In August–October 2025, Saudi Arabia reached a milestone: the Saudi Real Estate Refinance Company (SRC), a Public Investment Fund (PIF) subsidiary, completed the Kingdom’s first residential mortgage backed securities (RMBS) transaction. The deal executed with HSBC Saudi as arranger and advised by A&O Shearman (for HSBC) and White & Case (for SRC) is being billed as a structural template that can unlock long term liquidity for banks, broaden investor access to home finance assets, and strengthen Saudi capital markets. This article unpacks the deal mechanics, the credit enhancement and tranche structure typically used in RMBS, Shariah compliance issues, investor appetite, and the macro implications for banks, borrowers, and the housing market.

Why this matters now

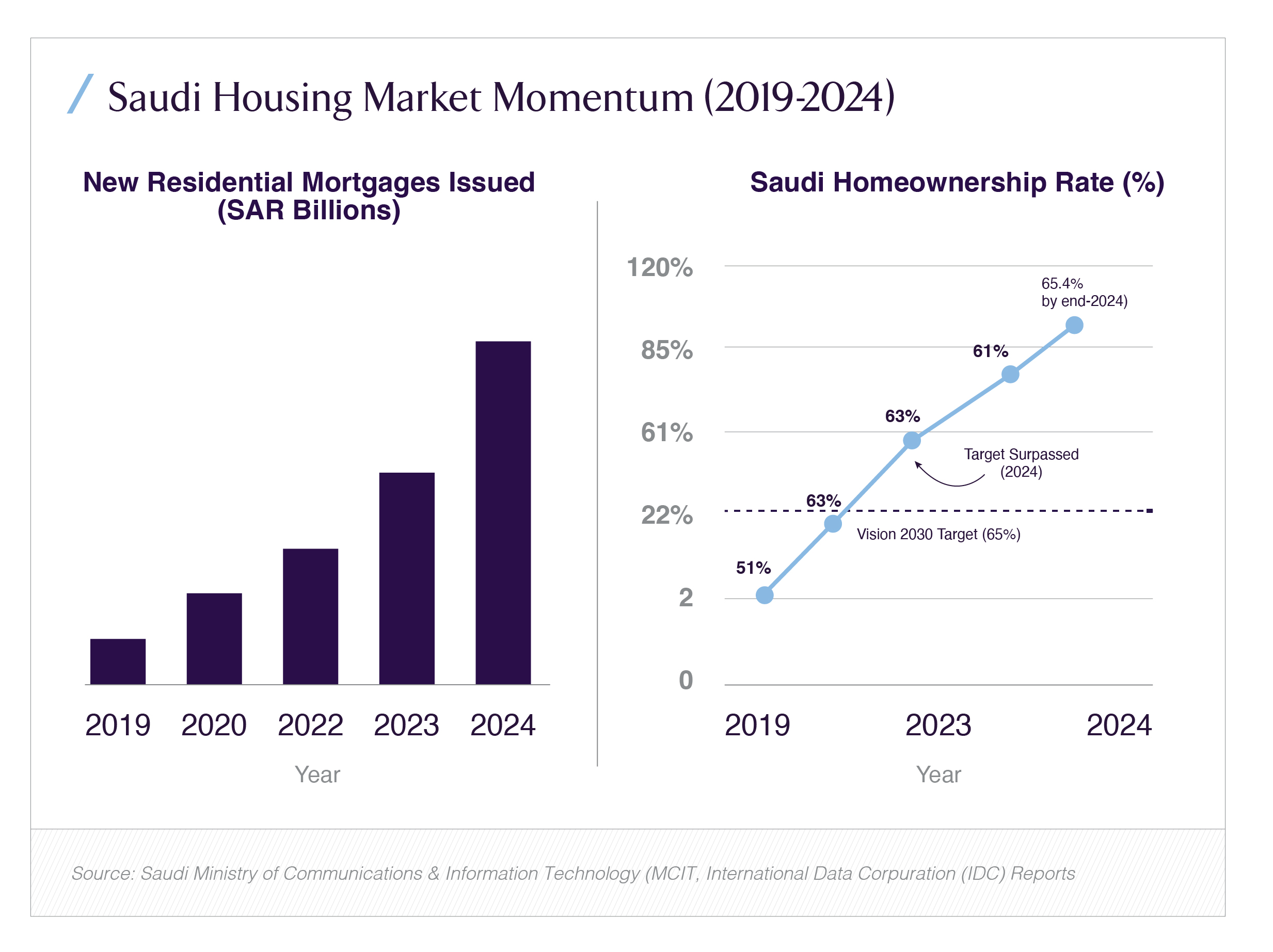

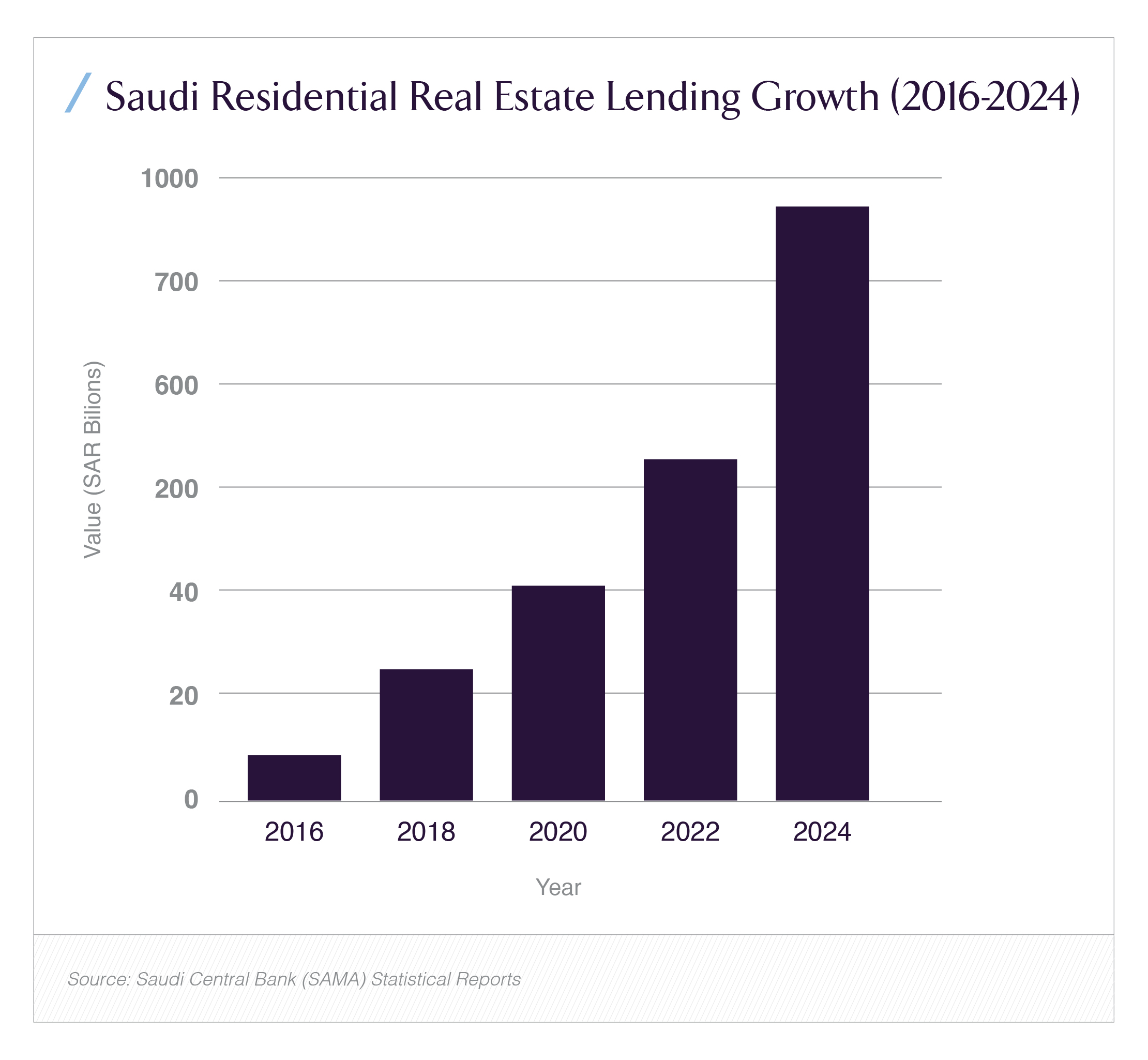

Saudi mortgage activity and real-estate lending have expanded rapidly in recent years. New residential mortgages issued by banks rose to SAR 91.1 billion in 2024 (about USD 24.3 billion), a 17% year on year increase, and real estate loans outstanding reached record levels (SAR-hundreds of billions), making housing finance a large and growing asset class in the banking system. Meanwhile, homeownership has climbed, with official reporting showing Saudi household ownership at roughly 65.4% by end 2024, surpassing earlier targets. An RMBS market gives banks a mechanism to convert those on-balance-sheet mortgage loans into tradable securities freeing capital to originate more mortgages and transferring select credit risk to capital markets investors.

How an RMBS in Saudi Arabia is likely structured (and why structure matters)

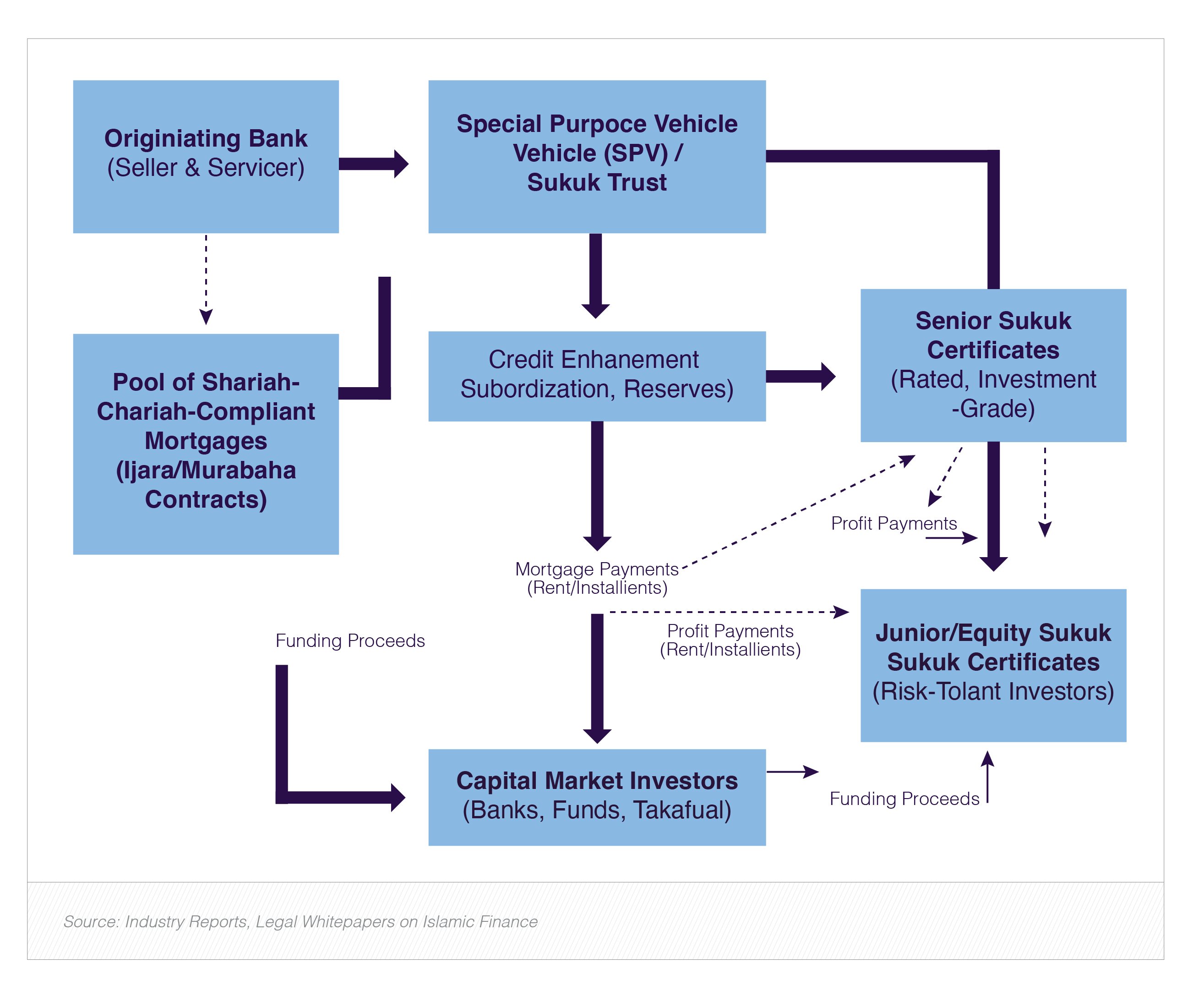

Although deal documents are proprietary, the press releases and market commentary show the SRC issuance follows international RMBS best practice adapted for local regulation and Shariah considerations. Key structural elements to look for:

• Pool composition and underwriting standards. Issuers typically securitize a pool of performing residential mortgages that meet pre-defined eligibility criteria (LTV caps, documentation, seasoning). High underwriting standards make senior tranches investment grade and attractive to conservative investors. The SRC program is built to package mortgages of demonstrated credit quality to create marketable tranches.

• Tranching and credit enhancement. RMBS are split into tranches (senior, mezzanine, junior/equity) with sequential payment or waterfall rules. Credit enhancement can be internal (subordination i.e., junior tranches absorb first losses), excess spread, reserve accounts, and external (guarantees or insurance). Given SRC’s PIF ownership and previous guaranteed sukuk programmes, market reports suggest the inaugural RMBS used structural credit support to achieve stronger ratings for senior notes. That mix improves investor confidence and pricing while leaving subordinated pieces for risk-tolerant buyers or the sponsor.

• Ratings & investor segmentation. Issuers seek ratings for senior tranches to access domestic institutional investors (banks, insurance, asset managers) and, potentially, qualified foreign investors. A rated senior tranche widens the buyer pool and reduces the cost of funding for the originators. Market commentary around the SRC issuance highlighted an aim to create investment grade exposures that are Shariah-compliant.

• Liquidity and standardization. For an RMBS market to scale, standardised documentation, servicer platforms, and regulatory certainty are essential. SRC’s program and SAMA’s oversight aim to provide that predictable framework so future deals can be repeatable and liquid.

Shariah compliance: sukuk structures and Islamic mortgages

Shariah-compliant securitizations require that the economic substance and contracts conform with Islamic finance principles (no riba/interest, asset backing, permissible contract forms). There are two common approaches for RMBS in majority-Muslim jurisdictions:

- Sukuk style certificates: The pool or SPV issues trust certificates backed by receivables, with profit distributions designed to mimic coupon payments. SRC and counsel have publicly referenced compatibility with sukuk frameworks and previous SRC sukuk issuances, suggesting the RMBS uses structures designed to produce Shariah-compliant returns (e.g., Ijara/leaseback or murabaha style arrangements adapted for receivables).

- Shariah compliant mortgage product design: Underlying mortgages themselves can be structured as Shariah approved financing (diminishing musharaka, ijara muntahia bittamleek, etc.). Packaging portfolios of such contracts simplifies the RMBS’s Shariah vetting and makes the securities suitable for Islamic institutional investors.

For investors and portfolio managers, clarity on the Shariah board opinions, the trustee’s role, and operational mechanics is essential; the SRC issuance is being positioned as a template precisely so other originators and asset managers can rely on the precedent.

Market appetite who will buy Saudi RMBS?

Investor demand will likely come from several buckets:

- Domestic banks and insurers are seeking credit enhanced yield while matching liability profiles.

- Islamic banks and Takaful/insurance funds want Shariah compliant assets.

- Sovereign/pension funds and asset managers that value high quality, medium-term fixed income in riyal or sukuk format.

- International capital qualified global investors looking for diversification into an under penetrated mortgage market, provided the securities have transparent legal, rating, and currency features.

Early reporting indicates strong domestic policy support and institutional interest, but long term success hinges on repeat issuances, secondary market liquidity, and standardized disclosure. Bloomberg and structured-credit outlets noted the launch is intended to “drive liquidity” and encourage banks to lend more.

What this means for banks, borrowers, and housing supply

For banks: RMBS creates a balance sheet tool that reduces mortgage capital consumption and funding volatility. By selling eligible mortgages into securitizations (or collateralising them in an SRC program), banks can recycle capital and scale mortgage origination without proportionally increasing funding costs. That effect can be material in a market where real estate loans are already a significant share of bank assets (real estate lending reached SAR 846–922 billion in recent official releases and reporting).

For borrowers and housing supply: Lower funding costs and greater lender capacity can expand mortgage availability and affordability if lenders pass on pricing improvements to end borrowers. The SRC’s public mandate (increase homeownership and support Vision 2030 housing targets) suggests policy intent for securitization to have downstream benefits for supply and affordability. However, these gains are conditional on competitive mortgage pricing and continued policy support for affordable housing development.

For investors and capital markets: RMBS brings a new riyal-denominated, asset-backed class to institutional portfolios. If a domestic secondary market develops, it will deepen fixed-income capital markets and create natural long-term assets for pension and insurance funds. The transaction also signals structural reform an important signal to foreign investors that Saudi markets are maturing in complexity and depth.

Risks and watch points

• Execution risk: Early transactions need airtight legal opinions, operational servicers, and transparent disclosure. Any operational lapse in servicing, remittance, or documentation will undermine market confidence.

• Credit & macro risk: A sharp economic slowdown or property-price correction would stress mortgage pools. Robust underwriting and conservative enhancement levels will be vital.

• Liquidity & secondary market: Initial deals may trade thinly. The market’s ability to attract diverse buyers (not just local banks or PIF-linked investors) will determine pricing dynamics and true “unlocking” of liquidity.

• Regulatory clarity: Continued SAMA and Capital Market Authority (CMA) support to clarify tax, bankruptcy, and investor protections for securitized assets will be essential to scale the RMBS market.

Takeaway

SRC’s RMBS transaction is less an isolated capital-markets exercise than a strategic lever: it is a template aimed at converting mortgages into investable, Shariah compatible securities and thereby freeing bank capital to lend more. The immediate benefits are liquidity and investor choice; the long term payoff if repeatable issuance, standardized documentation, and robust secondary markets follow is a deeper, more diversified Saudi capital market that supports homeownership objectives under Vision 2030. For banks and investors, the initial RMBS is a practice in balancing credit enhancement, Shariah integrity, and investor transparency; for policymakers, it’s a policy instrument to mobilize private capital into housing finance.