Showing its success in making its housing finance system bigger, more securitized, and more interconnected, Saudi Arabia officially passed the whopping SR 900 billion mark in October 2025. This development is vital in the context of the balance between household leverage, bank balance-sheet risk, and liquidity across the financial system. This development is also consistent with the Saudi Real Estate Refinance Company (SRC) and regulators' move to establish a domestic RMBS market that can re-engineer how mortgages are funded and priced. All these measures contributed to the faster credit expansion into this field and will result in important implications in terms of prices, defaults, and policy in the future.

Quick snapshot of the numbers

Chief points include:

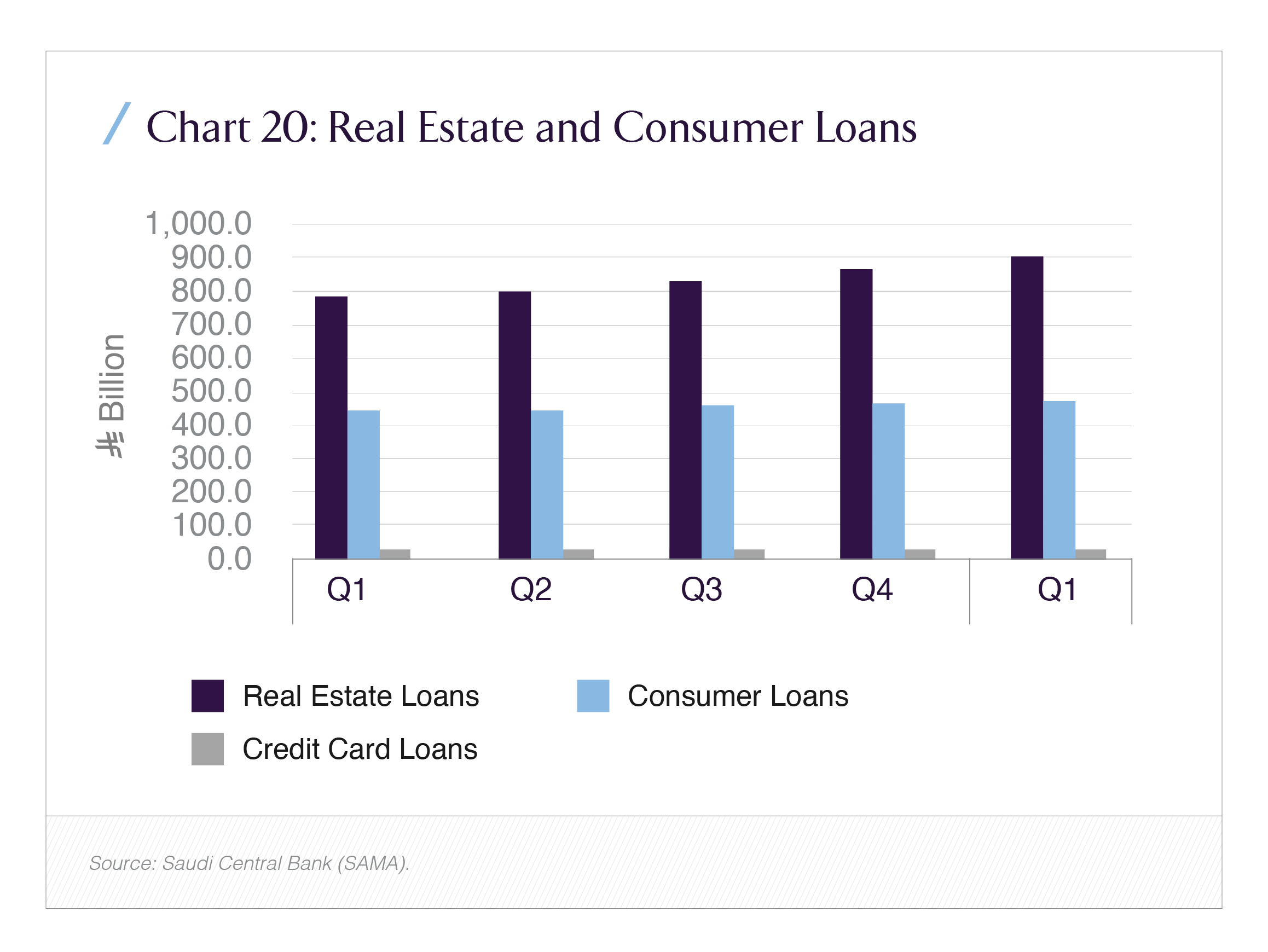

- Reports indicate real-estate lending surpassed SR 900 billion in 2025.

- Another report, called SAMA’s development reports, shows real-estate loans were around SAR 922.2 billion at end-Q1 2025 and rose to SAR 932.8 billion at end-Q2 2025.

- Signaling a combined effort to enhance secondary market routes for mortgages, a PIF company called SRC and SAMA gave a no-objection for transactions involving residential mortgage-backed securities (RMBS),Saudi Arabia’s first, in August 2025.

Why the surge happened supply, demand, and policy

Three forces combined to produce a rapid expansion in mortgage volumes:

- Policy push for homeownership & Vision 2030 initiatives. Government housing programs and regulatory incentives have steadily increased mortgage access and affordability, moving home-ownership rates higher and directing credit into residential markets.

- Bank appetite and product innovation. Banks expanded both retail mortgages and corporate real-estate loans; SAMA data flagged retail mortgages constituting the majority of the outstanding stock, while corporate real-estate lending also grew strongly, reflecting developer financing and commercial real estate activity.

- Liquidity and capital markets reforms. The launch of RMBS and SRC’s transactions gives banks a new outlet to manage mortgage exposure and raise funding a structural market development that encourages origination because lenders can now plan to sell or securitize mortgage pools.

Leverage profiles and where the risk sits

As mortgage stock rises, two leverage channels matter:

- Household leverage. A significant risk can be middle-income buyers with long tenors or high loan-to-value (LTV) products, and the risk is not the middle-income buyer themselves, but the interest rate. If the interest rate gets even a bit high, it can damage household balance sheets.

- Bank / system leverage. Bank sector risk involves dependency on the real estate market until securitization becomes widespread in the system. The SAMA figures show real-estate lending constituted nearly 30% of total bank credit by mid-2025. RMBS providing a tool to transfer credit off bank balance sheets can be fresh air, but securitization is still the key.

Leverage is rising in both households and the banking sector, but the emergence of securitization tools could moderate bank concentration over time if RMBS markets scale up and investor demand is sustained.

Default risk current profile and what could change

So far, the data have not signaled a spike in mortgage delinquencies; SAMA and banks continue to report stable asset-quality metrics. But three factors could raise default risk:

- Interest-rate shock. Saudi mortgage pricing and borrower ability to service debt depend on interest rates and the macro cycle. A sharp global or domestic tightening could increase monthly payments for floating-rate products or raise refinancing costs at a time when property values are under pressure.

- Concentration and loan features. High LTVs, longer initial interest-only periods, or a large share of mortgages to speculative buyers amplify vulnerability. Public reporting suggests retail mortgages are a dominant share; the exact composition of LTVs and borrower credit quality will determine resilience.

- Developer and commercial contagion. Corporate real-estate lending rose faster than retail at times; a downturn in commercial real-estate (or stressed developers) could produce second-round effects on banks and thus indirectly on retail mortgage funding.

Strong SAMA oversight, borrower protections, and the SRC’s role in providing alternative funding reduce the probability of a systemic shock. But the system will be sensitive to macro shocks unless underwriting standards remain prudent.

Impact on property prices will more credit keep prices rising?

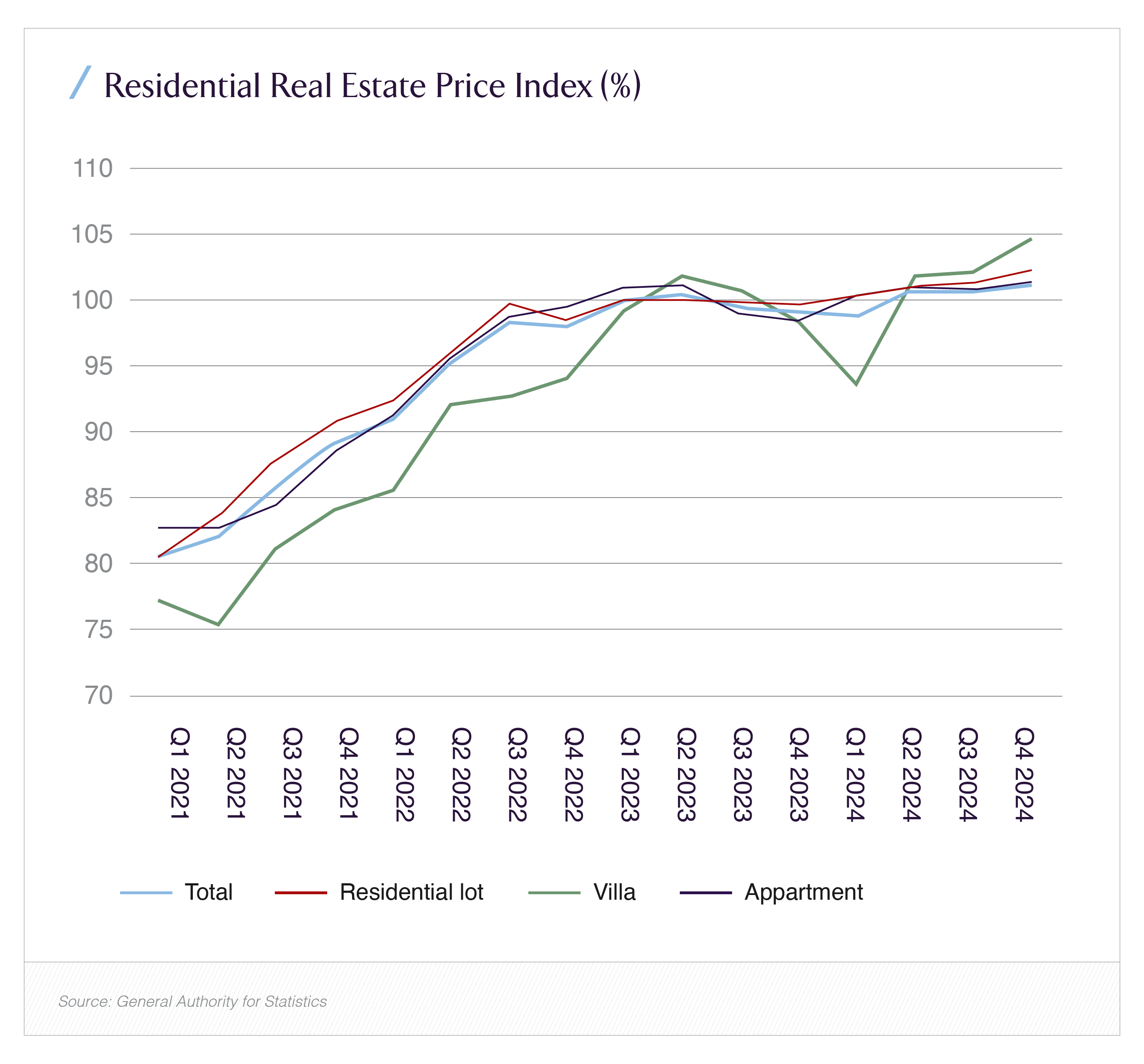

Credit is a clear fuel for price growth: greater access to mortgages typically expands buyer demand and can push prices up, especially in markets with constrained supply. In Saudi Arabia:

- Short-term: the mortgage expansion has likely supported price growth in key urban markets, given elevated demand and supply lags. Several market trackers noted regional price gains in 2024–25.

- Medium-term: the price trajectory will depend on supply additions (new housing stock), the elasticity of demand, and whether lending growth is concentrated among owner-occupiers or investors. If mortgage growth shifts toward investor/speculative buying, price volatility risk increases.

- Policy response: if authorities judge credit-driven price overheating is occurring, they can adjust macroprudential tools (LTV caps, stress-testing, borrower buffers) or fine-tune the secondary market structure to steer origination standards.

The SRC and the advent of RMBS why securitization changes the game

The decision to build a functioning RMBS market is the structural development with perhaps the largest long-term consequences:

- SRC as a market maker. SRC’s issuance of RMBS and its ability to buy mortgages from banks create a credible secondary buyer, improving banks’ liquidity planning and potentially lowering funding costs for mortgage origination. SAMA granted no-objection clearance earlier in 2025; SRC’s first RMBS transactions were executed in late summer 2025.

- Investor diversification. RMBS opens the door for institutional investors to buy tranches of mortgage pools, including sharia-compliant structures. That increases the investor base beyond bank deposits and local funding, helping to share risk more widely across the capital markets. Analysts have noted that a functioning RMBS market could materially improve liquidity for banks and encourage more predictable origination behavior.

- Standards and transparency. For RMBS to be stabilizing rather than destabilizing, underwriting, pool disclosure, and servicer performance must meet high standards. Early legal, advisory, and structuring work by international firms on the inaugural transactions suggests the Kingdom is trying to import global best practices in documentation and investor protections.

Bottom line: RMBS gives banks a credible exit option which should, in theory, lower funding costs and allow lenders to underwrite more mortgages without overstretching capital. But the benefit depends on investor confidence, regulatory oversight, and the quality of underlying loans.

What to watch next (policy and market signals)

- Delinquency and NPL trends. SAMA and banks will publish the early warning signals. Any uptick in arrears would be the clearest sign that rapid credit growth is producing strain.

- LTV and underwriting disclosures. Transparent reporting of new origination LTVs, borrower income verification standards, and stress-testing assumptions will tell whether growth is prudent or aggressive.

- RMBS market take-up. Are subsequent RMBS transactions executed? Is there strong demand from domestic and international investors for senior tranches? Successful repeat issuance and broad investor participation would indicate the market is maturing.

- Macroprudential adjustments. Watch for any targeted tightening (caps, buffers) if housing inflation or speculative behaviour accelerates.

Conclusion

Saudi Arabia’s crossing of SR 900 billion in mortgages reflects its willingness to actually bring to reality its Vision 2030. This milestone is clear evidence of Saudi Arabia’s decision to deploy policies that will bring revolution in its housing market, as can be seen by the emergence of the Saudi Real Estate Refinance Company (SRC) and regulators' move to establish a domestic RMBS market.

With securitization, controlled interest rates, and a tight speculative buyers ratio, the chances of defaults can be averted, and strict underwriting and ongoing transparency can convert rapid credit growth into a stable expansion of ownership and investment. Further, to keep things in control, measures like keeping origination quality high, keeping an eye on arrears, and making sure the fledgling RMBS market deepens without lowering standards should be adopted.