From “Gut Feel” to Instrument Panel

Saudi real estate is about to move from driving on instinct to driving with a full dashboard.

In February 2026, the Minister of Municipalities and Housing, Majid Al-Hogail, confirmed that a new suite of real estate market indicators will be launched in 1Q 2026 and that the Real Estate Market Balance program piloted in Riyadh will be activated across all cities based on these indicators.

In parallel, the digital Real Estate Indicators platform run by Real Estate General Authority (REGA) already hosts transaction and rental data at Kingdom, city, and even neighborhood level, with interactive visualizations. The 2026 upgrade is less about “inventing data” and more about:

- standardizing which indicators matter,

- publishing them at higher frequency, and

- using them to actively steer land release, taxation, and regulation through the expanded Real Estate Market Balance program.

For investors, this is not a cosmetic open-data initiative. It is a structural shift: once vacancy, rent-to-income ratios, and sustainable price trends are quantified and visible, you can no longer rely on opacity to justify margins, nor on anecdotal “hot market” stories to support underwriting.

This piece unpacks that shift through a global, regional, and Saudi-specific lens, then drills into challenges, policy solutions, and the practical benefits for institutional capital.

Global Landscape: Transparency as a Priced Asset

Over the last decade, global real-estate capital has increasingly priced transparency, not just yield.

The Global Real Estate Transparency Index 2024 by JLL ranks markets on data availability, regulatory clarity, and enforcement quality. Markets that score higher attract a disproportionate share of cross-border capital, even when yields are tighter, because investors can underwrite with narrower error bars.

A few global patterns matter for how we interpret Saudi’s move in 2026:

- Mature markets increasingly publish official rental and price indices, not just private-sector dashboards.

- Regulatory authorities tie zoning, taxation, and macroprudential tools (LTVs, DSTI caps) to observable market indicators/vacancy, rent-to-income, price-to-income, days-on-market.

- Data transparency is no longer a “nice-to-have” marketing pitch; it is part of prudential risk management and AML/CFT supervision.

Saudi’s new indicators sit squarely in this global trend: real estate is being treated as a systemic asset class that requires continuous monitoring like credit, banking, or utilities rather than as a loosely-tracked pool of projects.

Regional Landscape: The GCC’s Transparency Benchmark

In the GCC, Dubai and Abu Dhabi set the benchmark for real-estate transparency.

Dubai’s Mo’asher indexan official sales and rental performance indexpublishes monthly data on transaction volumes, values, and price indices, and is widely referenced by both local and global investors. In 2025, Dubai recorded over 200,000 residential transactions worth more than AED 540 billion, with total real-estate deals (all asset classes) nearing AED 917 billion.

That transparency has been recognized internationally. In the 2024 Global Real Estate Transparency Index, Dubai achieved a “Transparent” ranking (the only market in MENA to do so), while Abu Dhabi ranked among the top five global improvers, off the back of initiatives like the DARI platform and a residential rental index.

For Saudi investors, the regional lesson is simple:

- Transparency tightens spreads between asking and clearing prices.

- It reduces information asymmetry between large and small players.

- It supports institutionalizationmore REITs, more listed developers, more structured products.

Saudi’s 2026 indicator rollout is its own version of this regional playbook, calibrated to its scale and Vision 2030 priorities.

Saudi Landscape: From Fragmented Data to an Integrated Indicator Regime

Existing Data Infrastructure

Saudi does not start from zero. Several building blocks are already in place:

- Digital Real Estate Indicators & Interactive Maps on REGA’s platform, which provide sales and leasing data across regions, cities, and neighborhoods, with geographic visualizations.

- Real Estate Market Balance (Tawazoun) pilot in Riyadh, led by the Royal Commission for Riyadh City (RCRC), which uses data to sequence serviced land release and match supply to demographic and income realities.

- A growing suite of regulatory instruments: White Land Tax reforms, the Real Estate Units Ownership System, and modernized brokerage and off-plan sales regulations.

But until now, these have mostly been sectoral tools valuable, but not yet woven into a single set of macro indicators that investors can anchor on quarter after quarter.

What the New Indicators Add

Public remarks and ministry communications suggest that the new 2026 indicator suite will explicitly track:

- Vacancy rates by segment and city

- Rental inflation and rent-to-income ratios

- Sustainable price trends (not one-off spikes)

- Transaction volumes and values, segmented by purpose and buyer type

- Supply pipelines aligned with Market Balance interventions

In other words, the inputs institutional investors already track in fragmented spreadsheets will now have an official, standardized, and regularly updated reference.

Reading the Latest Data: A Snapshot from Q3 2025

To understand why these indicators matter, it helps to look at how volatile the market has been even with partial data. Cavendish Maxwell’s Saudi Arabia Residential Market Performance Q3 2025 gives a good pre-indicator baseline.

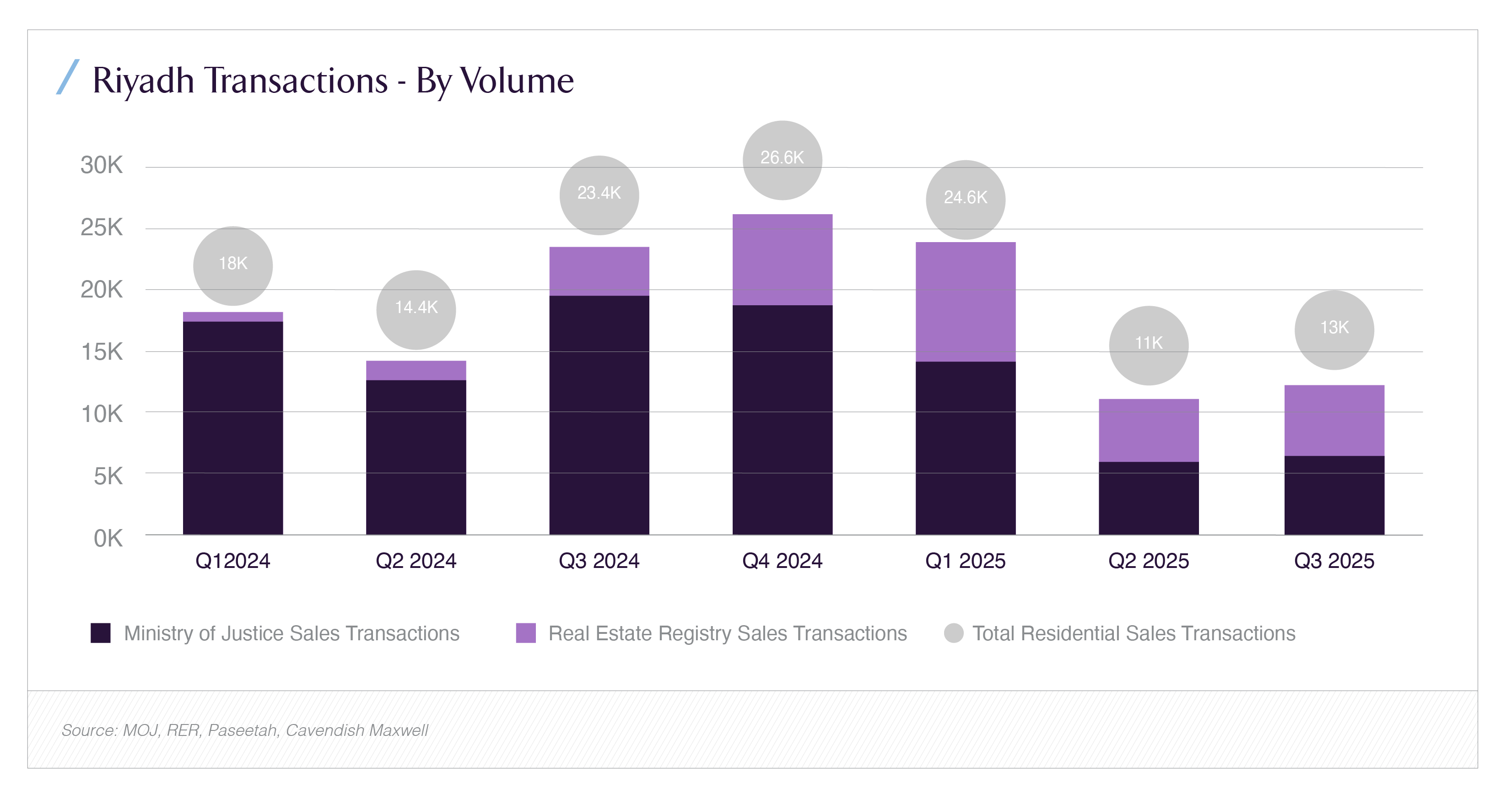

In Riyadh, residential sales transaction volumes and values swung sharply between Q1 2024 and Q3 2025 as affordability pressures and financing costs bit after a period of rapid price appreciation:

- Volumes peaked near 26.6k transactions in Q4 2024, before dropping to 13k in Q3 2025.

- Transaction values fell from ~SAR 48.7 billion in Q1 2025 to ~SAR 17.6 billion in Q3 2025.

At the same time, Riyadh’s residential supply pipeline remained heavy: roughly 10,000 units delivered in the first nine months of 2025, with a further ~6,000 expected by year-end and around 57,000 scheduled for 2026–2027.

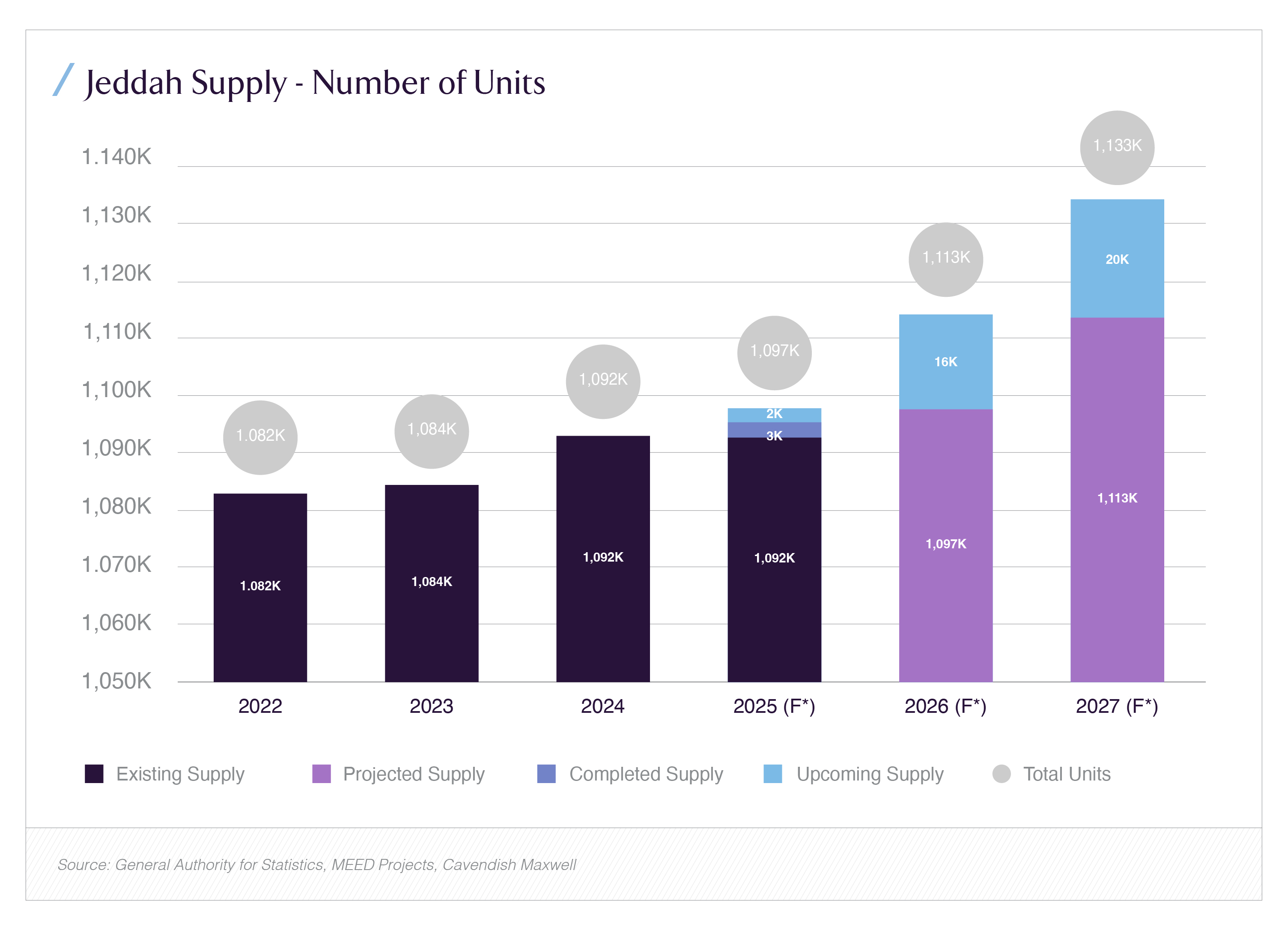

In Jeddah, volumes and values behaved differently: a more moderate year-on-year decline in transactions, with some stabilization in prices and a relatively steady supply pipeline (about 3,000 units added in the first nine months of 2025, 2,000 more expected by year-end, and ~36,000 projected for 2026–2027).

These charts underscore the policy problem the new indicators are meant to solve:

- Demand and supply are not moving in sync across cities.

- Affordability and financing costs are biting differently by segment.

- Without standardized indicators, the response risks being either blunt (national policies that ignore city dynamics) or delayed (reacting after price spikes or slumps).

Challenges: Execution, Data Quality, and Behaviour Change

The 2026 indicator rollout is promising, but not risk-free. Three execution challenges are particularly relevant for investors:

1. Harmonizing Data Sources

Saudi real-estate data has historically been spread across:

- Ministry of Justice registries,

- the Real Estate Registry,

- municipal systems,

- private-sector transaction trackers.

Aligning these into a single indicator set requires rigorous deduplication, consistent definitions (e.g., what counts as “vacant” or “completed”), and clear metadata. Any ambiguity will directly impact investor trust.

2. Timeliness and Revision Discipline

Indicators that arrive six months late, or that are frequently restated without clear versioning, can be worse than no indicators at all.

The global experience with price indices and rental benchmarks shows that:

- Lag undermines their usefulness for tactical decisions.

- Opaque revisions undermine their usefulness for strategic positioning.

Saudi’s challenge is to embed a publication calendar and revision policy that institutional investors can rely on.

3. Behavioural Adjustment for Market Participants

Once indicators are live, developers and brokers face a new reality:

- Over-priced inventory will be visible in days-on-market and price-to-income ratios.

- Under-supplied segments will be visible in vacancy and rent-to-income stress.

- Land hoarding will be visible when White Land plots remain undeveloped despite clear demand signals and subject to higher fees under the updated rules.

For players used to operating in an opaque environment, this is a significant behavioural adjustment. Some will adapt; others may struggle, particularly if they relied on asymmetry rather than operational excellence.

Policy Solutions: How Market Balance Uses the New Indicators

The expanded Real Estate Market Balance program is the execution arm of the indicator regime.

At its core, Market Balance aims to answer four questions at the city (and eventually sub-city) level:

- Is supply aligned with demographic and income trends?

- Are price and rent trajectories consistent with sustainable affordability?

- Is land being held idle in areas where serviced supply is needed?

- Are regulatory levers/infrastructure sequencing, zoning, taxation being used in the right order?

The new indicators give the program something it previously lacked: quantitative triggers rather than qualitative judgments. For example:

- If rent-to-income ratios breach a threshold while vacancy stays low, targeted land release and infrastructure spend can be accelerated in that sub-market.

- If transaction values are falling while vacancy rises, approvals for speculative projects can be tightened until absorption improves.

- If White Land plots remain undeveloped in high-pressure zones, higher fee tiers can be applied, sharpening the incentive to build or dispose.

Crucially, this isn’t just a municipal planning story. It’s a macroprudential story: real estate is a large, leveraged asset class; smoother cycles and fewer bubbles reduce systemic risk for banks and investors.

Benefits: What Better Indicators Change for Investors

For Saudi and international investors, the 2026 indicator regime changes both how you invest and what risk premia you demand.

1. Clearer City-by-City Strategies

The Cavendish Maxwell data already shows that Riyadh, Jeddah, and Dammam are behaving differently in terms of transaction swings and supply pipelines. The new indicators will formalize that divergence and make it easier to build city-specific theses:

- Riyadh as a scale, policy-intensive market where rent freezes, White Land enforcement, and foreign ownership reforms interact with each other.

- Jeddah has a coastal, tourism-linked market where supply catch-up and logistics expansion drive both residential and hospitality demand.

- Dammam is an industrial and energy-linked market where affordability is a key differentiator, and where modest but steady supply growth can be tracked transparently.

With standardized indicators, you can explicitly tie each strategy to observable metrics/vacancy, rent-to-income, transaction velocity rather than to qualitative narratives.

2. Better Underwriting and Exit Assumptions

For income-producing assets (residential rental communities, logistics, Grade-A offices, healthcare, education), the new indicators provide:

- Forward-looking signals on rent growth potential and affordability ceilings.

- Comparables across sub-markets for yields, rents, and occupancy.

- Context for exit pricing is especially important as REITs and listed developers deepen.

This is particularly relevant as Saudi continues to position itself as a major hub for regional HQs, tourism, and logistics each with distinct real-estate footprints and risk profiles.

3. More Credible Thematic and Impact Strategies

For investors running thematic strategies, affordable housing, student housing, logistics, healthcare real estate access to granular, official indicators allows you to:

- Quantify underserved segments more precisely (e.g., where rent-to-income is stretched but vacancy is low).

- Demonstrate impact (e.g., how a new development compresses rent-to-income or stabilizes prices in a district).

- Structure performance fees and governance around measurable outcomes, not just IRR.

In a world where LPs are increasingly sensitive to impact, governance, and systemic risk, that measurability is a differentiator.

4. Lower Information Risk, Not Necessarily Lower Returns

One common concern is that transparency will compress spreads and “kill alpha.” Experience from markets like Dubai and Abu Dhabi suggests a more nuanced reality: capital does not flee when transparency improves; it tends to rotate toward better managed, better located, and better governed assets.

For Saudi real estate, that likely means:

- Weakly capitalized, speculative projects will find it harder to price in narratives that contradict observable data.

- Well-governed platformsREITs, large developers, specialized operators will find it easier to attract institutional capital, at scale, on repeat.

- International capital will be able to justify exposure to Saudi real estate inside global portfolios using the same transparency frameworks it applies elsewhere.

The result is not “lower returns for everyone,” but more disciplined returns for those who can operate in a data-rich environment.

Recap: Indicators as a New Governance Layer

Saudi’s decision to launch unified real estate market indicators in 1Q 2026 and extend the Real Estate Market Balance program nationwide marks a clear inflection point.

Globally, transparency has become an investable attribute. Regionally, Dubai and Abu Dhabi show how official indices and open data can pull in capital and deepen markets. Saudi is now internalizing those lessons at a larger scale, tailored to Vision 2030’s urban, housing, and diversification agenda.

The new regime does three things that matter for investors:

- It hard-wires data into policy. Land release, taxation, and regulatory actions will increasingly respond to measurable indicators, not anecdotes.

- It narrows information asymmetry. The distance between what insiders know and what disciplined capital can see will shrink.

- It reframes risk. Cyclical volatility will not disappear, but the tools to understand and price it will be far stronger.

For Saudi investors, the question is no longer whether transparency is coming. It is how quickly you can embed the new indicators into your investment committees, underwriting models, and portfolio steering mechanisms before they become the baseline that everyone else uses too.