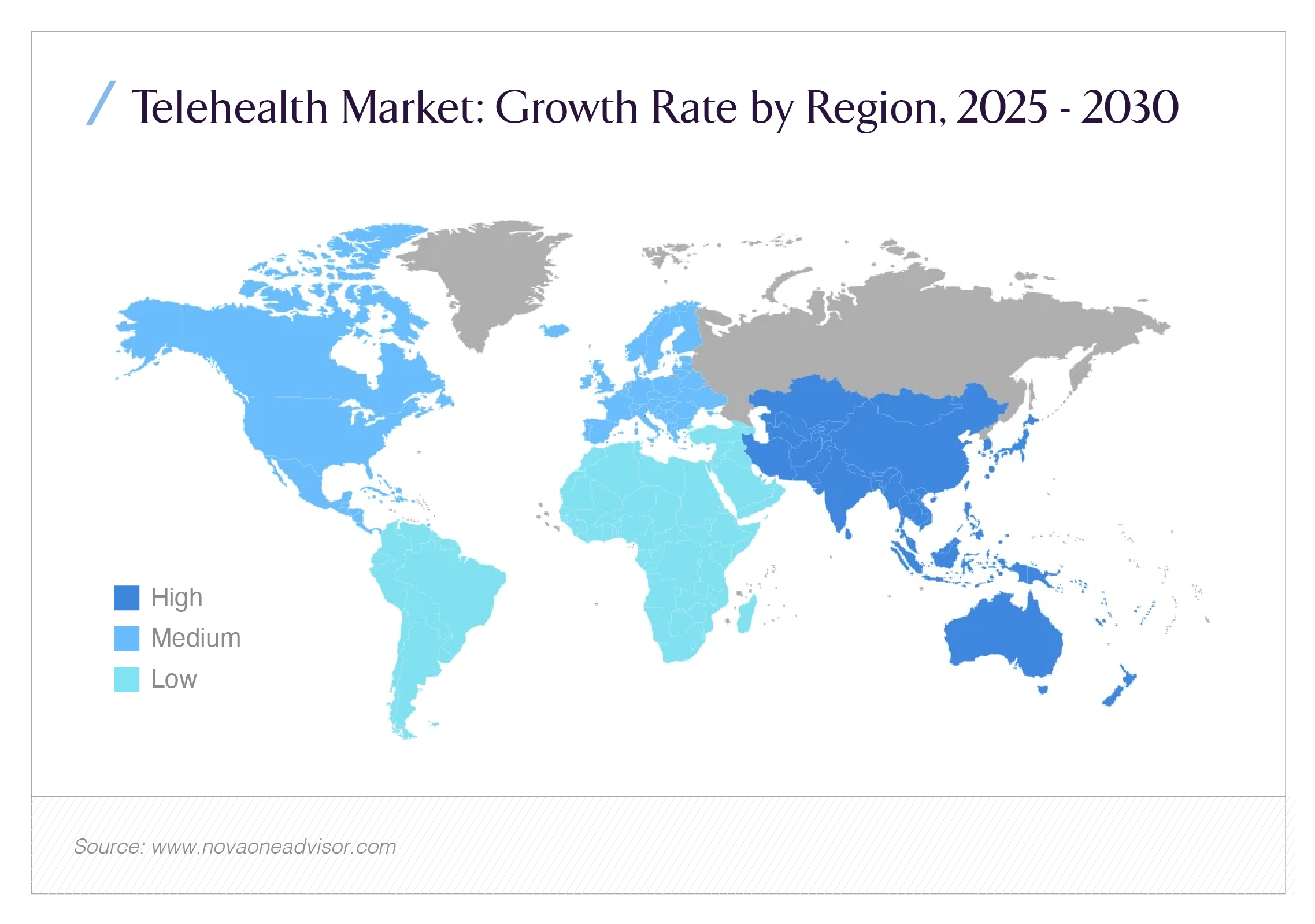

At the global level, telehealth and digital health have shifted decisively from pandemic emergency tools to core infrastructure. Market data now reflect that repositioning. Mordor Intelligence estimates the global telehealth market at about USD 134 billion in 2024, with projections of roughly USD 505 billion by 2030 implying a compound annual growth rate (CAGR) of ~23.5%.

This growth is far from uniform. A “growth rate by region” split shows Asia–Pacific and parts of the Middle East and Africa outpacing more mature North American and European markets, which are already wrestling with reimbursement ceilings and integration costs. For allocators, the implication is straightforward: benchmark returns increasingly depend on a portfolio that captures both the depth of developed markets and the velocity of high growth regions.

What matters for Saudi Arabia is not simply that global telehealth is growing, but that its own market sits on the steep part of that curve while being anchored by a sovereign transformation agenda. The Zimam award confirms that global peers now view Seha VH as a credible reference implementation within that broader transition.

Regional Positioning: GCC Digital Health as Critical Infrastructure

Across the GCC, digital health has become a pillar of national competitiveness rather than a convenience feature. Saudi Arabia and the UAE in particular are investing in virtual hospitals, AI enabled triage, and integrated electronic health records (EHRs) to manage chronic disease burdens and geographic dispersion.

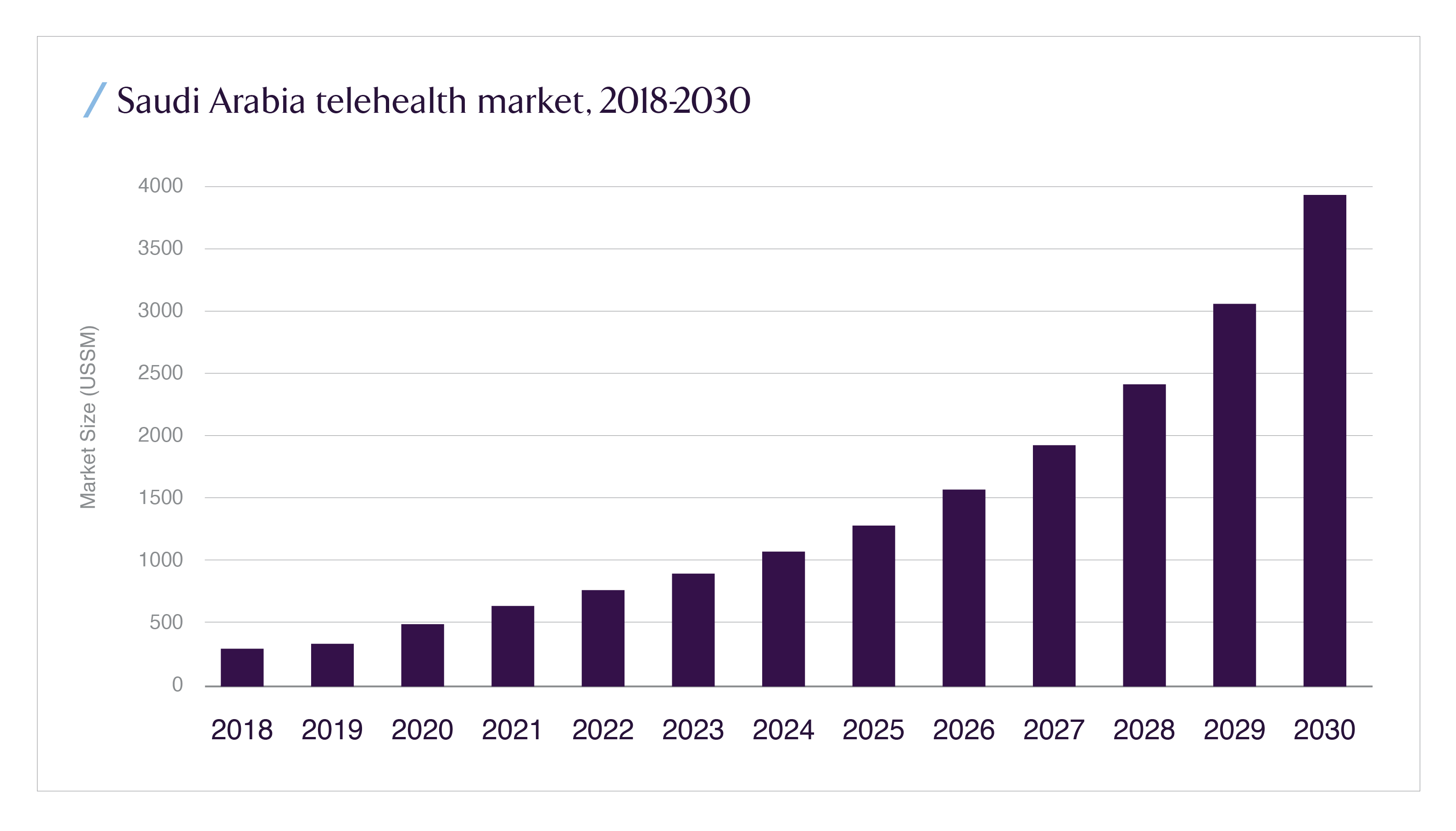

Saudi’s telehealth market illustrates this regional repositioning numerically. Grand View Research estimates Saudi telehealth revenue at about USD 1.06 billion in 2024, with a projected USD 3.92 billion by 2030 equivalent to a 25.1% CAGR from 2025 to 2030 and roughly 0.9% of global telehealth revenue in 2024. That share looks modest, but the growth rate is not; it puts Saudi firmly within the global high growth cohort for virtual care.

While each GCC state is building its own stack, a common pattern is emerging: virtual hospitals, AI assisted diagnostics, and remote patient monitoring (RPM) are being coupled to broader industrial policies, data centers, med tech manufacturing, and local content requirements. Saudi’s November announcements around digital health awards and procurement collaboration fit precisely into that pattern.

Saudi Digital Health Market: From Niche to Macro Relevant

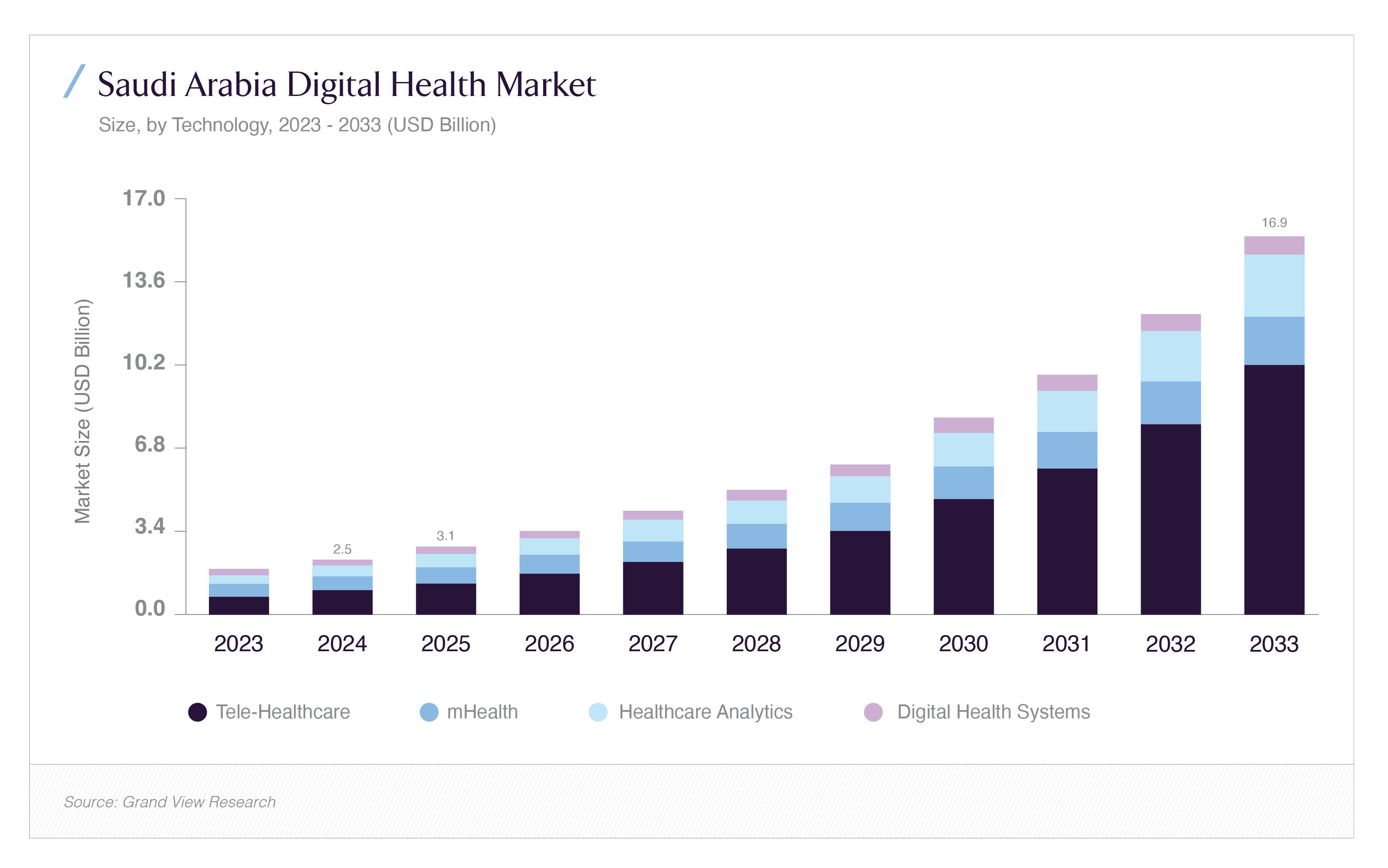

The most recent Saudi focused market work suggests a digital health sector that has outgrown the “pilot” label. A 2025 market intelligence report, drawing on Grand View Research data, estimates Saudi’s digital health market at roughly USD 2.5 billion in 2024, rising toward nearly USD 16.9 billion by 2033 implying ~23.8% CAGR. Other vendor estimates, using broader definitions that include additional mHealth and IT categories, place the 2024 market closer to USD 4.4 billion and the 2033 outcome around USD 15.3 billion.

The exact number matters less than the order of magnitude and slope: digital health is already a multi billion dollar market, with a path to mid teens billions over the next decade. Telehealth and RPM are consistently identified as the leading and fastest growing sub segments by revenue share.

For Saudi investors, three themes stand out:

- Digital health is compounding at a rate well above nominal GDP and general healthcare spending.

- Telehealth and RPM are not fringe add ons; they are where most of the incremental value is accruing.

- Government policy Vision 2030, the Health Sector Transformation Program, regulatory sandboxes is not just enabling this growth but actively steering it.

Within this trajectory, Seha Virtual Hospital is both a beneficiary and a driver.

Seha Virtual Hospital: From Flagship to System Integrator

Seha Virtual Hospital, launched in 2022, is now recognized as the world’s largest virtual hospital by the Guinness Book of Records. It connects more than 220 physical hospitals nationwide and delivers over 40 specialized services entirely online, from cardiology and critical care to neurology and psychiatry.

Public and semi official sources point to three types of impact:

- Access and reach. Seha VH supports hospitals across Saudi Arabia, allowing patients in remote regions to access sub-specialists without travel. Reports indicate coverage of 160–224 hospitals and capacity in the hundreds of thousands of patients annually.

Operational efficiency. Market intelligence work citing Seha VH case data reports up to a 40% reduction in average hospital length of stay and a 25% reduction in readmission rates for certain service lines.

- Patient experience. A 2024 population level study of telehealth in Saudi Arabia found virtual consultations achieving ~97% overall satisfaction versus ~84% for in person visits, driven by convenience and timeliness.

Seha VH’s Zimam award therefore does more than decorate a single institution. It effectively signals to the market that Saudi’s flagship virtual hospital:

- Meets regional benchmarks on governance, safety, and digital health strategy.

- Has demonstrable impact on core efficiency and quality metrics.

- Serves as an integration layer across an increasingly digital and data rich national health system.

For investors, this shifts Seha VH from an interesting policy story to a reference operator whose architecture and KPIs can be used to benchmark other digital health assets in the region.

Procurement, Supply Chain, and Local Content: The Hidden Backbone

Digital health is only as strong as its supply chain. AI enabled imaging, home monitoring devices, and virtual care platforms all rely on uninterrupted flows of hardware, consumables, and IT services. The MoH’s newly announced collaboration with Efficio is designed explicitly to tighten that backbone.

According to public statements, Efficio will work with the MoH to:

- Professionalize procurement processes across the value chain, from central tenders to hospital level purchasing.

- Embed digital tools and analytics into sourcing, category management, and performance monitoring.

- Align procurement practices with Saudi Arabia’s broader local content agenda, ensuring that more spend supports domestic manufacturing and service providers.

In parallel, the KFSHRC–NUPCO memorandum of understanding aims to streamline medical supply chains, co develop procurement related digital platforms, and enhance knowledge sharing around business development and IT. This is not a marginal initiative; NUPCO already plays a central role in pooling and digitizing public sector medical procurement, and deeper integration with a leading tertiary center like KFSHRC effectively extends that digital backbone into complex care.

The net effect is a convergence between two agendas:

- Digital front end: Seha VH and other virtual care platforms orchestrating patient journeys, triage, and remote consultations.

- Digitized back end: Centralized, analytics driven procurement and logistics infrastructure ensuring that the physical and IT assets required for digital care are available and cost effective.

Investors evaluating Saudi digital health now need to treat supply chain digitization as part of the thesis, not a footnote. Margin leakage, resilience under shock (pandemics, geopolitical events), and the ability to scale new pathways (such as home infusion or RPM) all depend on this backbone.

Challenges: From Integration to Outcomes Based Contracting

Despite the positive November print, Saudi digital health still faces a set of structural challenges that will determine whether the sector achieves its full potential as a capital efficient infrastructure asset:

1. Integration across regions and providers.

Seha VH knits together hundreds of hospitals, yet care pathways still run across multiple legacy IT systems, regional clusters, and semi autonomous providers. Full end to end interoperability clinical, administrative, and financial remains a work in progress.

2. Talent, workflows, and change management.

Digital health is not just software; it is a re-design of clinical workflows and roles. Saudi’s health system is managing simultaneous transitions: new payment models, increased private sector participation, and the introduction of AI assisted decision support. Training clinicians to work effectively in virtual and hybrid environments is a non-trivial transition cost.

3. Data governance, cybersecurity, and AI assurance.

As more data flows through virtual platforms, questions of consent, secondary use, and algorithmic bias become more acute. Saudi’s broader push on AI regulation and data localization provides a helpful macro framework, but operationalizing this at the level of each vendor contract and system integration remains complex.

4. Outcomes based contracting and investor signals.

While case studies highlight reductions in length of stay and readmissions, systematic outcomes based contracts where virtual care providers are paid explicitly for reduced admissions, improved control of chronic conditions, or avoided emergency department visits are still emerging. Without those structures, investors must infer value from high level market growth numbers rather than cash flow linked performance.

These constraints do not erase the opportunity, but they do shape the risk return profile. For Saudi investors, the key is to differentiate between exposure to generic “digital health growth” and exposure to assets that are contractually tied to measurable system wide outcomes.

Solutions: Architecting Digital Health as an Investable Infrastructure Layer

Solving these challenges requires alignment between policymakers, operators, and capital. The November announcements offer clues as to how that alignment is forming.

First, the Zimam award crystallizes a reference architecture for virtual hospitals: multi hospital integration, specialty coverage, clear KPIs around access, quality, and efficiency, and governance structures that satisfy external evaluators. This gives investors a benchmark for what “good” looks like when assessing other virtual care platforms, both inside and outside the Kingdom.

Second, the Efficio and NUPCO initiatives indicate a move toward professionalized, analytics driven procurement with explicit local content objectives. For digital health, this opens several levers:

- Standardized frameworks for procuring telehealth platforms, RPM devices, and AI solutions, with clear requirements around interoperability and cybersecurity.

- Lifecycle cost modeling that internalizes not just capital expenditure on hardware and software, but also training, maintenance, and data governance overhead.

- Local manufacturing and assembly of medical devices and IT hardware, reducing FX exposure and supply chain risk while supporting Saudi’s broader industrial strategy.

Third, global market data can be used to structure more sophisticated contracts. The global telehealth market’s regional growth differentials and Saudi’s 0.9% share with a 25.1% CAGR provide a quantitative backdrop for negotiating risk sharing arrangements with vendors and operators.

In practice, this might translate into:

- Virtual care PPPs where investor returns are tied to regional penetration targets and reductions in specific high cost events (e.g., avoidable admissions for diabetes and cardiovascular disease).

- Outcome linked fee schedules for AI enabled diagnostics, with payment contingent on documented improvements in time to diagnosis or reduction in unnecessary imaging.

- Structured funds or co-investment vehicles that aggregate digital health assets platforms, device portfolios, and data infrastructure under governance frameworks aligned with national health and industrial policy.

Investor Benefits: How This November Print Re Prices Saudi Digital Health

For Saudi investors whether institutional allocators, family offices, or specialized funds the November print around Seha VH and national procurement collaborations changes the calculus in several ways.

1. Reduced execution risk for virtual care.

An award validated, Guinness recognized virtual hospital that already integrates hundreds of facilities and tens of services provides strong evidence that complex virtual care models can work at scale in Saudi Arabia. This de risks future investments in adjacent digital health assets, from specialty telehealth to AI assisted triage.

2. Clearer line of sight from policy to cash flows.

Vision 2030 and the Health Sector Transformation Program are no longer abstract frameworks; they are showing up as market growth numbers (high teens to mid 20s CAGR), project awards, and procurement reform. This makes it easier to underwrite long duration digital health plays where payback depends on policy continuity.

3. Stronger supply chain and local content story.

Efforts to professionalize procurement and boost local content in healthcare purchases align digital health investment with broader themes that already resonate in Saudi portfolios: industrial diversification, resilience, and technology transfer.

4. Exposure to global growth with domestic risk anchors.

Global telehealth and digital health markets are expanding rapidly, but many of the pure play names are listed in markets with their own macro and regulatory risks. Positioning capital in Saudi digital health where growth is anchored in domestic policy and demand, but linked to global technology and service vendors offers a way to capture that upside with a different risk profile.

Recap: From Zimam Trophy to Balance Sheet Outcomes

Saudi digital health’s November print is more than a news cycle. It provides a coherent snapshot of a system in transition from experimentation to institutionalization.

On the front end, Seha Virtual Hospital’s award consolidates its role as a reference architecture for large scale virtual care, with documented impacts on access, efficiency, and patient satisfaction. On the back end, new procurement and supply chain collaborations indicate a deliberate effort to treat digital health as an infrastructure asset whose performance depends on disciplined sourcing, logistics, and local industrial capabilities.

For Saudi investors, the message is clear: this is no longer a bet on whether digital health will matter. It is a question of how to participate directly in platforms and providers, indirectly via enabling infrastructure, or through structured vehicles that align with national health and industrial policy. The November print suggests that the window for building differentiated exposure, ahead of a more crowded global capital queue, is still open.